HSAs: Saving for, and During, an Emergency

Before the COVID-19 pandemic, HSAs were gaining a lot of traction as a valuable tool in the retirement tool belt. While we certainly don’t intend to minimize the importance of saving for long-term retirement goals, this pandemic reminds us that saving for unexpected emergencies is an equally important goal. Moreover, for most people, these goals are not mutually exclusive. And, as we’ll discuss, HSAs can serve both needs effectively.

With unprecedented numbers of Americans filing for unemployment compensation and paying for COBRA coverage, it is important to remember that tax-free HSAs distributions can reimburse any health coverage premiums while an individual is receiving federal or state unemployment compensation, as well as COBRA premiums, even if an individual is not receiving unemployment benefits. (An example of this would be an employee who experiences a reduction in work hours that makes him or her ineligible for the employer health plan.)

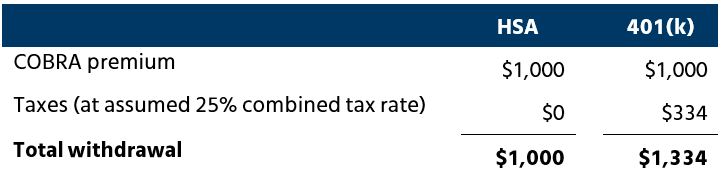

In light of a reduced income, or no paycheck, individuals may look at their various savings accounts to pay for premiums. Let’s compare the net costs of withdrawing funds from a 401(k) versus an HSA by an individual paying a COBRA premium of $1,000 per month:

As this simple example illustrates, the negative impact on savings is reduced significantly by using tax-free HSA funds, as opposed to funds from a non-tax sheltered account like a 401(k) or traditional IRA, to pay for COBRA premiums.

In addition, if eligible to make further HSA contributions for 2019 or 2020, this individual could contribute any premium amounts needed first into the HSA, and then withdraw that amount to pay COBRA premiums tax free. With the deadline for making 2019 contributions extended to July 15, 2020, this would be an excellent way to maximize savings on an immediate expense and minimize the impact on future savings. In essence, the HSA acts as a tax-effective pass-through account. To receive the tax advantage for the contribution, individuals would claim the deduction on their 2019 or 2020 tax return. Not only will this strategy provide a tax benefit on premiums paid, it will also preserve existing HSA funds for retirement needs. (Note that pending COVID-19 legislation includes a government-provided COBRA subsidy, and if enacted, might mitigate the savings from this strategy.)

As many employers are building their benefits strategy for 2021, boosting financial wellbeing is an important component. While it’s impossible to know what the future holds, it is important to remember the role HSAs can play in preparing for emergencies as well as boosting a population’s savings habits in general.