Market volatility continues to benefit FTSE 350 pension schemes

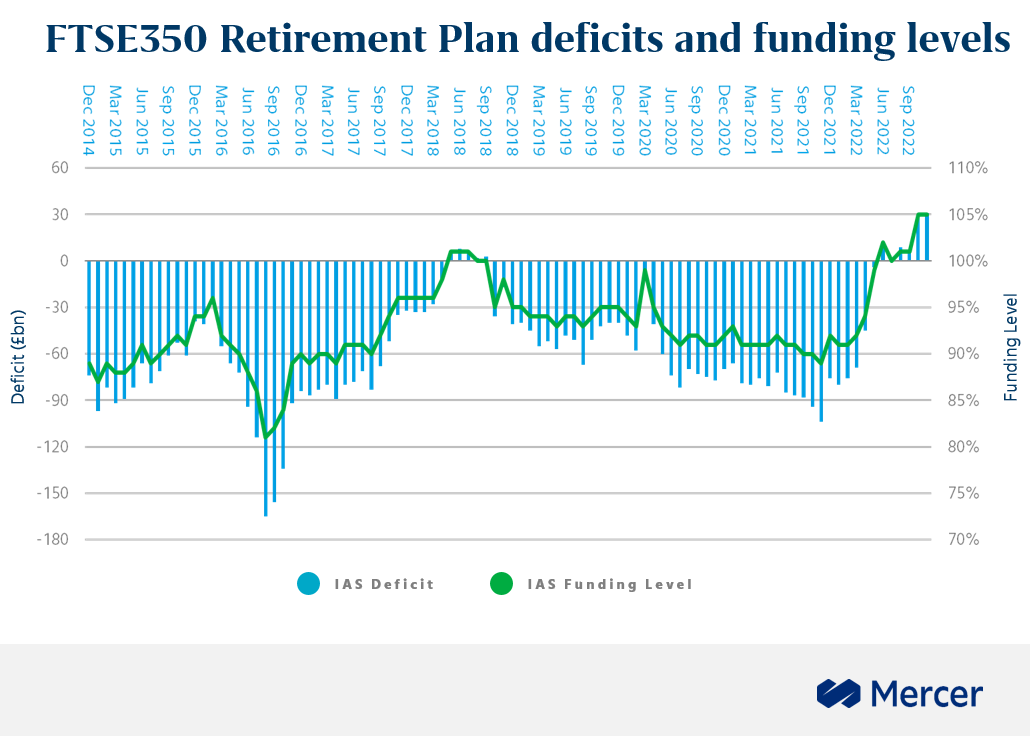

- Mercer’s FTSE350 analysis shows month-end surplus increasing from £5bn at end September to £29bn at end October, driven by asset outperformance versus liabilities

- October saw political changes and the reversal of many of the September “mini budget’s” planned measures, which led to a fall in bond yields and falling inflation expectations

- Trustees and employers may want to consider how they translate funding improvements into reduced risk, including accelerated plans to buy-out – insurer capacity being an increasing concern

- October also saw the release of inflation figures used for many pension scheme annual increases. Coupled with the strong improvements in funding positions this may see member expectations raised on discretionary pension increases

London, 03 November 2022

Mercer’s Pensions Risk Survey data analysis for October shows that the accounting surplus of defined benefit (DB) pension schemes for the UK’s 350 largest listed companies increased to £29bn at the end of October. Liabilities fell from £605bn at 30 September 2022 to £600bn at the end of October driven by a fall in future implied inflation expectations largely offsetting falling corporate bond yields. The reduction in bond yields was also positive for asset values, which increased over the period to £629bn compared to £610bn at the end of September.

Despite short term operational and liquidity issues arising from the events at the end of September, many schemes will have benefited from recent market volatility and may now be considering how they convert the funding gains into reduced risk investment strategies or how to implement risk transfer activities.

Matt Smith, Principal at Mercer said, “The aggregate funding position on an accounting basis has improved following the market turmoil at the end of September and the continued market volatility over October, settling at a surplus £29bn at the end of October.

“This may be the first time trustees and employers have been within touching distance of estimates of insurance pricing, and some may be underprepared. In a busy insurance market, schemes may be fighting for attention and well-run schemes may be exploring the growing range of options available to them.”

Trustees may wish to explore all available options. Rather than defaulting to buy-in and buyout as the only options, trustees might also consider that alternatives such as consolidators, master trust and low-dependency run-on may offer attractive benefits in a higher yield environment.

Mr Smith added, “October also revealed the September to September inflation figures which is used for many pension schemes to determine the next annual pension increase. Many schemes will have a cap on pension increases, resulting in members’ pensions eroding in real terms in the current high-inflation environment. Others may have no increase and in other cases, increases will be discretionary.

“Trustees and employers may come under increasing pressure from members to provide additional or discretionary increases in light of the increase in the cost of living. While various factors will influence decision-making on this point, it may be harder to justify not providing additional increases based on funding levels alone when some schemes may now see funding levels closing in on buyout.”

Mercer’s Pensions Risk Survey data relates to about 50% of all UK pension scheme liabilities, with analysis focused on pension deficits calculated using the approach companies have to adopt for their corporate accounts. The data underlying the survey is refreshed as companies report their year-end accounts. Other measures are also relevant for trustees and employers considering their risk exposure. Data published by the Pensions Regulator and elsewhere tells a similar story.

ENDS

Notes to Editors

Mercer estimates the aggregate combined funded ratio of plans operated by FTSE350 companies on a monthly basis. This is based on projections of their reported financial statements adjusted from each company’s financial year end in line with financial indices. This includes UK domestic funded and unfunded plans and all non-domestic plans. The estimated aggregate value of pension plan assets of the FTSE350 companies at 31 December 2019 was £775 billion, compared with estimated aggregate liabilities of £815 billion. Allowing for changes in financial markets through to 31 October 2022, changes to the FTSE350 constituents, and newly released financial disclosures, the estimated aggregate assets were £629 billion, compared with the estimated value of the aggregate liabilities of £600 billion.

Sample Data Points