Retirement Income for US DC Plans: Point of View

09 May 2025

The retirement income landscape can be overwhelming given the wide array of investment products and solutions available.

Over the last decade, there has been a dramatic shift in the role played by defined contribution (DC) plans in the US retirement landscape. Initially, DC plans were intended to be a supplemental savings vehicle complementing defined benefit (DB) plans and social security benefits in providing income streams to participants in retirement.

However, as DB plans have gradually diminished, the responsibility for generating retirement income has shifted from plan sponsors to plan participants. Many Americans now face the dual challenge of saving for retirement and converting those savings into a sustainable income stream for their later years. Simultaneously, retirees are confronting myriad potential demands on that income stream – from supporting multiple generations to inflation to longevity.

In light of this evolving dynamic, we believe plan sponsors should take proactive steps to ensure their retirement plans are equipped to address the challenges of providing income throughout retirement.

The retirement income landscape can be overwhelming given the wide array of investment products and solutions available, many of which are complex and unproven at this point. Retirement income solutions also encounter several challenges in adoption, such as fees (both implicit and explicit), integration with recordkeepers, and effectively communicating product offerings to participants, among others. Compounding these difficulties is the reality that no single solution is likely to meet the diverse needs of all participants, as individuals have varying goals, risk profiles, and longevity expectations.

Therefore, plan sponsors undertaking this objective must be prepared to take a multi-pronged approach. This approach can leverage existing investment options available to participants, utilize services and advice provided by the plan’s recordkeeper, and if necessary, consider adding dedicated investment options from which participants can choose.

Multi-Pronged Solution – Not One Size Fits All

A one-size-fits-all solution will not satisfy the diverse needs of every participant. The term "retirement tier" encompasses a range of options, from simple measures (such as allowing participants to remain in the plan after retirement and take partial withdrawals) to more comprehensive offerings that include a mix of tools, resources, advice and solutions. Before introducing a "retirement tier", plan sponsors should assess the existing resources available to support participants in converting their accumulated assets into retirement income. The key is to provide offerings that resonate with retirees and near-retirees, ensuring that the solutions are clear, engaging and relevant. Without this, the proposed solutions are unlikely to gain traction among participants. Therefore, effective communication strategies are critical in driving the use of retirement income solutions.

An approach to retirement income may include one, or all, of the categories below, depending on the objectives and investment philosophy of the plan sponsor.

Understand – then (Consider) Action

-

Set objectives on retirement income solutions in the DC plan

The first step in exploring retirement income solutions is to establish a set of guiding objectives. By clearly outlining beliefs, the fiduciary committee (committee) develops a philosophy regarding retirement income solutions. They should consider whether offering retirement income solutions aligns with their goals, identify the specific participants they aim to reach, and define their objectives in supporting retirees. Mercer recommends facilitating a discussion with the committee that addresses several important topics.

Key Questions to Consider:

- How much does the committee feel the DC plan should help participants generate retirement income?

- Does the committee wish to retain terminated employees in the plan?

- Are there any talent acquisition or retention goals that could be supported through retirement income offerings in the DC plan?

- Who should the retirement income offerings be developed for? Are there different goals in mind for the medium term versus the long term?

- How much time and expense does the committee want to dedicate to retirement income?

- What are the committee’s goals in supporting retirees?

- Does the committee’s fiduciary responsibility increase with a change in objectives, and in what ways? Is the committee comfortable with any additional fiduciary exposure?

As solutions are evaluated, it is important for the committee to keep their key objectives in mind and consider how each solution aligns with the established framework.

-

Analyze the plan’s demographics to understand savings and withdrawal behavior, specifically near or in retirement yearsIt is critical for plan sponsors to conduct a demographic analysis to gain a comprehensive understanding of how participants use the plan both leading up to and during retirement. Key metrics to evaluate include age distribution, asset allocation, the ratio of active to inactive participants, average account balances, tenure/turnover, and withdrawal behavior after terminating employment or retiring. By understanding participant utilization, plan sponsors can make more informed decisions about which retirement income features or solutions best align with the needs of their defined contribution plan.

-

Review current plan design options and explore additional recordkeeper tools and resources

A thorough review of existing solutions is crucial. Plan sponsors should assess their objectives against the current offerings in their defined contribution (DC) plan design, evaluating what features are already enabled for participants and whether they are being utilized effectively. This includes promoting available features more effectively and determining if there are additional plan design elements that can be activated to enhance participant access.

Retirement income options can include various tools and resources, such as Social Security optimization, retirement planning and projections, targeted communications, and plan design features that facilitate systematic or partial withdrawals. The design features and services provided by the recordkeeper can play a crucial role, as they often come at little or no extra cost and are seamlessly integrated into the recordkeeping platform, promoting familiarity and ease of access for participants.

As a starting point, Mercer believes that plan sponsors should offer flexible withdrawal options, such as partial and systematic withdrawals, to allow participants the option of accessing their balance without taking a full distribution.

Advice services are also critical, including managed accounts, income advice services, education services, and financial coaching or Employee Assistance Programs (EAPs). These personalized advice tools are often highly customizable and provide comprehensive resources to help participants set income goals, determine suitable asset allocations, and develop withdrawal strategies. Integration with recordkeeper services is vital, as an option’s availability may be influenced by the recordkeeper's capabilities. Evaluating whether messaging is consistent and tools are directionally aligned between the recordkeeper and point solutions is also critical. Ultimately, it is essential to ensure that the solutions offered are relevant to participants, encourage engagement, align with the plan sponsor's objectives for achieving their goals, and are evaluated with the proper lens to the extent that the solution is of a fiduciary nature (e.g. managed accounts).

-

Understand the retirement income product landscape and identify the solutions that best align with plan objectives, current design and recordkeeper integration

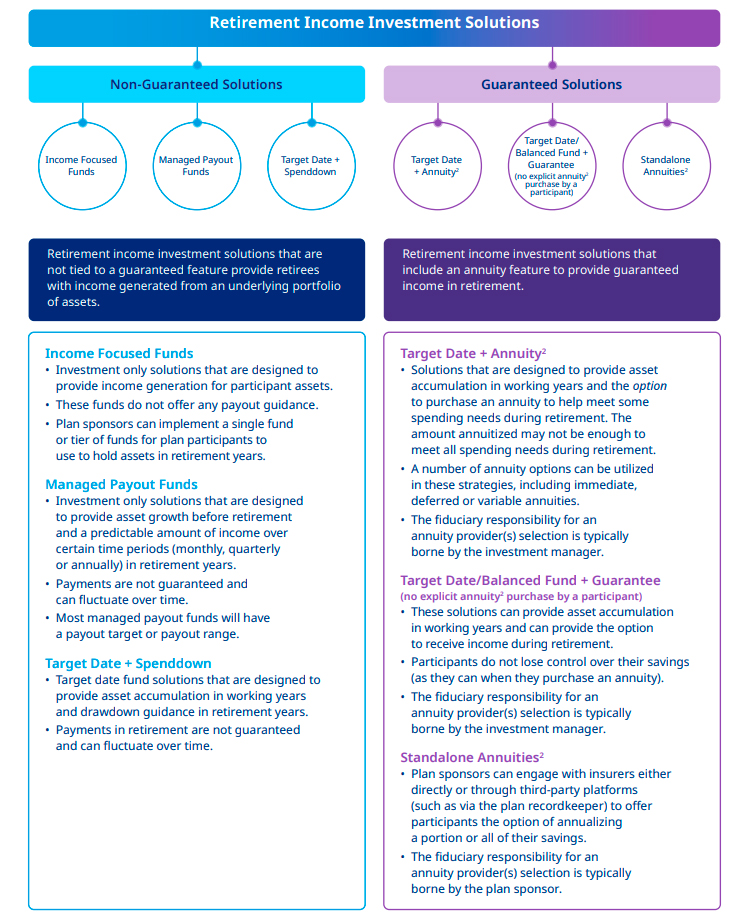

Once all these steps have been completed, a plan sponsor may consider incorporating an investment solution into the plan. Mercer believes that most fiduciaries currently incorporate the essential investment components for the retirement tier in their plans, including target date funds, stable value options and managed accounts. These solutions are familiar to participants and simplify understanding and oversight by avoiding additional layers of complexity. A key aspect of this strategy is effectively communicating their benefits to plan participants as a decumulation vehicle.

In recent years, investment managers have developed a diverse array of guaranteed and non-guaranteed income solutions designed to meet the investment and spend-down needs of retirees. Guaranteed solutions include an annuity feature that offers retirees varying levels of guaranteed income in retirement. Non-guaranteed solutions are investment-only solutions that may provide drawdown advice in retirement years. As plan sponsors take inventory of the current retirement income options they have in place, these guaranteed and non-guaranteed investment solutions may be appropriate to address specific gaps or needs. Mercer supports both annuity-backed and investment-only retirement income options; however, they may not be suitable for all defined contribution plans at this time. It is essential to address significant hurdles and considerations on a case-by-case basis, keeping committee philosophy, participant demographics, solution complexity, and recordkeeper integration and portability in mind. Additionally, investment option evaluation should consider how the solutions will address other key factors, including longevity risk, market risk, personalization, and fees.

Conclusion

Retirement income solutions can play a vital role within defined contribution plans and plan sponsors should consider incorporating plan design and investment solutions. Plan sponsors who have yet to embark upon retirement income education and objective setting may find themselves falling behind in the near future.

In summary, Mercer believes:

Plan sponsors should define their objectives for offering a retirement income solution. Analyzing participant demographics and assessing employee needs is a critical part of this process.

- Communication is the most critical aspect of facilitating and supporting participants’ transition into retirement and standard communications have notable room for improvement.

- Plan sponsors should provide flexible withdrawal options, like partial or systematic withdrawals.

- Most fiduciaries already offer the critical building blocks of the investment portion of the retirement tier in their plans, like target date funds, stable value and managed accounts.

- Annuity-backed investment options can play a role in decumulation, but they are probably not appropriate for all DC plans at this time. Significant hurdles and considerations need to be addressed on a case-by-case basis.

- Plan sponsors must understand the potential risks, solution complexity and additional responsibilities they may face and the risks for participants if a new solution is offered. Education on retirement income may lead some plan sponsors to conclude that offering a new retirement income solution is not warranted for several reasons, such as a sponsor’s unwillingness to assume additional responsibility and fiduciary risks, disinclination to offer a complex solution, and potentially unknown risks for the participants.

Participant retirement success is dependent on careful and thoughtful collaboration with recordkeepers. Retirement income is no different. Any discussion about retirement income should start with a thorough understanding of the current capabilities and limitations of the recordkeeper. Mercer believes a multi-pronged approach may be necessary for most DC plans to meet the diverse needs of all participants.

Retirement Income for DC plans

1 Guaranteed refers to investment solutions that have an embedded annuity component. Any guarantees are subject to the claims-paying ability of the annuity provider and should be carefully evaluated.

2 Annuity guarantees are subject to the claims-paying ability of the issuing insurance company.