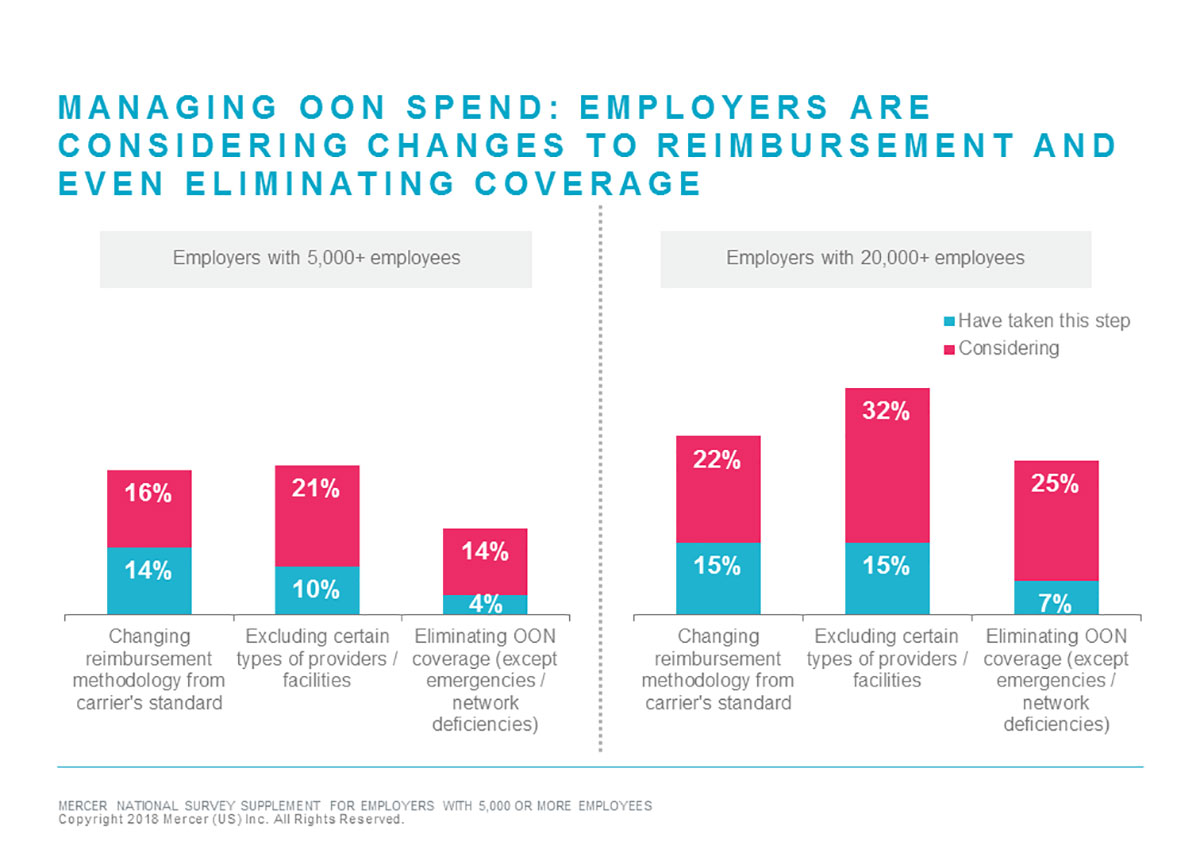

Are Out-of-Network Benefits Soon to Become Obsolete?

Minimizing out-of-network utilization has been a perennial item on many plan sponsors’ to-do lists, but we’re now starting to see some employers eliminating out-of-network (OON) benefits altogether. According to Mercer survey data, while fewer than 10% of jumbo employers (those with 20,000 or more employees) have actually taken this step, another 25% are considering it. We know from past experience that new strategies seen among jumbo employers sometimes emerge as trends in the broader employer community. Will this be the case with eliminating OON benefits? Here are some thoughts on why it may be an effective strategy for some, but not all.

The trouble with out-of-network claims

On average, less than 10% of medical plan claims are incurred with OON providers. But as employers have become more focused on steering employees to high-quality, cost-effective providers, they’ve also become more concerned about the care that members receive from OON providers. Particularly worrisome is OON utilization of expensive, poor-quality facilities for treating substance use disorder. These facilities may waive or minimize out-of-pocket costs for patients but send hefty bills to the health plan, which, under mental health parity laws, must provide members with same OON benefits for mental health as for medical care.

The problem with OON providers is the lack of quality oversight. Without a contractual relationship via network participation, there’s no avenue to initiate improvement. While some very good providers have decided to be out of network to simplify their lives and because they can get enough business on that basis, not all non-network providers are good. But when providers operate outside a health plan network, the plan doesn’t monitor their performance and employers don’t have access to performance data.

Another reason employers are moved to eliminate OON benefits is dissatisfaction with shared savings fees, where the carrier negotiates the OON charges and keeps a significant portion of the savings for their work. Some employers have discovered waste in shared savings charges for non-network provider negotiations and simply concluded that continued spend on non-network benefits was poor plan stewardship.

When maintaining out-of-network benefits is the right thing

There are a number of reasons why members go out of network. If non-network usage is related to poor access to certain services in-network – for example, behavioral healthcare, employers should think carefully about removing the benefit without first addressing the access issue. It’s also important to look at the volume of existing OON utilization for emergency care, elective procedures and essential care to estimate the impact of eliminating OON coverage. If major sources of non-network spend are for essential services, such as ambulance rides (including the air lift variety that can cost $20,000 per trip) and emergency room care, the opportunity to reduce cost may be limited.

There are other, more moderate, strategies to address OON utilization, such as excluding specific providers/facilities and changing OON reimbursement methodology. But if careful analysis suggests that eliminating OON coverage is viable for your organization, thoughtful messaging is essential to effectively support this type of change. Employees need to understand that the goal is higher-quality care and better-managed cost – for the plan and for patients.

Mary Kay O’Neill, Albert Snell, Mendy Stein, Peter Hou and Jeff Dobro contributed to this post