Drug copay accumulator programs: A many-sided argument

While we used to find more of a mix of therapy purposes and price points, today the drug pipeline comprises high-cost biologics, brand-name and specialty drugs. Though these drugs can be life-enhancing and even lifesaving, they can also have significant impact on prescription drug costs for the member and the group health plan.

To help health plan members afford higher-priced drugs, pharmaceutical manufacturers often provide members with direct financial support through copay coupons or other methods that reduce and sometimes eliminate all out-of-pocket costs for that drug. Examples are as close as your TV screen. Often, a drug commercial will communicate that financial assistance is available for members with insurance.

This direct financial support helps members afford expensive drugs by reducing the amount of their out-of-pocket costs. Traditionally, the amount of the financial assistance would also be applied to the member’s deductible and out-of-pocket maximum. The manufacturer would continue to charge the plan its normal share of the drug cost.

Plan design features like copays and deductibles give members some skin in the game. Manufacturer financial assistance significantly reduces or eliminates that skin – those members have little or no incentive to try lower-cost therapies that could be as effective.

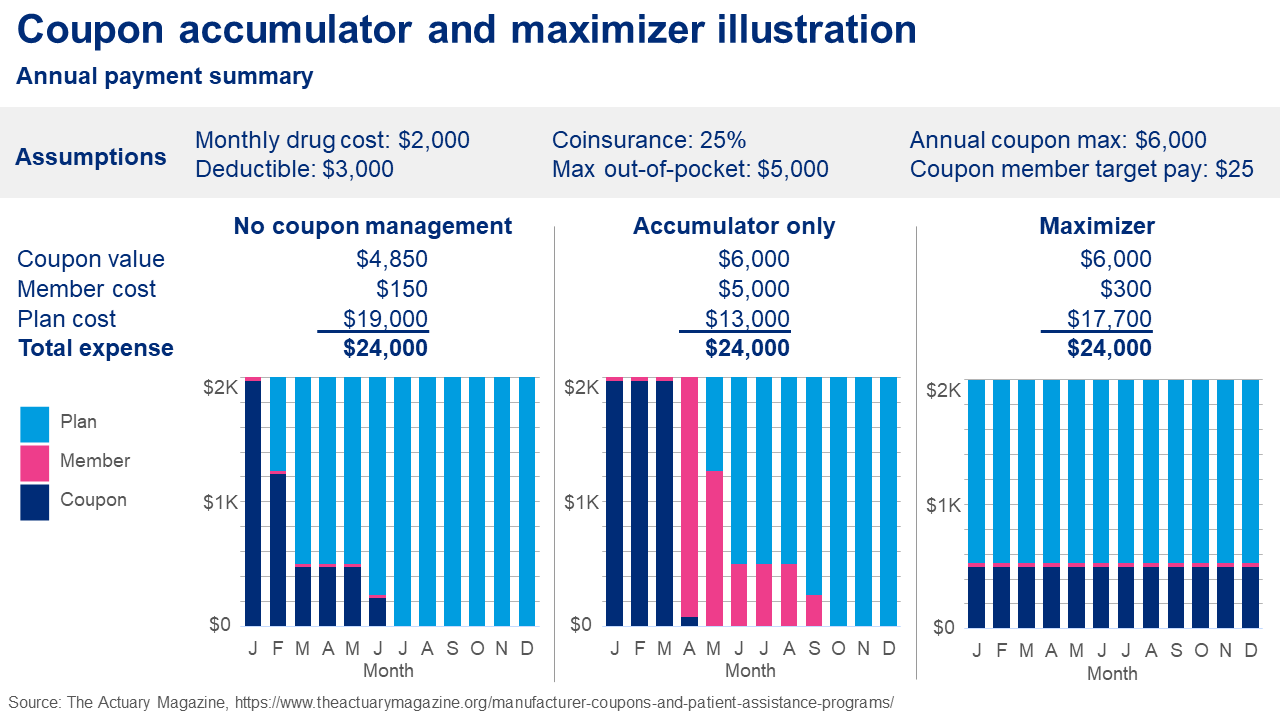

PBM response to manufacturer financial assistance programs

To address this issue, PBMs began offering co-pay accumulators and maximizer programs. These programs are popular – over 70% of plan sponsors use them. Program specifics vary, but they all have two common features: the member may use the manufacturer financial assistance, but the assistance generally does not count toward the annual plan deductible or OOP maximum.

Early versions of these co-pay accumulator programs were unpopular with members. That’s because most manufacturers’ financial assistance has an annual limit, so when a member – often unknowingly – hit the limit during the plan year, the next refill could be very expensive if the plan’s deductible and OOP maximum had not yet been met. Later versions addressed this issue by spreading the manufacturer assistance over the plan year.

Member pushback

Patient advocacy groups have noticed the high adoption rate of copay accumulator programs and have let their state legislators know about it. Currently, 19 states (and Puerto Rico) have enacted legislation requiring fully insured plans to count third-party financial assistance toward a member’s cost sharing. These state laws do not apply to ERISA-covered self-funded plans.

Three major patient advocacy groups—HIV and Hepatitis Policy Institute, Diabetes Leadership Council, and Diabetes Patient Advocacy Coalition – sued the Department of Health and Human Services (HHS), challenging a regulation that effectively allowed fully insured and self-funded group health plans to adopt copay accumulator programs that disregard drug manufacturers’ financial assistance from accumulating to a plan’s deductible and out-of-pocket maximum. The court directed the regulators to rewrite the regulation. As of now, the circumstances under which plans and insurers may still use copay accumulators, if at all, are unclear.

Separately, counting third-party financial assistance toward deductibles creates an issue for heath savings account (HSA)-qualifying high-deductible health plans (HDHPs), as the regulators acknowledged in prior regulations. If the government (HHS) does not appeal this decision, then it’s possible that a prior version of their regulation will be back in effect, under which plans and issuers will only be able to use copay accumulators for branded drugs if the drug has an available and medically appropriate generic equivalent, and for fully-insured plans if permitted under state law. And in that case, there’s an unresolved HSA/HDHP compliance issue to address. The case is currently pending.

These developments are a major issue for the many plan sponsors who have adopted copay accumulators to control plan costs. Members on high-cost drugs who receive financial assistance are better off without copay accumulators, but all health plan members may see higher employee contributions if plan costs rise as a result.

What’s next?

The role of manufacturer financial assistance will continue to be debated. Some see assistance as helping members stay on physician-directed therapy while others feel they keep prices high for everyone. To the extent a new law or regulation requires third-party assistance to count toward the member’s deductible and OOP maximum, that would impact the viability of copay accumulators.

Regardless, manufacturers are looking at the funds they provide in rebates and financial assistance, and their approach going forward may be determined as much by shifting economics as by the actions of regulators or state legislators.