Why buy-ins might not be the only answer

There is currently a high level of demand from defined benefit (DB) pension schemes to transfer the responsibility for paying member benefits to insurance companies. Over the next 10 years, if things continue to change at the current rate, it is projected that insurers will be managing half of all outstanding defined benefit assets, worth some £1 trillion.

The gilt market crisis of 2022

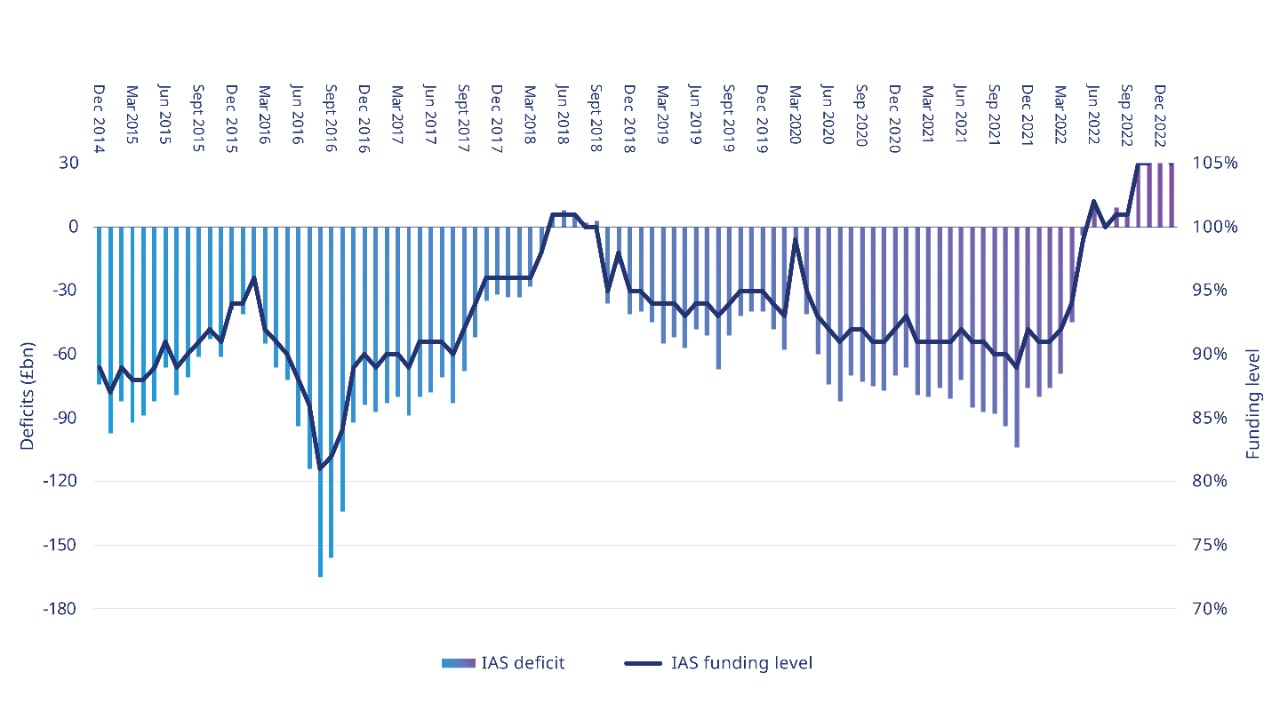

What a difference a crisis makes. The September 2022 UK mini-budget sparked a sell-off in the gilt market, this correspondingly shocked bond yields to spike higher, completing the steady rise in yields that had been under way all year. This has left many DB pension schemes in the UK much better funded because liability values have fallen (a consequence of higher yields), insurer pricing looks cheaper (as insurers can generate higher returns from corporate bonds and other assets), and outstanding deficit contributions now look proportionately larger and more capable of bridging any deficit or funding gaps.

Taking advantage of their stronger positions, many schemes are eager to de-risk through buy-in and buyout contracts with insurance companies — also referred to as a bulk purchase annuities or risk transfers. Doing so removes the three main risks schemes face: investment, inflation and longevity. In the case of buyout contracts the insurer replaces the employer as the ultimate entity liable to pay the pensions (the covenant risk).

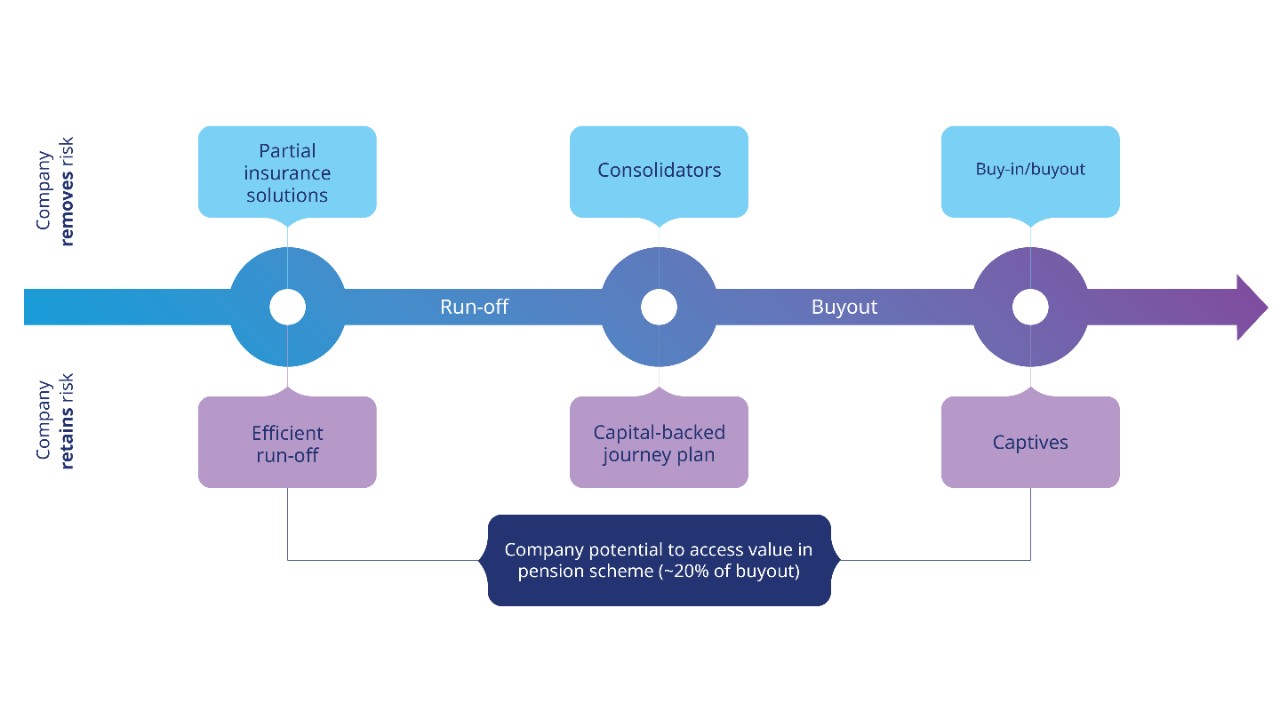

However, are insurance contracts the best solution for all schemes, or are there better choices? After all, alternatives such as cashflow-driven investing or establishing captive solutions also remove risk, yet do not transfer economic value solely to the insurer. So why are so many schemes and sponsors rushing to transfer their pension liabilities to a small set of insurers? What might be the consequences? It seems wise to consider all the options before signing up to a buy-in or a buyout contract, which are irrevocable and cannot be unwound.

Gold or silver plated?

Risk transfers will make a lot of sense for schemes where the sponsoring employer is not in a strong position to support the financial risk of running a pension scheme off into the future. The security of a regulated insurer backing future pension payments is, in such cases, likely to offer members a far higher level of security than that provided by a weak corporate employer.

Nevertheless, while insurance companies are highly regulated and, by and large, well-managed entities, there is a trade-off involved in swapping the sponsor of a pension fund over from a corporate sponsor to an insurer. This trade-off might offer higher security, as member benefits are backed by the insurer, but it will also come with potential unknown risk, given the irrevocable and very long-term nature of the contract.

One such potential risk is regulatory in nature. The proposed relaxation in Solvency II rules governing insurers’ capital, will, as the Bank of England has publicly stated, increase risk. There is one up-side: as buy-in and buyout policies become riskier, so they should, arguably, become cheaper. However, if the proposed changes are adopted, this will be of little comfort to those schemes and sponsoring employers that have already entered into buy-ins and buyouts — they will have to accept that their policies are now higher risk, even though they have gained no compensation. What’s more, as riskier underlying investments boost insurers’ profits, they also transfer value away from policyholders (such as DB scheme members) over to insurers’ shareholders.

As this trade-off in risks shows, even though they are an irrevocable asset that is typically held for 75 years, buyout policies may not be as gold plated as many believe.

The need for caution will surely be acknowledged retrospectively by those pension schemes that undertook partial buy-in policies (that is, policies covering just their pensioner liabilities and not deferred or active members) at the expense of their remaining assets, which consequently have had to be worked harder (as capital is tied-up in the buy-in policy). The assets that were not used to transact the buyout would typically have been invested in equities and other growth assets, combined with a small but highly leveraged liability hedging portfolio to reduce interest rate and inflation risks. Such portfolios suffered greatly during the 2022 gilt crisis and, most likely, saw a deterioration in their funding positions. Furthermore, subsequent changes in leverage rules have meant that higher levels of risk, due to lower hedge ratios, will have to be accepted going forward.

Overall, these issues and events serve as another important reminder of the unknown risks that can be faced when tying up capital in low-return, highly illiquid assets such as buy-in policies.

The reform package as a whole increases risk”. “The way it comes home to roost is if there is not enough capital backing pensions,”…“I would say it is highly likely that comes back to the public purse if that occurs,

A lost opportunity for members and sponsors alike

For the last two decades the DB pension sector has been focused on eradicating funding-level deficits, which grew larger due to lower interest rates. Over this time, the regulatory regime tightened. This made company deficit contributions more likely, and forced companies to close schemes to new members. In turn, this led to mature pools of liabilities and much shorter time horizons for investments.

In the decade before this period (the 90s), the focus was very different, as many schemes were in surplus and sponsoring companies enjoyed contribution holidays, albeit having benefited from high levels of investment risk and weaker measures of funding.

The decade ahead of us will, similarly, be characterised by strongly funded DB pension schemes. However, this time, it is projected that the schemes will feature low levels of investment risk and pay out predictable cashflow returns. Having reached this level of maturity, and as they will be operating in a higher interest-rate environment, it is quite feasible that many schemes will see material surpluses generated in the years ahead (assuming they stay invested). This will happen not just through higher-than-assumed returns on assets, but also due to the fact that other areas of actuarial prudence will unwind, as schemes mature still further. Due to this effect, we are already seeing some clients with funding levels at 110% to 120% on a buyout basis. This is despite the fact that they have adopted very low risk investment strategies for many years. It must be asked: how much higher could these funding levels go over the next decade?

At the same time, much of the UK is experiencing a cost of living crisis where inflation is outstripping the vast majority of pension payments (which typically increase with inflation by between 2% and 5% per annum) thus reducing pensions in real terms. Indeed, the true impact of a 3% rise in interest rates in less than 12 months is yet to be fully felt by most of us. Against this backdrop the previously unthinkable idea of awarding discretionary pensions, funded from funding-level surpluses, now looks to have some justification. It is therefore important to understand that transferring a pension scheme to an insurer takes this option off the table. This is because any resulting surplus on the scheme’s assets would be paid in profit to shareholders.

It should also be noted that there are a number of ways for sponsoring employers to profit from the economic benefit provided by a surplus (see Figure 2). Tax-efficient structures exist for this purpose (if the necessary forward planning is undertaken). There are also simpler mechanisms that can be put in place, such as using a surplus to supplement defined contributions.

So why don’t more organisations want to run off (i.e. pay the pensions as they fall due) these schemes so that the corporate entity, and possibly the pension scheme members, can benefit from the gains? There are a number of reasons that are often cited. These include: “Our pension scheme is a legacy issue,” “It is not core to the business,” “It takes up too much time,” and “The scheme is smaller due to rising yields, so any upside is smaller.”

However, there is also another reason which is not discussed as often — short-termism. Finance teams, particularly those working for listed companies, are incentivised to generate short-term gains to boost earnings and, ultimately, the performance of share prices. In contrast, returning economic value to the sponsoring company and its shareholder through a defined benefit surplus is a long-term strategy (even if it is one that can start immediately using structures such as captive insurance solutions).

If schemes are likely to end up in surplus (which isn’t always factored into the decision-making process when transacting with an insurer) imagine the true cost to shareholders of not participating in the surplus because schemes have chosen to buyout with insurers! A very broad estimate puts this at around 20% of the outstanding value of liabilities measured on a buyout basis.

Associations with the past — when DB pension schemes have been a problem — will undoubtedly influence thinking. However, the outlook is now very different as schemes are being managed with lower levels of investment risk than previously.

That said, following last year’s rise in interest rates, schemes are much smaller, which does reduce the practical options open to many DB schemes (particularly if corporates want to take advantage of the potential economic benefits). Industry consolidation would be helpful in this regard, but that is a different, albeit related, topic.

Unintended consequences

While undertaking a bulk purchase annuity neutralises a scheme’s existing risks, doing so may potentially add new problems. Take concentration risk by way of an example. Currently, there are about 5,000 DB schemes in the UK, backed by a similar number of companies. This means that sponsor-risk is well diversified. However, as the assets and liabilities of these schemes are transferred, those risks will rest with just a handful of insurers and will therefore become concentrated. As said at the start of this article, at the current pace, in the next ten years approximately half of the defined benefit market will be in the hands of a small number of insurers. Some £1 trillion is likely to be managed by these insurers.

Of course, the Regulator may grant new entrants access to the market to address such concentration fears. Even so, the projected level of assets managed by such a small number of companies — and, most likely, invested in a relatively narrow way — does raise the real likelihood of concentration risk. In addition, for some of the insurers this will represent a big change from their traditional business models and practices.

The UK DB market last saw such levels of concentration in the late 1990s, with a small number of asset managers controlling approximately 80% of pension assets. The assets under management grew to the point where they became unwieldy. The resulting business risk impacted behaviour, with the net result being that investment returns proved disappointing.

We also need to think about where UK insurers invest and where any concentration risk might manifest itself. With a home bias, UK insurers tend to invest in UK corporate credit. By international standards, this is a relatively small and illiquid credit market (especially when compared to the US and Europe). As a result, it is not unfeasible to consider a scenario where a credit crunch of some kind leads to lower capital solvency levels, which in turn leads to forced selling by insurers of largely domestic credit. If such a scenario seems unlikely, it should be remembered that insurers were forced sellers of equities during the bursting of the dot.com bubble. This was again the case during the 2008 global financial crisis when leading names saw their share price fall by approximately 80%, as the market questioned their dependability. It should also be remembered that forced selling in credit markets, which are less liquid than equities, can be equally messy, if not more so.

If a UK insurer were to fail, then pension fund members would be able to take some comfort in the knowledge that the Financial Services Compensation Scheme (FSCS) would cover their benefits to an unlimited value. However, the FSCS is unfunded and has not been tested. So, some unknowns exists, and the Prudential Regulation Authority itself speculates that tax payers would likely end up having to foot the bill. If paid in full, this would be a higher level of security than would be offered by the Pension Protection Fund (which is funded) should a corporate pension scheme fall into it.

Summary

Rather than simply settling for the comfort of entering into buyouts/buy-ins, we believe that trustees, sponsoring employers, stakeholders and advisers should consider the advantages and disadvantages of all of the options open to them.

At the end of this evaluation process, many may still conclude that buy-ins and buyouts are the best way to de-risk pension schemes — but it is likely that a number will discover alternatives that suit them better. Their decisions may be influenced by the appreciation that such buy-in/buyout policies are probably closer to being silver- than gold-plated, and that it may not be possible to identify all of the future risks associated with buying out a scheme.

- Head of UK Intellectual Capital

Before you access this page, please read and accept the terms and legal notices below. You’re about to enter a page intended for sophisticated, institutional investors only.

This content is provided for informational purposes only. The information provided does not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities, or an offer, invitation or solicitation of any specific products or the investment management services of Mercer, or an offer or invitation to enter into any portfolio management mandate with Mercer.

Past performance is not an indication of future performance. If you are not able to accept these terms and conditions, please decline and do not proceed further. We reserve the right to suspend or withdraw access to any page(s) included on this website without notice at any time and Mercer accepts no liability if, for any reason, these pages are unavailable at any time or for any period.