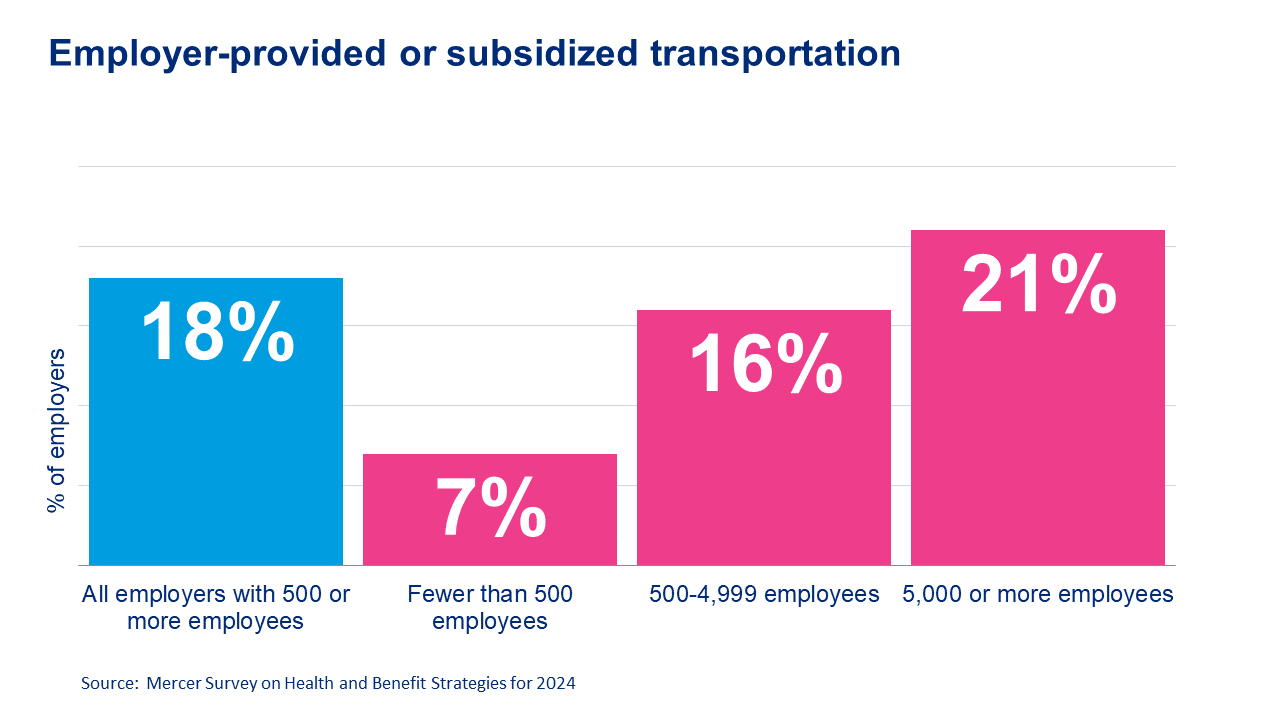

Transportation benefits – a return-to-office perk

Plan funding and design options

Qualified transportation benefits apply to transportation between an employee’s residence and place of employment. Benefits may be funded by the employer and/or by the employee on a pre-tax basis, subject to monthly dollar limits indexed annually. These programs are not subject to ERISA nor the cafeteria plan rules and allow employees to change benefit amounts during the year for any reason. Unused amounts can be rolled over to the next plan year but cannot be cashed out. They are forfeited when the employee terminates employment. Rules regarding substantiation, use of vouchers and taxation of excess amounts apply. Note, however, generally, through the end of the 2025 tax year, contributions are not tax-deductible for employers, except for bicycle-commuting expenses.

The following four types of transportation expenses may be provided:

- Transportation in a commuter highway vehicle, such as vanpools

- (Mass) transit passes

- Parking

- Bicycle commuting

A program can provide all or a combination of these benefits, allowing employers to tailor the program specifically to its workforce location and needs, in accordance with IRS requirements. Cash reimbursement of expenses incurred or paid for vanpools, qualified parking and sometimes transit passes, can be provided so long as the reimbursement is made under a “bona fide reimbursement arrangement.”

Monthly limits

The federal tax-free benefits are limited to a monthly amount, adjusted annually for the cost of living. For 2023, the combined commuter vehicle and transit limit is $300 monthly, while the parking benefit has a separate monthly limit of $300. We expect 2024 rates to be finalized soon but they are currently projected at $315.

Separately, bicycle commuting reimbursement is limited to $20 monthly. However, bicycle commuting expenses are not eligible to be provided on a pre-tax basis through December 31, 2025.

State / local laws

Employer next steps

Employers that have (or are contemplating adopting) a transportation benefits program should consider the following next steps:

- Confirm which, if any, state or local transportation mandates apply to your workforce locations

- Assess whether a transportation benefit would be valued by employees and design accordingly based on sustainability goals, office location, availability of mass transit, and other means of commuting to work

- Revise the plan design of an existing transportation benefit to account for changes in workforce, if necessary

- Evaluate transportation vendors for administration and compliance, including assistance with developing a bona fide cash reimbursement plan or administering a voucher program on a local or multi-state/jurisdiction basis

- Review payroll, enrollment and other administrative details to ensure employees do not exceed monthly limits

- Communicate the benefit availability and election process to employees

You can read more about transportation benefits, compliance requirements and state and local requirements in our GRIST: Transportation plans offer valued benefits but pose compliance issues.