Surprising Gender Gap in Health Benefits Persists

On an organizational level, pay and benefits generally go hand in hand: In companies where the workforce is highly paid, benefits tend to be richer. The converse is also true. In employer-sponsored health plans, employee paycheck deductions and cost-sharing requirements tend to be stiffer in companies with mainly low-wage workers. What makes this a women’s issue is that women disproportionally work in low-wage industries, and thus working women are more likely to struggle with health care affordability than working men.

We first analyzed the gender gap in benefit levels in 2014 and have revisited it several times since then. This year, as International Women’s Day approached, we performed the analysis with 2021 data to see what improvement, if any, the past three years have brought. Using data from Mercer’s National Survey of Employer-Sponsored Health Plans, we grouped employers with a predominately female workforce (65% or more female) and those with a predominantly male workforce (65% or more male), and compared benefits and policies across the two groups. The majority of the mostly-female companies are in the health care and services sectors, while the majority of mostly-male companies are in manufacturing. Here’s how these two groups compare across a few key areas:

Pay gap remains, with slight improvement. In 2018, we found that the average salary was significantly lower in mostly-female companies, with a difference of over $16,000. In 2021, the difference is still around $16,000, although between 2018 and 2021 the average salary rose somewhat faster in the mostly-female group (a 20% increase compared to 15% for the mostly-male group), helping to narrow the gap on a percentage basis.

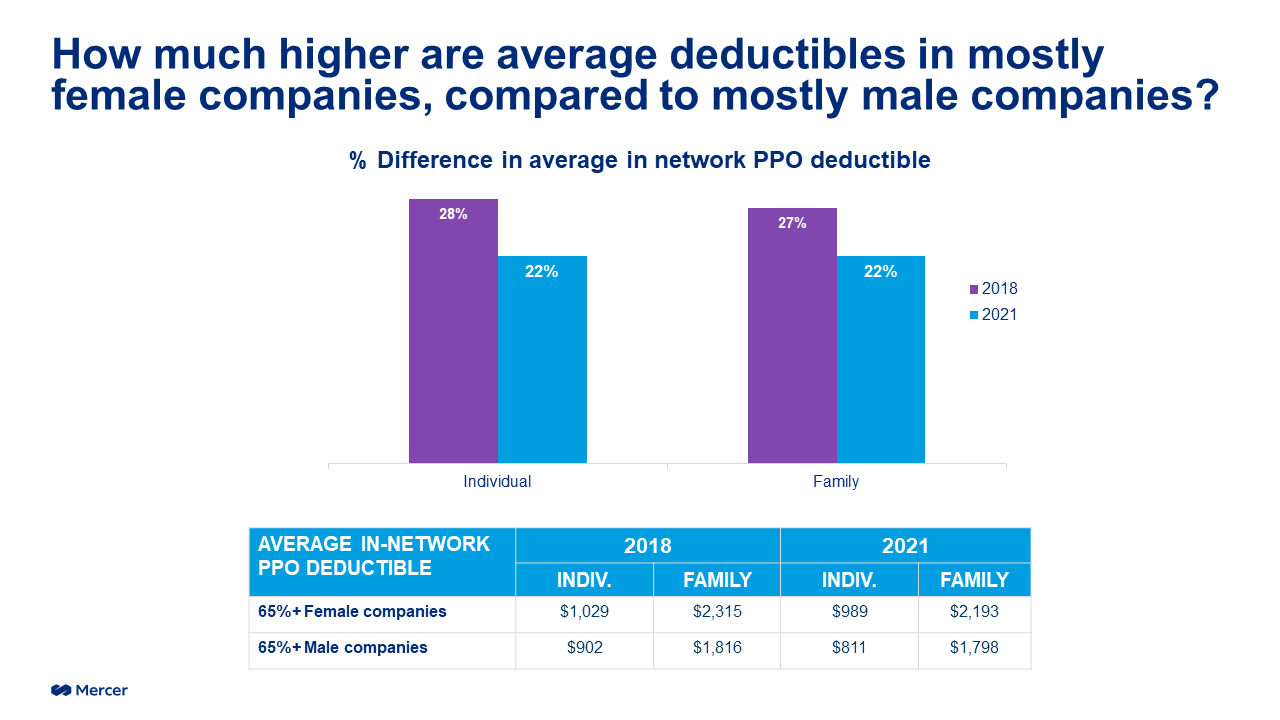

Employees in mostly-female companies still face higher deductibles and out-of-pocket maximums. Nearly all cost-sharing requirements are higher in the mostly-female group. Average in-network PPO deductibles in mostly-female companies are nearly $200 higher for individual coverage ($989) and about $400 higher for family coverage ($2,193). However, as shown in the graph below, the gap between the deductibles has narrowed somewhat. Out-of-pocket maximums are also higher, by about $500 for individual coverage ($3,850 on average) and about $1,000 for family coverage ($8,144 on average).

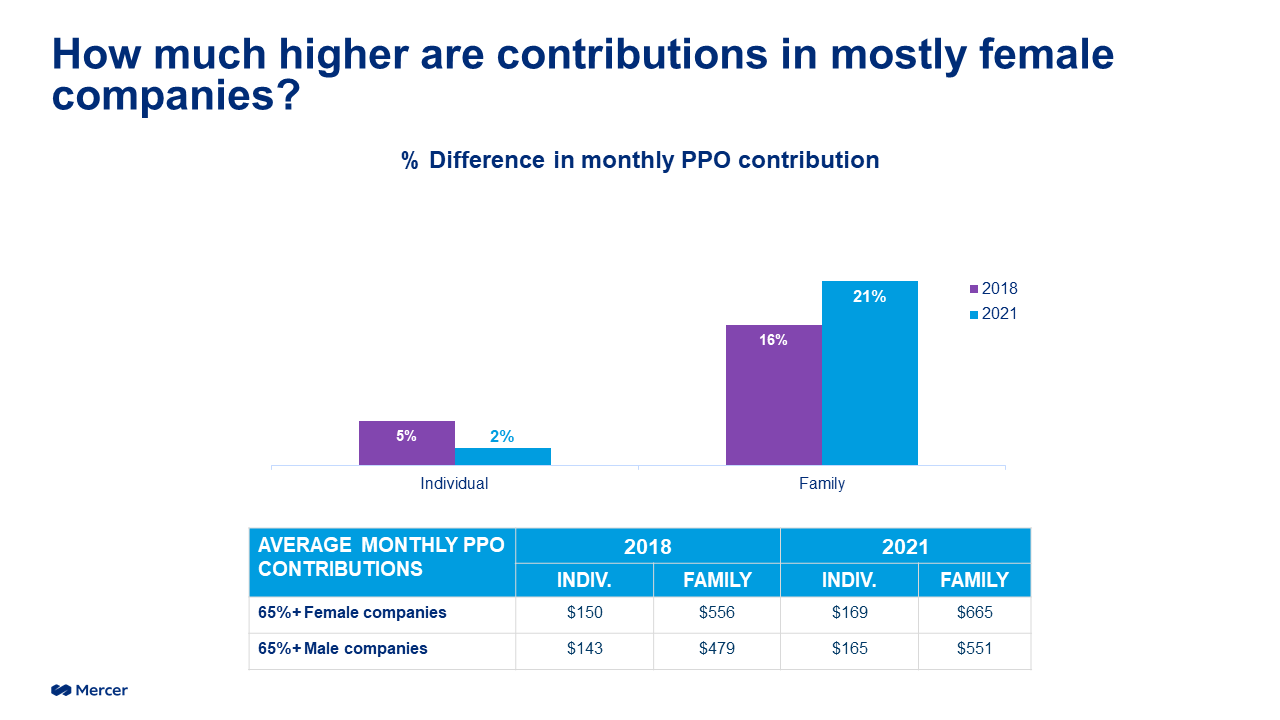

And the difference in contributions doesn’t stop at medical coverage – employees in mostly-female companies also pay more for dental coverage. As we’ve seen with medical plans, these higher contributions purchase a lower level of coverage; the annual dental plan cost per employee averages $774 in mostly-female companies but $874 in mostly male companies.

Waiting periods for health coverage. Mostly-female companies are more likely to impost a waiting period for coverage for newly hired full-time employees (43% do so) than mostly-male companies (31%). The gap is even wider for when it comes to coverage for newly hired part-time employees.

Momentum for faster change?

Amid the current labor shortage and tough competition for talent, offering an attractive benefit package is critical – and employees value the health benefit more highly than any other. Some of the industries that have been hit hardest by labor shortages are those that employ a lot of women, such as retail, hospitality and – especially – health care. According to Mercer’s 2021 National Survey, 74% of the employees in large health care organizations are female. As employers with largely female workforces seek to enhance their retention and recruitment efforts, many are looking to improve health care affordability for their employees. For organizations operating with tight margins, finding ways to manage health care cost without shifting cost to employees is no easy task. But while there is no one silver bullet, there are plenty of strategies that can make a difference. Over the past few years, we have seen some very large employers that offered only a high-deductible plan add plan choices with lower deductibles. Employers are also adding virtual care options – particularly for behavioral health care – that are less expensive and more convenient than in-person care. Onsite clinics can lower out-of-pocket costs for employees and reduce medical plan costs for employers. Voluntary benefits, such as critical care insurance or hospital indemnity plans, can fill coverage gaps. No-deductible plan designs, such as a copay-only plan, can make it easier for workers without savings to access care.

Women who left the workforce during the pandemic and have not yet returned may need a better value proposition from employers, and the health benefit is a great place to start. In the spirit of International Women’s Day, let’s recognize the extra burden on women workers and take meaningful action to help #breakthebias.

About the analysis

Using data from Mercer’s National Survey of Employer-Sponsored Health Plans 2021, we grouped employers with a predominantly female workforce (65% or more) and those with a predominantly male workforce, and compared benefits and policies across the two groups. The analysis was limited to employers with 500 or more employees. There were 217 organizations in the predominantly female group and 419 organizations in the predominantly male group.