Revisiting 417(e) stability and lookback periods

In 2024, the IRS issued final regulations regarding anti-cutback rules under 417(e).

Introduction

In 2024, the IRS issued final regulations regarding anti-cutback rules under 417(e). A key aspect of these final regulations stipulates that a plan can change the lookback and stability periods used to determine lump sums under 417(e) if the greater of the old and new provisions is provided for a period of one year. The “stability period” refers to the period of time a particular set of interest rates under 417(e) is used before being reset to more recent interest rates. This period ranges from one month to a year. The “lookback period” refers to how many months prior to the beginning of the stability period the plan looks back to apply the applicable interest rates, and this varies from the month prior to five months before the start of the stability period1. For example, a plan with a calendar year stability period can look back to use the rates for any month from August through December.

Plans that pay ongoing lump sums often set their lump sum lookback and stability periods many years ago, when 417(e) regulations were modified as part of the Pension Protection Act of 2006, and they may not have revisited them since the original election. With the final IRS regulations, plan sponsors now have an opportunity to revisit this feature of their plans, and changes may be appropriate in some cases.

Generally speaking, paying lump sums using a long stability and lookback period has been administratively more efficient and may not have resulted in a significant impact on funded status outcomes when interest rates were declining or relatively stable. However, with increases in the fixed income asset allocations and higher interest rate hedging targets, and higher levels of rate volatility, the time lapse between when rates lock in and when assets are liquidated to pay lump sums has the potential to introduce more material gains or losses. This may be a motivation to shorten the stability and lookback period.

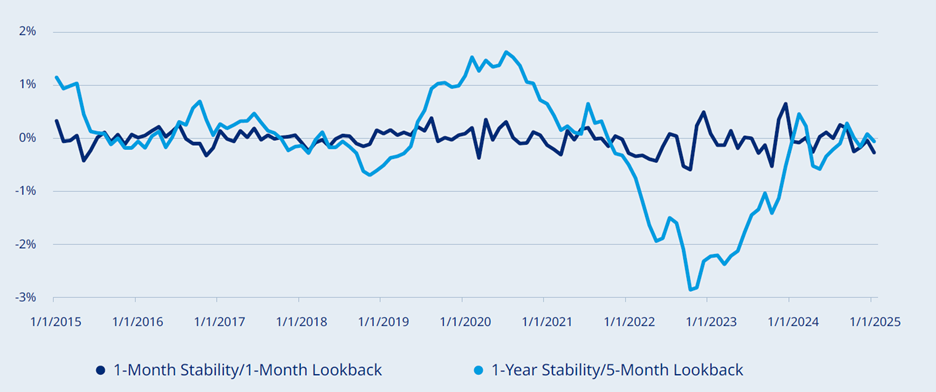

Historical variation of 417(e) interest rates and impact on relative lump sum values

Figure 1. Difference between two different stability/lookback period methods and spot bond yields over the past ten years

A closer look at the plan level impact of different stability and lookback periods

Over the long term, having a relatively long stability period may be fairly neutral in terms of paying lump sums that are more or less than current market values. However, there is the potential for large disconnects when bond yields move significantly in one direction during a year, similarly to 2022. In this scenario, liability and funded status losses occurred when lump sums paid to participants were greater than the market values and the corresponding liability release. There are many other variables that can lead to gains and losses in the future, including the overall asset allocation (return seeking versus liability hedging assets) and market performance, the interest rate hedging ratio, the amount of lump sums paid, participant behavior, demographic and assumption changes, and the gain or loss from lump sums may or may not be material. Nevertheless, having a shorter stability and/or lookback period may help reduce some of the variability.

Plans that pay ongoing lump sums and significantly hedge interest rate risk using LDI strategies may be surprised by the level of asset liability mismatch that could occur with a long stability and lookback period. The reason for this mismatch is that when a plan hedges most of its interest rate risk, its assets respond to changes in bond yields to match liability changes based on spot rates. When lump sums are paid each month based on interest rates from several months to over a year ago, this results in a gain or loss in funded status depending on the direction of rate changes. In a rising rate environment, there is an unfavorable situation where lump sums are valued at older, lower interest rates, producing higher lump sum payments relative to the current market pricing of the assets that need to be sold to make the payment. The opposite may occur in a falling rate environment.

Figure 2 illustrates the funded status implications for a plan hedging 100% of its interest rate risk under the three different 417(e) elections in a rapidly rising interest rate environment (2.5% over one year). The first scenario illustrates the impact on funded status if lump sums were valued using current 417(e) rates; the second scenario shows the impact of using a one-month stability period with a one-month lookback; and the last scenario shows a 12-month stability period with a five-month lookback.

Figure 2. Illustration of potential funded status impact under three 417(e) interest rate scenarios: spot rates, one-month stability and one-month lookback periods, one-year stability period, and five-month lookback

This illustration shows the potential asset liability mismatch using a long stability and lookback period in a rising rate environment. While 2022 was a particular outlier over the past 10 years, the experience highlights a potentially overlooked risk exposure for plans otherwise well-positioned to manage funded status risk through LDI strategies.

More and more plans have adopted de-risking strategies aimed at managing funded status volatility and limiting risk through a reduction in equity exposure, an increase in liability hedging assets, and an increase in interest rate hedge ratios. In the previous example, plans that were also hedging substantial rate risk saw their assets decrease along with their liabilities in 2022, when rates rose substantially. This would normally not be a concern, but problems arose when plans had permanent lump sum features and long lookback and/or stability periods. These plans saw asset values decline, but were paying lump sums based on much lower interest rates, leading to a compounding effect on asset losses. Some plan sponsors with savvy populations also saw an increase in lump sum elections with participants rushing to take potential advantage of the arbitrage opportunity (and in some cases, even terminating employment to do so) before the new higher rates took effect.

Approaches to manage stability and lookback period issues

For plans with a very long stability and lookback period, one approach to mitigate asset liability mismatch is to liquidate assets equal to the expected lump sums to be paid during the next stability period once the interest rates are set. These assets are held in cash and are no longer interest rate sensitive, similar to the lump sum payments. However, this strategy is subject to participant behavior risk in that actual lump sums are likely to vary, and history shows that participants tend to act in their own favor. As a result, in a rising rate environment, participants tend to be more likely to elect a lump sum, leading to actual lump sums being greater than expected, and the opposite can occur under a declining rate environment. So, while this strategy can be effective, there is still a risk that an asset liability mismatch persists and is exacerbated when rates move significantly in one direction during a year.

Minimizing the stability and lookback period is a better approach to potentially reduce gains and losses associated with lump sum payments. The minimum stability and lookback period is subject to plan administration constraints. A one-month stability and a prior-month lookback period is unlikely to be feasible based on when the interest rates are published, so plans would need to closely examine their specific situation to determine what can be implemented in practice.

These issues primarily affect plans paying permanent lump sums. Plans with a temporary period for electing lump sums or those that offer windows have less risk with respect to their stability and lookback periods, because they are able to control the timing of lump sum payments and the liquidation of hedging assets. However, where the temporary period associated with offering lump sums is associated with a plan termination and the timing of payments is not as flexible, the same issues can arise.

Summary

The final regulations issued by the IRS present plan sponsors with the opportunity to revisit and potentially optimize their lump sum stability and lookback periods for plans that pay ongoing lump sums. Plans with long stability and lookback periods have an ongoing risk of a mismatch between lump sum payments made and the market liability released upon distribution.

Plans that may be particularly surprised by the potential asset liability mismatch due to their elected lookback and stability periods are those that have implemented LDI strategies and may consider themselves “fully de-risked”, hedging 100% of their interest rate risk. These plans may consider themselves immune to interest rate risk, but a long stability and lookback period could present a hidden or overlooked risk.

Since there is a one-year period where plans are required to offer the better of their old and new stability and lookback periods, it would be prudent to explore the impact of potential changes now rather than wait and see. In many cases, it may be more advantageous to maintain the optionality of changing in the future, but it will vary on a plan-by-plan basis.