Survey results: There is more to virtual care than telemedicine

Health benefit cost growth is accelerating. Normally, that’s a signal to ratchet up cost management efforts. But in today’s tough labor market, many employers are looking for ways to make the benefit package more attractive and are prioritizing well-being to keep workers engaged and productive. Others may be concerned about health care affordability for their lower-wage workers.

Still, while shifting cost to employees may not be an option, neither is doing nothing. Results from our National Survey of Employer-Sponsored Health Plans show a growing number of employers are exploring virtual care solutions that can enhance access, convenience and cost-efficiency.

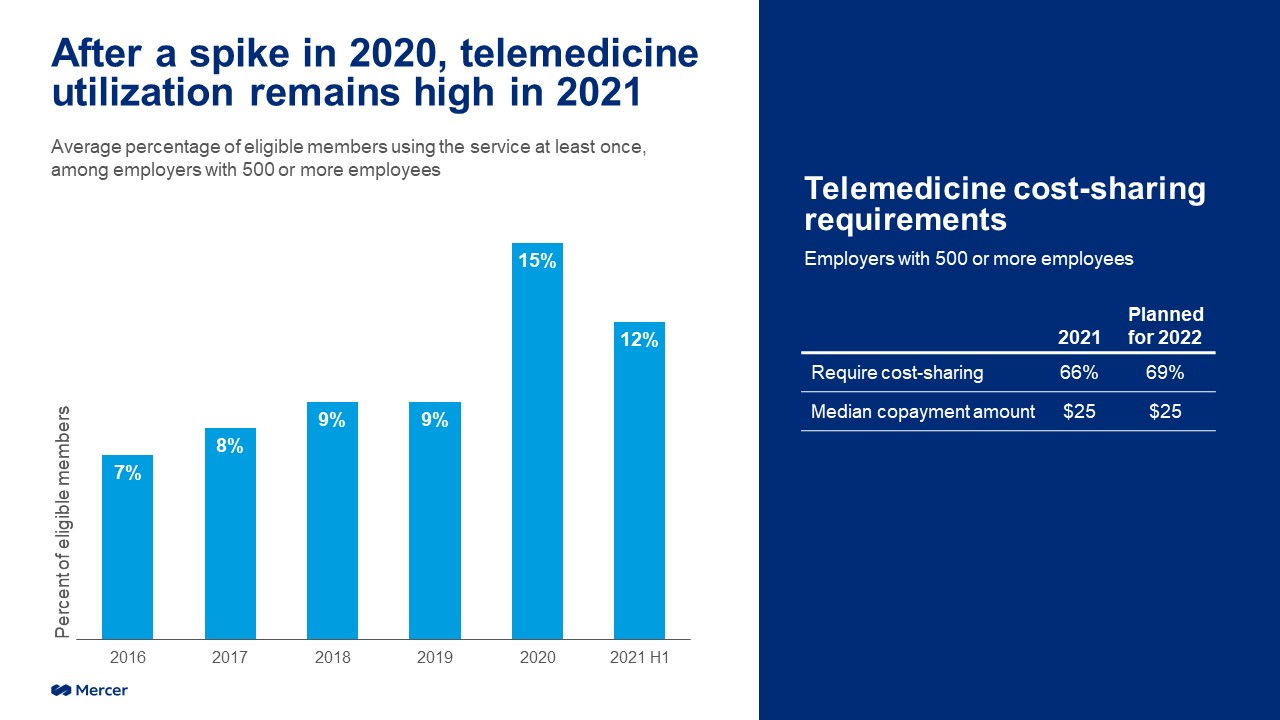

Virtual health care can optimize value by making it easy for members to access the most appropriate level of care. In the most obvious example, that could mean choosing a telemedicine visit instead of a trip to the ER in the middle of the night. With in-person health care severely limited during the worst of the pandemic, both providers and patients turned to telemedicine. Prior to the pandemic, utilization rates for traditional telemedicine (services such as Teladoc and Doctors on Demand) had stalled at 9 percent or less among large employers for several years. In 2020, utilization jumped to 15 percent and in the first half of 2021 it remained a relatively high 12 percent, even though the majority of large employers (66 percent) had reinstated cost-sharing with a median copay of $25. In 2022, 69 percent of employers will require cost-sharing.

Now offered almost universally, traditional telemedicine services have been a critical source of care during the pandemic, but there are many other forms of virtual care as well. Over a fourth of large employers (28 percent) offer a virtual behavioral health care network. A virtual Primary Care Physician (PCP) network or service is offered by 16 percent of large employers, with another 10 considering it. This type of service typically provides patients with virtual-only access to a team of primary care providers, steering them to in-person care outside the network as needed. Virtual care also encompasses a wide range of digital health solutions that don’t rely solely on real-time interactions with a live health care professional. Targeted health solutions that address specific health conditions such as diabetes or musculoskeletal are now offered by 25 percent of all large employers, with another 20 percent considering adding them. AI-powered triage programs, which suggest care options based on reported symptoms, are just starting to gain traction; they are offered by only 2 percent of employers, but an additional 5 percent are considering them.

Growing acceptance of virtual care prompts employers to pursue a range of digital strategies

Employers with 500 or more employees

| Currently offer | Considering | |

| Traditional telemedicine (e.g., Teladoc, MDLIVE, Doctor on Demand) |

94% | 2% |

| Virtual behavioral health care (e.g., Lyra Health, Ginger) |

28% | 21% |

| Targeted virtual health solutions (e.g., Livongo, Hinge Health) |

25% | 20% |

| Virtual PCP service or network (e.g., 98point6, Medici) | 16% | 10% |

| AI triage program to identify care options (e.g., Babylon, Buoy) |

2% | 5% |

And on the horizon is a novel approach called Virtual First Care, or V1C, that relies on providers who function mostly, if not entirely, outside of brick and mortar facilities. V1C gives individuals the ability to initiate care from anywhere, at any time, through telecommunication and digital technologies. It includes a personalized platform that offers a range of solutions to support a person along all the necessary steps in their health journey.

When the survey asked employers about their objectives for adding virtual care in their programs, they placed “greater convenience” at the top of the list – above “improving access” and “managing cost.” In any strategy that seeks to steer employees to higher-value care, convenience must be part of the equation, along with affinity. People want to get their care through the channels they are most comfortable with, and that’s not always a doctor’s office. It might be a pharmacy or a retail establishment — and more and more these days, it’s online.