Partial plan termination relief not a free pass for reportable events

Pandemic relief in the 2021 Consolidated Appropriations Act (Pub. L. No. 116-260) may help defined benefit (DB) plan sponsors with large workforce reductions avoid the cost of a partial plan termination if employees are restored before April 1. But the relief won’t excuse sponsors from the Pension Benefit Guaranty Corporation (PBGC) reporting requirements for an active-participant reduction. Plan sponsors should continue to monitor their active-participant population in case PBGC event reporting is required.

Partial plan termination vs. active-participant reduction

Large reductions in an employer’s active workforce can trigger two different sets of requirements for DB plan sponsors: special vesting rules for partial plan terminations under Section 411(d)(3) of the Internal Revenue Code and event reporting to the PBGC under ERISA Section 4043 (29 USC § 1343). Although both requirements generally arise when a plan experiences a 20% or greater reduction in active participants, the determinations are not identical.

Partial plan termination. The IRS presumes a partial plan termination has occurred when employer-initiated terminations (that is, involuntary terminations) during a plan year exceed 20% of the number of active participants during that year. The employer can rebut the presumption based on facts and circumstances, such as demonstrating that the turnover rate is routine. If a partial termination occurs, the sponsor must fully vest affected participants to the extent their benefits are funded.

20%-plus active-participant reduction is reportable event. Unless a waiver applies, DB sponsors must file with the PBGC when an event or attrition causes an active-participant drop exceeding 20% of the number of participants at the beginning of the year. Single-cause events are measured and reported at the time of the event. Attrition events are measured at plan year-end and can be reported as late as the due date for the PBGC premium filing (generally 9-1/2 months after plan year-end, or Oct. 15 for calendar-year plans). Unlike partial plan terminations, active-participant reductions don’t distinguish between voluntary and involuntary terminations and have no rebuttal process.

Partial plan termination relief

Under the relief in the 2021 appropriations package, plans won’t have a partial plan termination for any plan year that includes the period beginning March 13, 2020, and ending March 31, 2021, if the number of active participants at the end of that period is at least 80% of the number of participants at the beginning of the period.

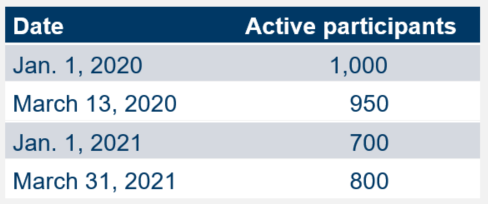

Example. A calendar-year plan had the following active-participant counts:

Assuming that all terminations were employer-initiated, the 30% reduction in the active-participant count during 2020 ordinarily would have triggered the presumption that a partial plan termination had occurred ([1,000 – 700] / 1,000 = 30%). However, because the active-participant count on March 31, 2021, is more than 80% of the active-participant count on March 13, 2020 (800 / 950 = 84.2%), no partial plan termination occurred during the 2020 plan year. For the same reason, no partial plan termination apparently will occur during the 2021 plan year, even if the participant count drops below 560 (80% of 700) by year-end.

Further guidance needed. The statute appears to say plans that qualify for the relief won’t have a partial termination for two consecutive plan years, regardless of their participant counts at the beginning and end of the plan years or any other events that would ordinarily give rise to a presumed partial termination. However, it’s not clear that this is what Congress intended. Further, the law provides no direction for employers that had already vested employees due to a partial plan termination before Congress granted the relief. Future IRS interpretive guidance may address these issues. In the meantime, employers in these situations should consult with legal counsel.

PBGC reporting still required

The plan sponsor in the earlier example is not entirely off the hook. The 30% reduction in active participants during 2020 must be reported to the PBGC using the Form 10, unless the plan sponsor qualifies for one of the four available waivers (low-default risk, well-funded plan, SEC disclosure or small plan). The timing for the required filing will depend on the circumstances of the termination — that is, whether the terminations occurred due to one or more discrete events, attrition during the year, or a combination.

Related resources

- Pub. L. No. 116-260, the Consolidated Appropriations Act, 2021 (Congress, Dec. 27, 2020)

- Reportable events & large unpaid contributions (PBGC)

- Retirement plan FAQs regarding partial plan termination (IRS)