Pension Risk Transfer versus Cash Flow Matching

Is cash flow matching a viable and less expensive alternative to pension risk transfer?

Cash flow matching was an early form of liability-driven investing for US defined benefit plans. In fashion during the 1970s and 1980s, it gave way to asset liability management strategies focusing on matching the interest-rate sensitivity of liabilities and market value of assets rather than matching future expected fixed-income coupon payments and bond maturities to expected future participant benefit payments. Cash flow matching has recently resurfaced as a potentially viable and less expensive alternative to pension risk transfer strategies such as retiree buyouts. It has also gained traction as a strategy for underfunded plans, where benefit payments exceed employer contributions. There is a vast literature describing cash flow matching portfolio construction and extolling the clear benefits to these plans of adopting the strategy. A cash flow matching strategy allows for a greater allocation to less liquid, higher-expected-return asset classes in order to help improve funding levels. The focus of this paper is on whether cash flow matching is a viable and less expensive alternative to pension risk transfer. Viable, feasible, possible – sure. Whether it is less expensive is not so clear, and plan sponsors need to consider numerous factors to decide whether to utilize cash flow matching rather than pension risk transfer.

Pension risk transfer – the perfect hedge

Increasingly, US corporate defined benefit pension plans have turned to life insurers to take on the liability associated with all, or a subset of, their plan participants through an annuity purchase. In this type of pension risk transfer, a premium is paid to a life insurer who then assumes the responsibility, risk, and cost of making benefit payments to participants. Here, we will focus on comparing retiree-only pension risk transfers (“retiree buyouts”) to a cash flow matching strategy and, as we’ll see, cash flow matching is generally best suited to retiree-only liability blocks, in our view. Furthermore, retiree buyouts are the largest component of pension risk transfers.

PRT Deal Volume 2014-2024

We expect employers to continue to shed risk through pension risk transfers and, in particular, retiree buyouts, for myriad reasons. First and foremost, these pension risk transfers are the perfect hedge. All investment and longevity risks are transferred to the insurer, while administrative and investment expenses and PBGC premiums are eliminated for the sponsor. No other investment strategy can make this claim. Secondly, the pricing for retiree-only deals has improved dramatically. Whereas a decade ago, insurers might have charged a premium of up to 5% or more over the market-based liability being held by the plan sponsor, in 2023, many of these deals transacted with no premium or at a discount (driven in part by the fact that many deals were for smaller monthly benefits, which often receive more favorable pricing compared to deals with larger monthly benefits). Part of this pricing improvement can be attributed to increased competition. Twenty-one insurers are currently active in the retiree buyout market, compared to fewer than ten insurers a decade ago. Insurers have extensive actuarial and risk-management expertise in managing liabilities, in addition to strong administrative capabilities. Granted, retiree liabilities are a natural hedge to life insurance blocks; as such, this has become an attractive business for life insurers.

Headwinds to a retiree buyout include the one-time income statement settlement recognition that occurs if the buyout is large enough (liability released is greater than the service cost plus interest cost in accounting terminology). While this settlement charge is “below the line,” careful management and understanding of any potential charge is important. A pension risk transfer may result in a deterioration of the funded status, which might trigger an employer cash contribution to restore the funding level to certain regulatory levels. While we see this headwind less often, it also needs to be considered. Finally, some plan sponsors view the transfer of assets to an insurer as detrimental, as they could keep the assets and potentially earn a higher return than the AA yield. Careful design of the retiree buyout can help mitigate these headwinds and alleviate concerns.

Cash flow matching – an old foe

Cash flow matching has been around since WWII when it was suggested by Tjalling C. Koopmans, a Dutch mathematical economist working at Penn Mutual Life Insurance Co (he won the Nobel Memorial Prize in Economic Sciences in 1975). The basic idea is to construct a fixed-income portfolio whose cash inflows (coupon and principal payments) match pension plan outflows (benefit payments to retirees). This is often referred to as “dedication,” as each set of inflows is dedicated to a specific outflow. Optimization techniques are designed to identify the least-cost portfolio and address reinvestment risk, while meeting any additional constraints that may be set on the portfolio by the plan sponsor. Generally, a buy-and-maintain approach is adopted to limit turnover and address credit risk. Cash flow matching is usually limited to a closed group of current retirees, as benefit payments to other participants cannot be predicted with a similar level of accuracy.

Cash Flow Matching

Least-cost Fixed-income Portfolio

With Non-negative Cumulative Net Cash Flows

Cash flow matching fell out of favor as a liability-driven investment strategy in the late 1980s, partly due to the fact that it is a strategy intended to meet future values rather than present values (e.g., mitigate volatility in the funded status). With changes to accounting standards in 1986 that necessitated the use of discount rates based on high-quality corporate bond yields (generally AA or better) that could settle liabilities, the focus turned from cash flow matching to duration matching. The Pension Protection Act of 2006, requiring the use of high-quality A-AAA bond yields to determine IRS cash contribution requirements, further heightened this focus on matching the interest-rate sensitivity of assets and liabilities.

Many defined benefit plans have annual benefit payments that exceed cash contributions (negative net cash flow). Underfunded plans with negative net cash flows will see their funded status decline on a percentage basis. A greater investment return is therefore required to improve or just maintain the same funding level.

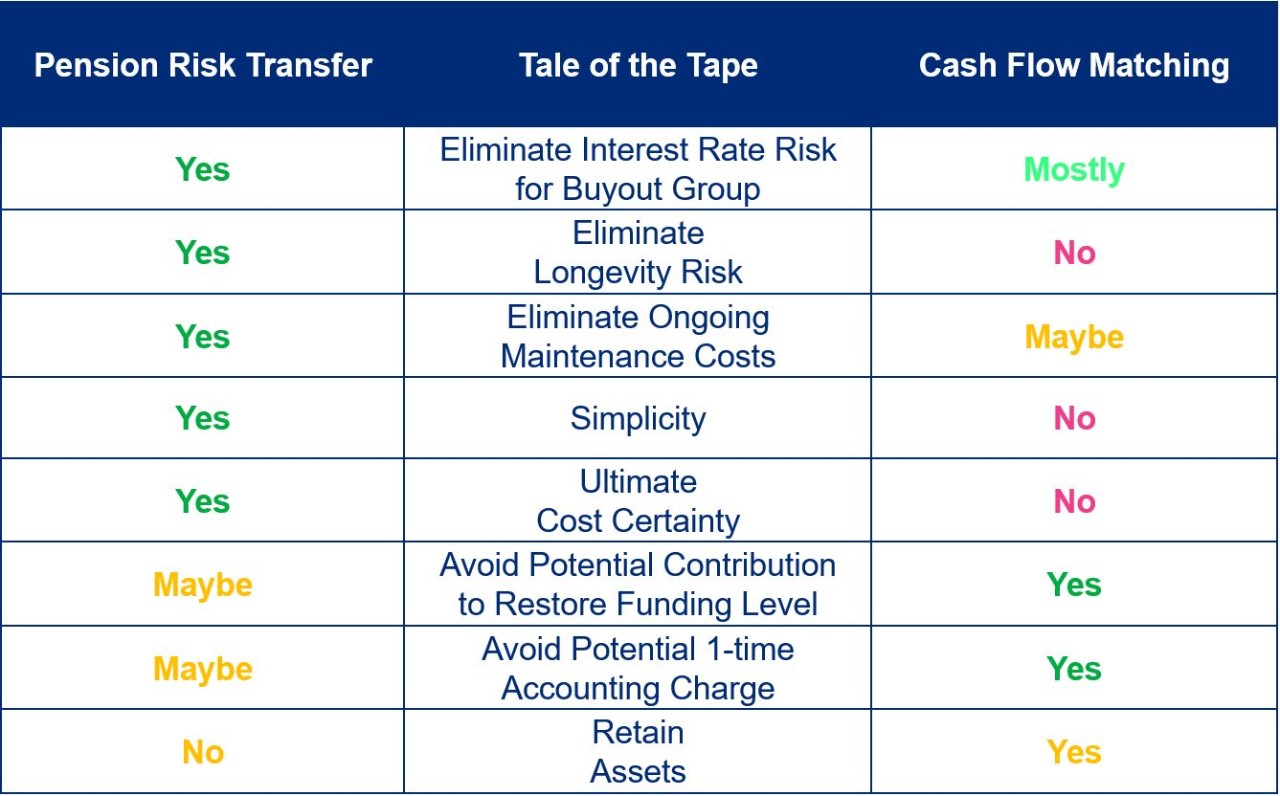

Tale of the tape

As described above, it is not uncommon for a retiree-only risk transfer (retiree buyout) to transact at or below par on a market-based liability basis. That is, for $100M of liabilities determined using an AA discount rate, an insurer would be willing to assume responsibility for making payments to these retirees for $100M in assets or less. In addition to no longer being exposed to investment and longevity risk, the plan sponsor has also eliminated all future costs associated with those participants, including administrative costs, PBGC premiums and investment management fees.

If, however, a cash flow matching portfolio consisting of AA, A, and BBB fixed-income securities is created instead, this lower-than-AA quality credit portfolio is expected to earn a yield higher than an AA yield used in determining the present value of the liabilities. Because yields and prices move in opposite directions, for less than $100M, we can defease the same liability (expected benefit payments) of $100M. This is the heart of the argument for cash flow matching as an alternative to pension risk transfer: a higher-yielding portfolio requires fewer assets to defease the same liability. Furthermore, with interest rates at multi-year highs (as of May 2024), more benefit payments can be defeased than when rates were lower. N.B. defeasance is not the same as elimination.

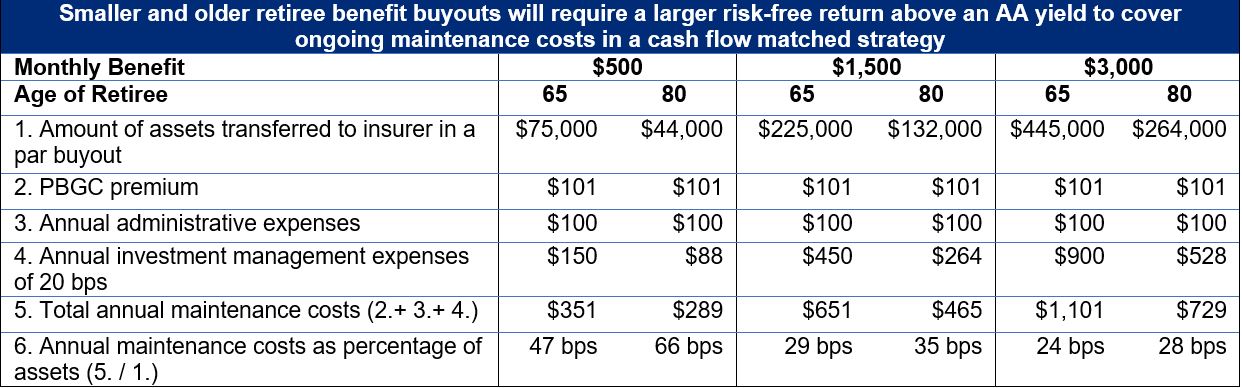

Maintenance costs such as administrative fees, PBGC premiums and investment fees remain under cash flow matching. Under pension risk transfer, however, they have been permanently eliminated for the retiree buyout group. In our example here, if $97M was used to create a cash flow matching portfolio, the $3M in savings relative to pension risk transfer could be used to help offset these costs.

Maintenance costs are plan-specific, depending on the total number of plan participants, level of administrative services provided and investment management fees. Furthermore, the average monthly benefit size and average age of participants in the buyout group have considerable influence on annual maintenance costs as a percentage of assets. As an illustration, if the average age in the buyout group is 65, a cash flow matched portfolio would need to earn roughly 25-50 basis points above an AA yield on a risk-free basis to offset ongoing maintenance costs. However, if the average age was 80, these excess returns jump to 30-70 basis points, requiring investment in lower-quality bonds to earn that spread.

Careful and detailed analysis is clearly warranted to see whether a cash flow matching portfolio can be constructed that will generate sufficient returns to offset future maintenance costs. Looking at the incremental yield required gives us a high-level view. Based on credit spreads in mid-May 2024, the credit quality of the cash flow matching portfolio might need to be dropped to as low as BBB, the lowest investment grade to meet maintenance costs. Plan fiduciaries will need to be comfortable with this drop in the context of the total portfolio.

The bell

Pension risk transfer and cash flow matching are different tools in the pension risk management toolbox. Pension risk transfer completely removes risks, while cash flow matching leaves risks with the plan sponsor. Is cash flow matching a viable and less expensive alternative to pension risk transfer? As we’ve seen, that depends. Viable, feasible, possible – yes. Less expensive? That’s not so clear. As the tale of the tape illustrates, there are numerous factors that plan sponsors will need to consider before deciding to utilize cash flow matching in lieu of pension risk transfer.