The Golden Bachelor: A wake-up call for employers to invest in longevity literacy

Longevity literacy: The basics

Quality of life

A person’s quality of life is the first, and most important, aspect of longevity literacy. As employees age, many of them worry about the kind of life they will have in their later years. According to the Longevity Literacy Pulse Poll of about 400 employees of global corporations that fuels the report’s findings, 43% of respondents said illness or health was their top concern for maintaining a high quality of life in their later years – with many of them pointing to fears of cognitive and physical decline. Personal health wasn’t the only concern of many respondents either; two-thirds reported fearing they would need to look after older or unwell family members into the future, and 45% of respondents under 40 believe they will need to financially support their older relatives.

Race also appears to play a role in how people think about their older years. The report found 56% of white respondents believe they will live past 85 compared to only 38% of non-white respondents. Further, 52% of white respondents believe they have saved enough money for retirement, compared to just 26% of non-white respondents.

Here are a few ways employers can address quality-of-life challenges:

- Take care of employees who are caregivers with caregivers’ leave, flex-work arrangements, and information resources.

- Analyze your retirement plan design’s effects on retirement readiness and labor flow. This can help you provide a clearer path for your employees on their options for retirement.

- Design benefit plans that address barriers to quality of life for diverse populations. As an example, you could provide preventative health support packages such as epigenetics (the study of how your behaviors and environment can cause changes that affect the way your genes work) that are targeted to the well-being of diverse populations.

Purpose

A sense of purpose is a critical aspect of maintaining a long and healthy life. The survey found that 40% of respondents under 40 want to retire by 60. If someone retires at 60, given the average lifespan of 73 years there’s an abundance of time to fill with meaningful experiences.

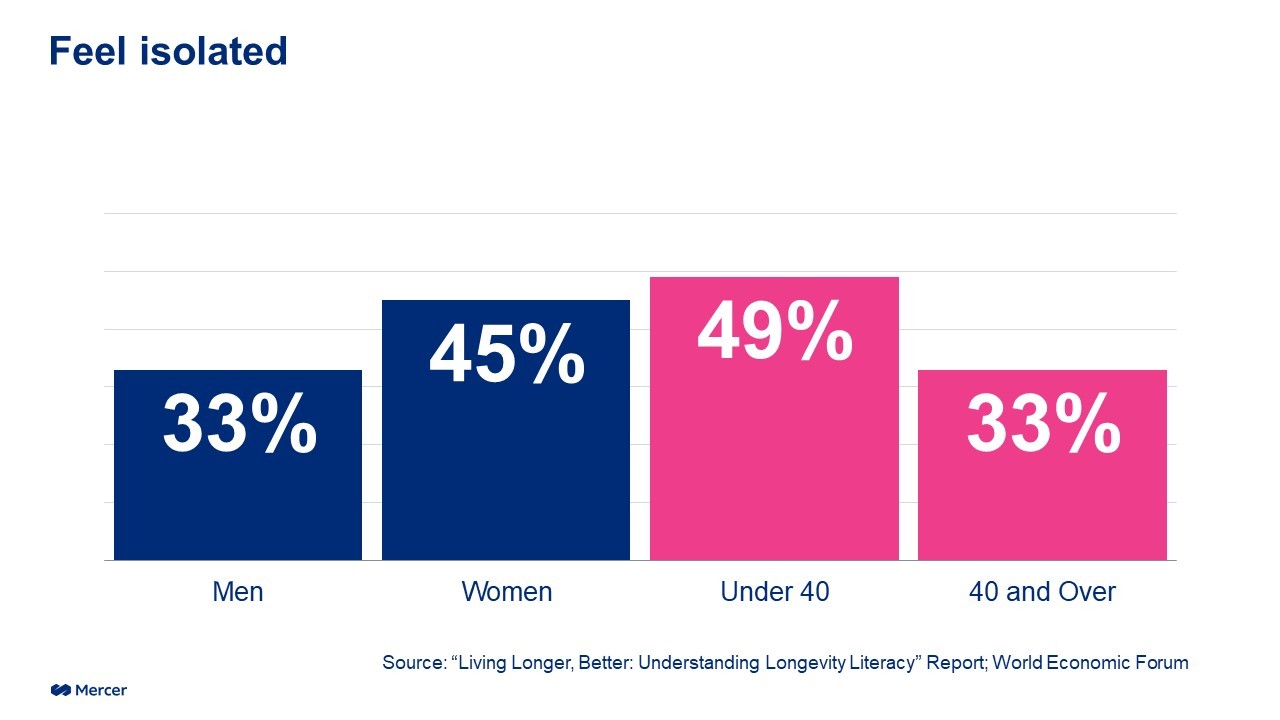

The primary factor to address in supporting a sense of purpose? Loneliness. The report indicates 40% of respondents feel isolated, with variations by gender and generation: Women were more likely to feel isolated than men (45% vs 33%), and younger people were more likely to feel isolated that older people (49% of those under age 40 vs 33% of those 40 and over).

Research has indicated that loneliness can have the same effects on the mental and physical well-being of older adults as smoking 14 cigarettes a day. This alarming statistic makes clear the importance of helping employees connect with others and live with purpose, whether by focusing on career or family, or by developing new hobbies and skills. Here are a few ways to help:

- Provide incentives for developing skills, such as by implementing a skills-based pay approach and being transparent about how investing in self-development now can pay back over time.

- Offer accessible volunteer opportunities that allow individuals to reap emotional rewards now and a network for later in their life.

- Create inclusive groups to combat loneliness; provide targeted, affordable training opportunities for diverse groups.

Financial resilience

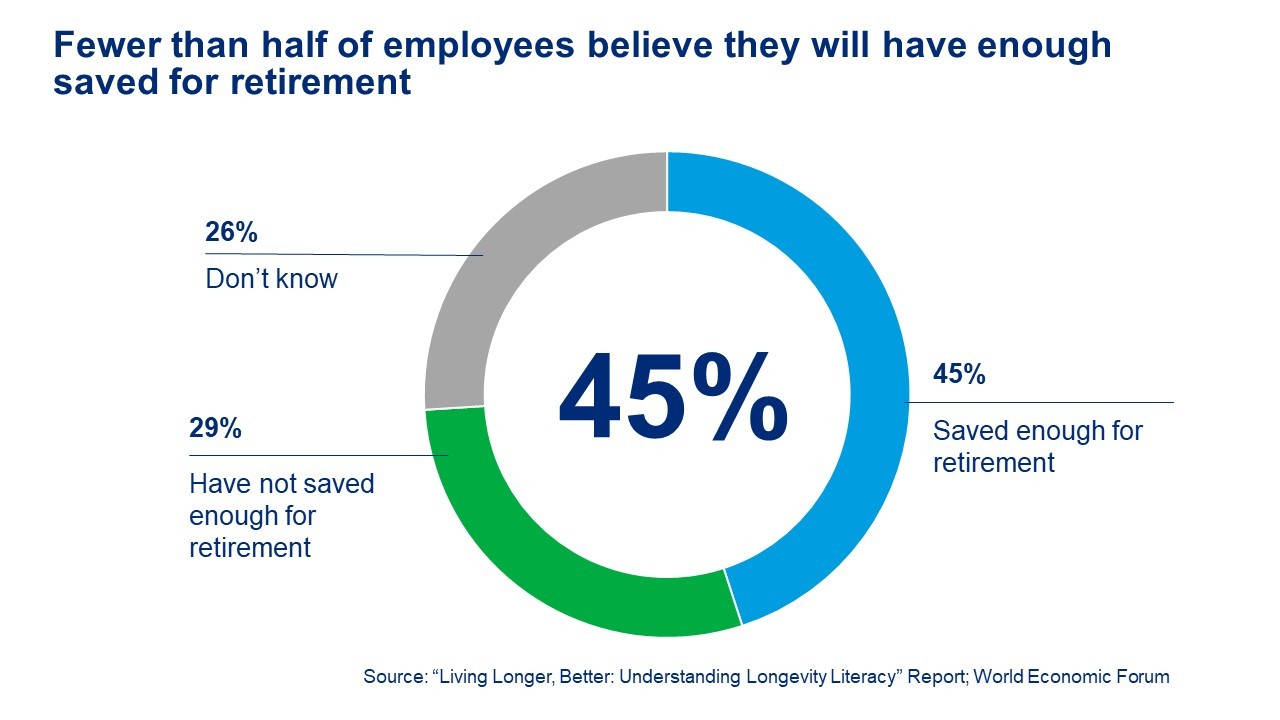

Once again, there are various hurdles minority groups are facing. Some 55% of respondents said they have not saved enough - or don’t know if they can save enough - for retirement. This number drastically increases among women, who are 41% more likely to have these concerns. Age also plays a key role when determining financial resilience, especially when it comes to seeking financial advice. Respondents under 40 years old were more likely to seek financial advice from various resources in general, and they were 8 times more likely to use social media for financial advice.

Worried employees may look to save more money, or simply keep working and retire later in life. To help alleviate workers’ financial concerns, employers may consider the following actions:

- Implement financial wellness programs focused on helping participants understand how to save for retirement, and that specifically address the financial concerns of low-income workers.

- Communicate your guidance and advice on financial well-being clearly. Ensure this information is accessible to all and consider a variety of channels that engage digital and non-digital users alike.

- Adjust your benefits and programs to target various needs across demographics, such as generation, gender and ethnicity.

We don’t know if bachelor Gerry Turner will find the love he’s looking for, just as many employees don’t know what their older years hold in store for them. However, with their employer’s support, employees might just get to contribute to the workplace for longer and retire with a future that’s a little more golden.

You can learn more about longevity literacy and our collaborative report here.