What If Employees Could Buy Coverage with Tax-Free HRA Contributions?

Dan Moore

Dan Moore

Suppose employers could fund health reimbursement accounts with tax-free dollars so that employees could buy coverage on their own in the individual market. That’s a possibility raised by the executive order on healthcare just signed by President Trump. But is this a change that employers would welcome?

Right now, under the 21 Century Cures Act, signed into law in 2016, employers with fewer than 50 employees can fund an HRA for this purpose, although with limits. But earlier this year, we asked employers of all sizes whether they would consider this option as a way to provide coverage for some or all of their employees. About 750 benefit professionals responded to the March survey.

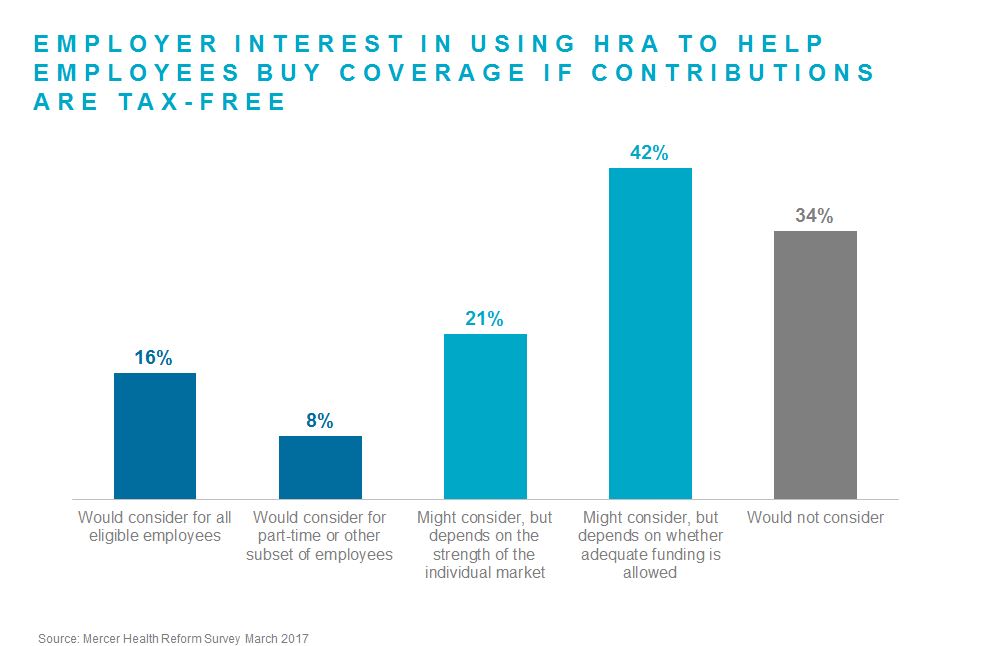

The results were interesting. Respondents were at least open to the idea. Only about a third of employers – of any size – said they would not consider this option. This was something of a surprise, given that we have surveyed employers since the ACA was signed into law and they have consistently rejected the idea of terminating their health plans and sending employees to the public exchanges to buy coverage on their own. Most employers, even those that might be attracted to the idea of getting out of the business of providing health care, realized that the math simply didn’t work – employees would be buying coverage with after-tax dollars, so employers would need to gross up their pay to keep them whole and pay the ACA penalty for not providing coverage. But if funding an HRA satisfied the ESR requirement and the money contributed were tax free, the math gets better.

Still, there are other issues to consider. Would they be allowed to contribute enough so that employees could obtain coverage of comparable value? And would the individual market offer coverage that employees would want at prices they could afford? The majority of respondents to the survey said they would need to know the answers to these question before they could consider using an HRA for this purpose.

These are important questions, but a number of respondents signaled their interest in this approach by saying they were ready to consider this option for all employees (16%) or at least for part-timers or another subset of employees (8%). Smaller employers were the most likely to say they would consider this option for all employee -- 23% of those with fewer than 500 employees, compared to 10% of those with 5,000 or more.

Even if HRA rules changed immediately – which is not likely – few employers with a January 1 plan year would be able to take advantage of this for 2018 since most have already finalized benefit offerings and are preparing to launch open enrollment. Employers will need to see how the regulations are written before they can assess whether tax-free HRAs could have a role in their benefits strategy. But a change like this could lead to new approaches to defined contribution benefits – and a way to attract gig workers.