Not all sacrifices are bad for business

Do you have concerns about the rising costs impacting your business?

The cost-of-living crisis has been rapidly building into an economy-wide phenomenon, impacting businesses and employees in equal measure. A series of compounding factors may send CPI inflation soaring to 9.0% in April. The Bank of England has warned inflation could peak above 10% late this year and that there is a risk of recession.

The inflationary foundations were set by Brexit, limiting the supply of labour that would otherwise be available to satisfy unmet demand. The IMF estimates that the UK will have the highest inflation among the G7 next year and former Bank of England policymaker Adam Posen attributes 80% of this is because of Brexit.

The global bounce back from the Covid-19 pandemic has also brought with it wide-ranging inflationary pressure. Consumer demand in the UK, and other advanced nations with high vaccination rates, has more or less returned to normal – but many of the countries that supply goods, such as China, have not been so fortunate. Global supply chains have become overwhelmed and bottlenecks at ports have sent freight rates soaring. Ultimately, all such costs are passed onto businesses and ultimately consumers.

The conflict in Ukraine caused oil and gas prices to surge and they have remained elevated and exceptionally volatile since late February. Brent crude averaged around $60 per barrel for the previous five years but now trades at $110. This is heavily inflationary as oil is involved in the production of many other goods and the transportation of almost all of them. Natural gas prices have also shot up to the highest level since 2008.

Businesses are therefore facing a double-whammy of increased direct costs and increasing wage demands from employees struggling to absorb these increases. The 1.25% increase in National Insurance Contribution (NIC) rates for the 2022/23 tax year (as a result of the Health and Social Care Levy ‘the Levy’), only compounds wage bill pressure.

How can companies save costs with the current pressure on the payroll?

Salary sacrifice, also known as salary exchange, can provide an opportunity for employers and employees to offset some of the increase in costs stemming from the higher NIC rates for the 2022/23 tax year. It can be a great way for a company to reduce costs and improve its bottom line, whilst also helping employees to save money at this difficult time.

Salary sacrifice is a contractual arrangement whereby an employee ‘sacrifices’ or ‘exchanges’ part of their cash remuneration, usually in return for their employer’s agreement to provide some form of non-cash benefit. In the case of a pension salary sacrifice arrangement, employer pension contributions are not subject to employer or employee NICs, unlike salary payments. Therefore, whenever an employee sacrifices some of their earnings in return for an equivalent employer pension contribution, both the employer and the employee save money on their NICs on the amount of money sacrificed. Please note that other types of salary sacrifice arrangement may work differently depending upon the non-cash benefit.

Employees can also reduce costs by agreeing to sacrifice a portion of their salary for certain other government-approved benefits, such as use of an electric vehicle.

How large are the possible savings from salary sacrifice?

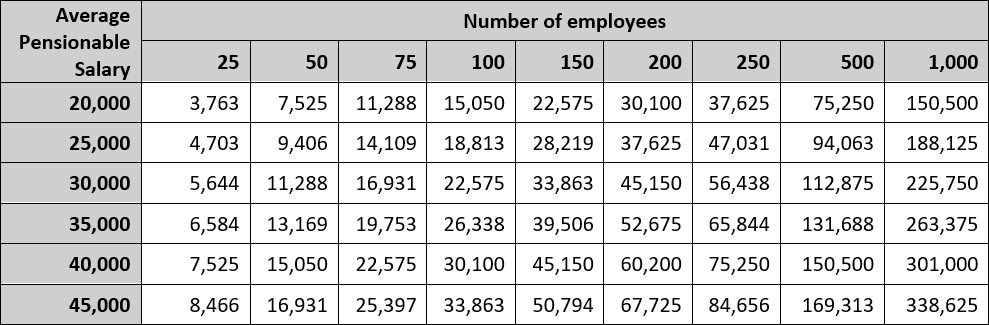

While salary sacrifice is simple in principle, the potential financial benefits to an employer are not as straightforward to quantify. The table below illustrates the potential annual savings to companies if all employees are eligible and take up salary sacrifice in exchange for pension contributions. It is based on employee contributions of 5% of pensionable salary and employer NIC rates (including the Levy) of 15.05% for the 2022/2023 tax year. If the employer pays an Apprenticeship Levy (which is 0.5% for the 2022/23 tax year) the savings will be increased.

It is a win-win situation; the greater the salary sacrifice, the better the employee’s potential retirement outcome and the larger the employer’s savings. If you consider that these are annual savings, they could be used to offset some, or all, of the cost of implementing a pension salary sacrifice arrangement. There are also many other ways that an employer could use these savings to benefit employees and their business.

The figures are not guaranteed and your exact savings will depend upon your specific circumstances. Savings in subsequent tax years will depend upon future NIC thresholds and rates, Government policy on salary sacrifice arrangements and whether or not the Levy will be included within the savings when it is established as a separate Levy from 2023/24 onwards.

Beyond pensions, even greater savings are potentially available if the employee also wishes to sacrifice salary for the use of an electric vehicle.

How should salary sacrifice be implemented?

The potential financial savings achieved from implementing a salary sacrifice arrangement can make it a highly worthwhile investment for your company and your employees, provided it is implemented correctly. There are many issues to consider, such as amending employees’ contracts of employment and issuing effective communications.

Our Pension Consultants can provide you with an initial consultation to determine the potential savings that you could achieve using salary sacrifice for pension contributions, and the number of your employees who could also benefit from such an arrangement.

Important Notes

This article is based on our current understanding of legislation, taxation and HMRC practice which may change in the future. It is intended for general information only and does not contain investment, financial, legal, tax or any other advice and should not be relied upon for this purpose. If you require advice based on your specific circumstances, you should contact a professional adviser.

SMEs can agree salary sacrifice arrangements with employees to help alleviate the worsening cost-of-living crisis.

Head of Corporate Benefits, Mercer Marsh Benefits