Government ‘invest for surplus’ consultation could herald reform of DB sector

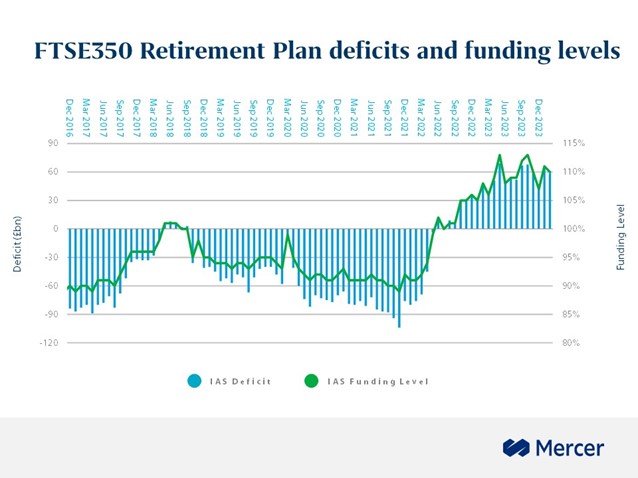

- Mercer analysis of FTSE 350 pension funds, shows an aggregate surplus across company accounts of £59bn at the end of February 2024, broadly staying level over the month.

- Government consultation has the potential to unlock surpluses to support employers’ businesses.

London – 14 March 2024

Mercer’s monthly analysis of FTSE 350 pension schemes shows an aggregate surplus which has persisted for almost two years. Mercer’s latest monthly analysis shows an aggregate funding level of 110% at the end of February 2024, falling only slightly from 111% at the end of January.

Mercer experts point to the newly launched government consultation on Options for Defined Benefit (DB) schemes. Launched on 23 February 2024, it explores some radical proposals which have the potential to unlock surpluses for employers with well-funded schemes. These challenge the concept that DB schemes’ central purpose is to pay the benefits promised to members.

The Government consultation aims to encourage schemes to 'invest for surplus' and to ‘bring surplus extraction in line with trustee duties'.

The rate of tax levied on refunds of surplus to sponsoring employers will be reduced from 6 April 2024, but the threshold for refunds to be paid remains high for the time being. This is one area the Government is looking at and the consultation proposes to lower the bar, in Mercer’s view a more critical piece of the puzzle.

Robbie Smith, Principal and policy expert at Mercer said:

“While we have historically high DB surpluses they will continue to be in the spotlight. The consultation has the potential to unlock surpluses to support employers’ businesses. The presence of a DB scheme on a balance sheet can often be seen as something which offers lots of risk and little reward, but that could be about to change.”

"The proposals could have far-reaching implications for DB schemes’ long-term strategies. For example, facilitating surplus access could encourage more use of run-on strategies over longer periods and a lower demand for insurance transactions.

“The questions being asked are less whether a surplus should be accessed, more when and how; this is likely to be contentious. While we can probably all agree that surplus assets should be put to use, what is equitable to members and sponsors? Conclusions will need to be reached on the threshold over which surplus extraction would be safe and then, who should benefit from any extraction. Trustees and sponsors of DB schemes might well have very different views on the answers to these questions.

“Although a switch to a Labour-led government later this year appears likely, its plan for financial services announced an intention which follows the current Government’s agenda around UK productive assets quite closely - this consultation shouldn’t be disregarded.”

The consultation is due to close on 19 April; Mercer will respond and monitor the outcome of this closely.

Background to the February analysis:

Bond yields and the market’s expectation for inflation both increased slightly over February. The funding position of the FTSE 350 pension funds on an accounting basis shows a slight fall surplus at the end of February according to Mercer’s Pensions Risk Survey data analysis for February 2024.

The analysis shows that the accounting surplus of defined benefit (DB) pension schemes for the UK’s 350 largest listed companies decreased to £59bn at the end of February 2024. The present value of liabilities increased from £597bn on 31 January 2024 to £603bn at the end of February 2024. Asset values increased from £661bn to £662bn at the end of February 2024.

Mercer’s Pensions Risk Survey data relates to about 50% of all UK pension scheme liabilities, with analysis focused on pension deficits calculated using the approach companies have adopted for their corporate accounts. The data underlying the survey is refreshed as companies report their year-end accounts. Other measures are also relevant for trustees and employers considering their risk exposure. Data published by the Pensions Regulator and elsewhere tells a similar story.

Notes to Editors

Mercer estimates the aggregate combined funded ratio of plans operated by FTSE350 companies on a monthly basis. This is based on projections of their reported financial statements adjusted from each company’s financial year end in line with financial indices. This includes UK domestic funded and unfunded plans and all non-domestic plans. The estimated aggregate value of pension plan assets of the FTSE350 companies at 31 December 2019 was £775 billion, compared with estimated aggregate liabilities of £815 billion. Allowing for changes in financial markets through to 23 February 2024, changes to the FTSE350 constituents, and newly released financial disclosures, the estimated aggregate assets were £662 billion, compared with the estimated value of the aggregate liabilities of £603 billion.

The FTSE350 funding data is generated by Mercer. It represents estimates of companies’ pension scheme funding positions using IAS19, one of the International Accounting Standards. Mercer uses data provided by London Stock Exchange Group.

About Mercer