Why It May Be Getting Harder to Move Employees into CDHPs

Mercer

Mercer

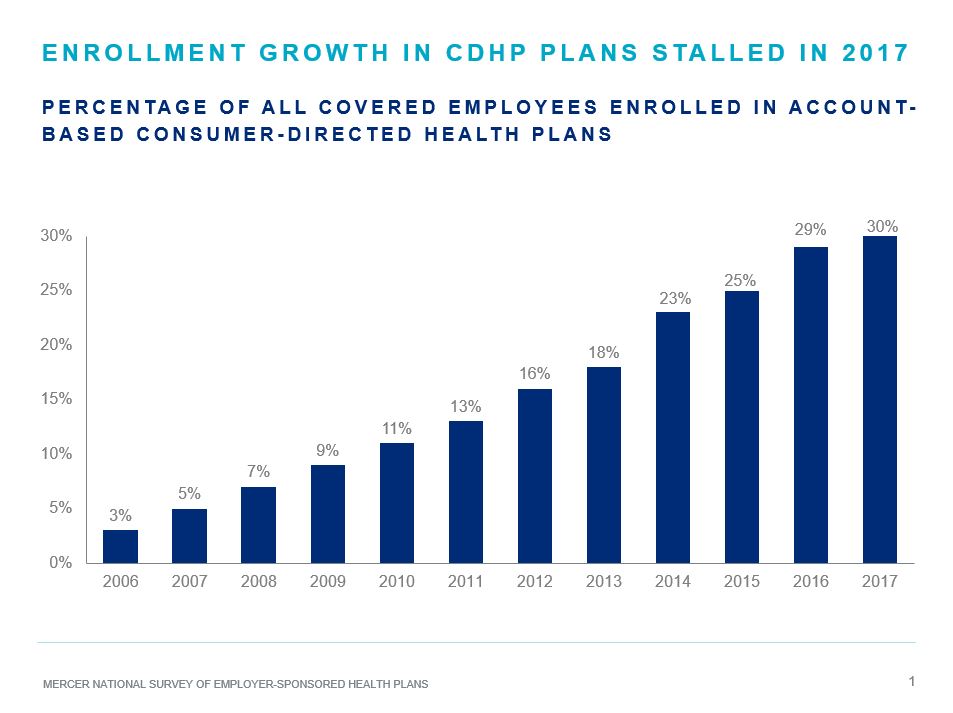

After a decade of cost growth of 6% or higher, beginning in 2012 employers have held cost growth to about 3% annually. A key strategy behind this success has been consumerism – giving employees more financial responsibility. Employers added high-deductible consumer-directed health plans and enrollment grew steadily – that is, until 2017, when enrollment slowed to nearly a standstill, rising just from 29% to 30% of all covered employees. While this might be just a temporary pause, it’s worth stopping to consider whether most of the early adopters have already enrolled and the next wave will be harder to persuade. This is important, because with the excise tax still on the books for 2020, high CDHP enrollment may be an important line of defense for many employers.

Of course, employers could simply drop all other medical plan options. But while that was a scenario many envisioned five years ago, full replacement hasn’t become a widespread practice. Most employers with 500 or more employees still offer CDHPs as a choice, rather than as a full replacement. Over the past five years, the percentage offering a CDHP as the sole medical plan has grown only from 6% to 10%, while the percentage offering a CDHP as a choice has grown from 28% to 54%.

Employers know that employees increasingly value choice. For employers that want to both provide choice and manage cost – which is most of you – the challenge is to steer employees to most cost-efficient level of coverage that makes sense for their financial situation and healthcare needs. Decision-support tools and other resources can empower them to choose the right plan and then get the most out of it:

- Voluntary benefits like hospital indemnity and critical illness coverage

- Telemedicine to help them save real money on out-of-pocket costs

- Health advocate services to help them navigate the system

- Expert medical opinion to help ensure they get the right diagnosis and find the best provider for the services they need.

Offering a range of medical plans, supplemental health plans, and point solutions helps personalize a health program, but there’s a catch -- you have to select and manage them all. That’s why a bundled solution can make sense for some employers, to ensure their employees have access to best-in-class programs that can add value to a high-deductible medical plan. In 2017, 16% of employers had already made the move to a bundled solution, with another 17% considering it. For 66% of employers, a bundled solution isn’t yet on the radar – but maybe it should be.

If you want to learn more about how employers are leveraging successful consumer empowerment strategies with their workforce and building CDHP enrollment, join me (and others!) for a webcast on January 17th.