When it Comes to HSA Plan Enrollment, Intention is Everything

We’ve reported that growth in consumer-directed health plan enrollment slowed in 2017, based on Mercer’s National Survey of Employer-Sponsored Health Plans. With many survey findings, if you dig around a little you can find interesting stories hiding behind the national averages, and in this case, we found that enrollment levels in HSA plans are related to how employers view the plan – a finding that could be useful to employers hoping to grow enrollment. Let me explain.

Most employers (86%) that sponsor an HSA plan offer it to employees as a choice, rather than as a full replacement (note that this analysis is based on employers with 500 or more employees). To assess how enrollment grows over time, we looked at employers that have offered an HSA-eligible plan as an option for at least three years and found that an average of 36% of covered employees enrolled in the HSA in 2017, up from 29% in 2015. Based on these national numbers, you’d say that while enrollment does grow over time, it doesn’t grow very quickly.

But not all employers offer HSA plans for the same reason. For the 14% of HSA sponsors offering the plan as a full replacement, high enrollment is obviously a goal. What about for the employers offering the plan as a choice? When asked about their primary objective for the HSA plan, 61% of these sponsors say they offer the plan as a low-cost option to provide medical plan choice, and another 4% say they added the plan simply to meet the ACA’s affordability requirement.

However, about a quarter of sponsors (27%) consider the HSA plan their “core” plan, with the goal of high enrollment. When the HSA is the core plan, the benefits are generally richer — the average actuarial value is 83%, compared with 80% among plans offered to provide a low-cost option. (Actuarial values were calculated using plan design information provided by survey respondents and Mercer’s proprietary plan value model, MedPrice.) Employers that offer the HSA as the core plan are more likely to provide an account contribution — 85% compared with 71% — and among those providing a contribution, the average amount is somewhat higher — $689 for employee-only coverage, compared to $612.

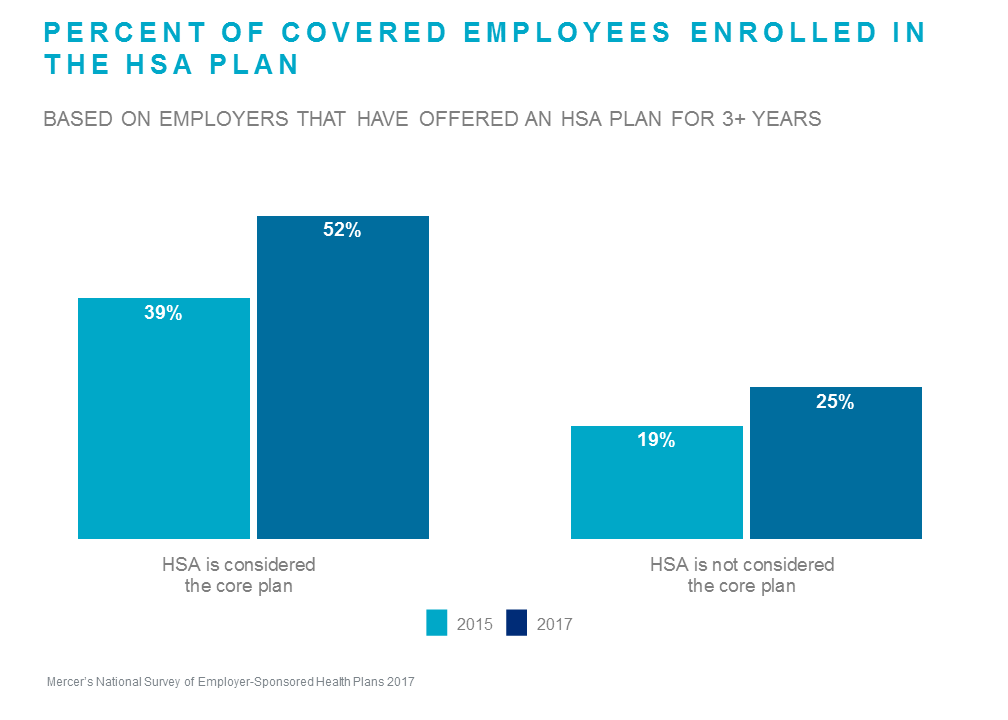

The pay-off? The employers that position the HSA as the core plan achieved more than double the average enrollment of other employers in 2017: 52% compared with 25%. Again, this is based on plans offered for three or more years, and from 2015 to 2017 enrollment also grew faster in the group of core plans, from 39% to 52%, while it grew only from 19% to 25% in the plans not considered core.

Interestingly, there is little difference in employee premium contribution requirements between the two groups. Past analyses have shown that investing in communications can make a bigger difference than a contribution differential in driving enrollment to an HSA plan – an important thought to keep in mind for employers ready to commit to the HSA plan as the core medical plan.