When performance shares aren't performing

How to address “nonperforming” performance shares in uncertain times

Assessing the situation

Companies considering action should evaluate the business case, including the following:

-

Number of shares remaining in stock plan reserves

-

Number of performance cycles affected and their scheduled end dates

-

Likelihood of achieving at least threshold performance under various performance scenarios

-

Whether current performance goals are absolute or relative, and whether awards already include a discretionary component

-

Level and number of employees affected

-

Status of other outstanding equity and cash awards

-

Whether broader workforce actions have been taken, such as pay cuts, layoffs, furloughs

-

Likely reaction of proxy advisers and investors

-

Regulatory implications

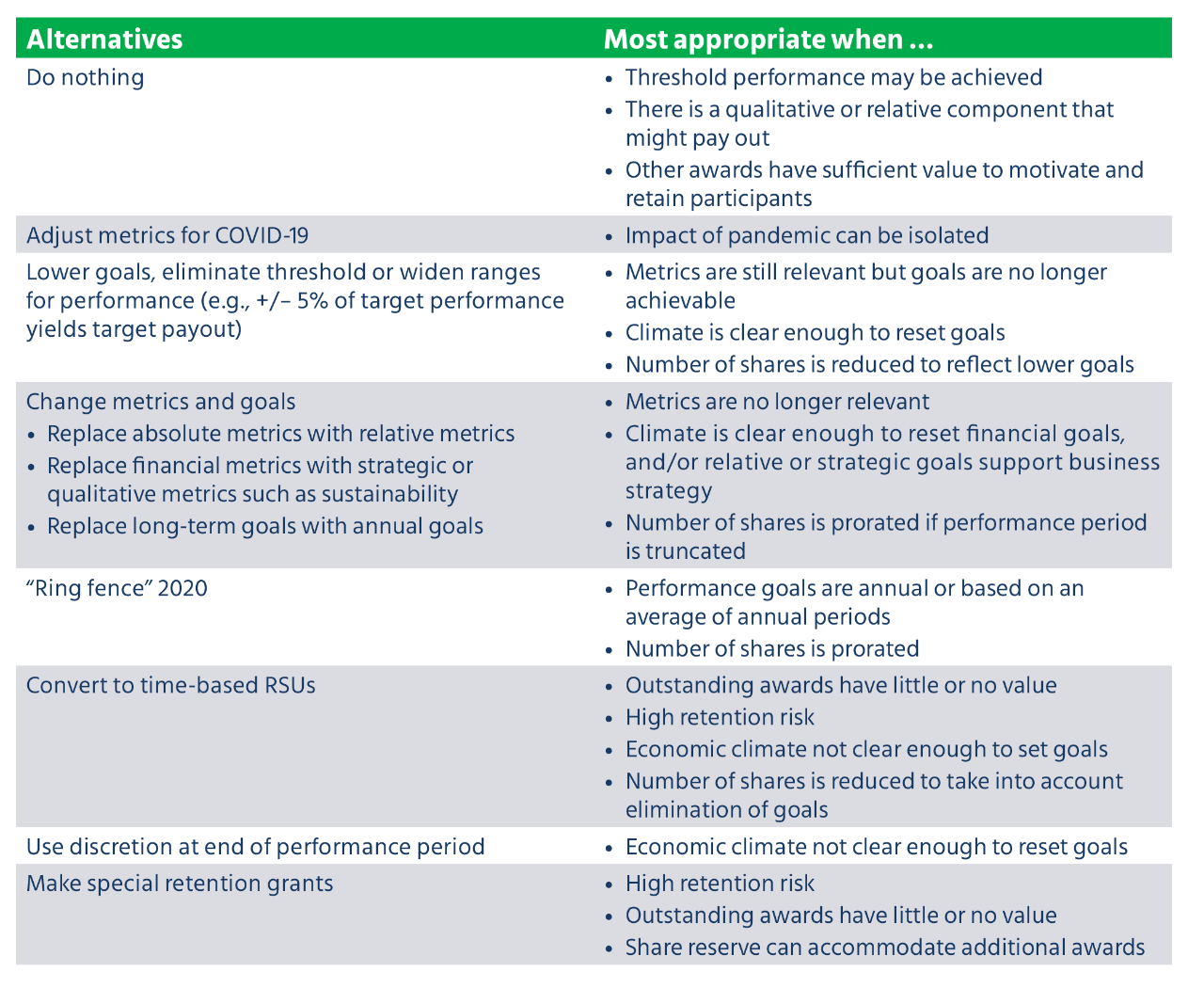

Strategies for nonperforming awards

Proxy adviser views

ISS

Glass Lewis

Glass Lewis cautions against executive pay changes that are inconsistent with the challenges workers are experiencing and is most likely to support changes that “take a proportional approach to the impacts on shareholders and employees”. The proxy adviser warns against “maintaining or even increasing executive compensation levels” and cautions that trying to make executives whole is a “certainty for proposals to be rejected and boards to get thrown out — and an open invitation for activists and lawsuits onto a company’s back for years to come.”

Regulatory considerations

Before changing in-progress performance shares, companies should consider the following plan document, accounting, disclosure, tender offer and tax issues.

Plan documents

Companies should also review documents for the following:

-

Are there any restrictions on discretionary modifications or replacements?

-

Is participant consent required?

-

Will cancelling awards or converting stock-settled awards replenish the share reserve?

-

Will additional grants exceed the available share reserve or any plan individual limits?

Accounting

The accounting treatment of discretionary performance share cancellations, modifications, and replacements differs for awards with nonmarket (e.g., EPS or sales targets) vs. market performance conditions (e.g., TSR). Automatic adjustments that are set out in the plan (“the committee shall adjust for …”) generally have no impact on compensation expense.

Nonmarket conditions. Companies recognize no cost for performance shares that are improbable of vesting or cancelled. Instead, companies must recognize any incremental cost associated with a modified or replacement award. The incremental cost is calculated by comparing the fair value of the award immediately pre- and post-modification. If an award is improbable of vesting or cancelled, the pre-modification fair value is zero and the post-modification value equals the new number of shares expected to vest (typically target) multiplied by the per-share fair value on the modification date. The final cost is trued up for the number of shares that actually vest.

Market conditions. The cost of a performance share with a market condition must be recognized regardless of the outcome or whether the award is cancelled, as long as the employee completes the award’s original service requirement. In addition, companies have to recognize any incremental cost associated with a modified or replacement award. The incremental cost is calculated by comparing the fair value of the award (using a Monte-Carlo simulation incorporating the probability of achievement) immediately pre- and post-modification.

Disclosure

All of the strategies (except do nothing) would trigger executive pay disclosures.

Proxy statement. Generally, the proxy statement Summary Compensation Table (SCT) presents equity awards using the accounting grant-date fair value. Any incremental accounting cost arising from a discretionary modification to, or cancellation and replacement of, awards held by the proxy named executive officers (NEOs) is reported in the SCT and Grants of Plan-Based Awards Table in the year in which the change is made. If the original grant and the modification occur in the same year, this will result in “double” disclosure because the grant date fair value of the original award must also be reported — reflecting two compensation decisions made in the same year (CDI 119.21). (If the original award was granted in a prior year, the original grant date value would already have been reported.) Any action taken should be explained in the Compensation Discussion and Analysis section of the proxy.

Financial statements. Under ASC Topic 718, material modifications in any year presented in the P&L must be discussed in the notes to the company’s financial statements.

Real-time disclosure. If NEO awards are affected, a Form 8-K filing might be required or prudent. While modifying performance goals generally doesn’t require a filing, ISS urges real-time disclosure of the changes and supporting rationale.

Section 16 Form 4 filings. Generally performance shares don’t need to be reported by Exchange Act Section 16 officers until vesting. However, the award must be reported at grant if it vests based solely on achievement of an absolute (not relative) stock price goal or, for a company that pays no or nominal dividends, a TSR goal. If an award with a stock price goal is modified (or an award is modified to add a stock price goal), the modification might trigger a filing.

Employee consent, tender offer rules

Tax

The 2017 tax law changes to Section 162(m) have given companies more flexibility to adjust awards without adverse tax consequences. But companies still need to consider the following:

Loss of Section 162(m) grandfather. If the original awards are grandfathered (granted under a written binding contract in effect on Nov. 2, 2017 that hasn’t been materially modified), modifying goals or replacing awards might be a material modification. If so, amounts earned by “covered employees” would be subject to the $1 million deductibility cap.

Section 409A. Assuming the time and form (e.g., installment or lump sum) of payment originally in place isn’t changed, simply modifying performance goals shouldn’t have 409A implications. But, for example, if the modified award has a longer performance period than the original award, there may be some 409A risk even if each award was designed to meet the short-term deferral exemption. Under 409A, a replacement award could be treated as extending the original forfeiture period (creating a “rolling risk” of forfeiture), with the net effect an impermissible 409A deferral.