High-Cost Claims Are Raising Employer Risk

Mercer

Mercer

In a recent Mercer survey of about 300 health benefit professionals, when asked to identify their biggest health plan cost-drivers, 74% of respondents cited high-cost claims. Two factors have combined over the past few years to heighten employer risk for high-cost claims: the rise of costly new medical technology and treatments – including specialty drugs -- and the ACA requirement to remove limits on annual and lifetime benefits payable.

As a result, the market for employer stop loss insurance has become increasingly complicated and costly. Statistics from a 2017 Sun Life Financial Stop Loss Report show that the frequency of claims above $1 million increased 68% between 2013 and 2016. Additionally, a recent ESI Drug Trend Report indicated that specialty drugs now represent a third of all drug expenditures. Patients being treated with recently developed drugs such as Venclexta, for leukemia, or Zinbryta, for multiple sclerosis, have annual costs well in excess of $100,000. And specialty drug costs are expected to trend upward at a rate of 20% to 30% through 2019.

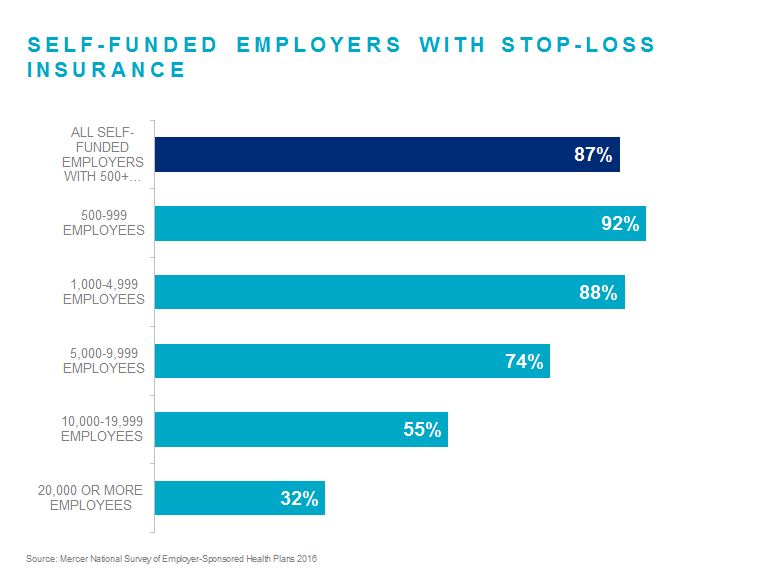

Traditionally, the majority of self-funded employers have purchased stop loss insurance to protect themselves from unexpected catastrophic claims. In 2016, 87% of all large self-funded employers (those with 500 or more employees) purchased stop loss coverage – although among the very largest (20,000 or more employees), this drops to 32%. As the frequency and severity of catastrophic claims have increased exponentially, employers that don’t purchase stop loss should review their previous strategies to ensure they are still appropriate.

For employers that already have stop loss, reviewing their policy for the most comprehensive terms and conditions is a must. Stop loss policies are typically 12 months in length and allow stop loss carriers to increase rates and/or apply lasers – higher deductibles for ongoing large claimants – at renewal. Policies without rate caps or provisions restricting carriers from adding lasers at renewal can leave an employer’s ongoing risk virtually unlimited.

Taking a closer look at your stop loss coverage -- or lack thereof -- has never been more important.

For many employers, increasing the stop loss deductible every two or three years can help offset the impact of rising claim trends, but as the healthcare landscape continues to evolve – expensively - it may take more than business-as-usual to minimize the growing risk. That is one reason Mercer’s Stop Loss Center of Excellence established a stop loss coalition with a small group of best-in-class stop loss carriers. Today the coalition includes over 400 clients, 1 million covered employees, and $400 million in premiums. Its unique benefits include the opportunity to participate in premium refund arrangements (these have returned approximately $19 million in premium to clients since the coalition’s inception in 2009); enhanced policy agreements; pricing discounts; and competitive performance guarantees.

For more information, contact your Mercer consultant or daniel.davey@mercer.com.