DOL releases model COBRA subsidy notices and forms

Subsidy overview

The subsidy — which pays 100% of COBRA premiums, including the 2% administration fee — is available from April 1 to Sept. 30 to assistance eligible individuals (AEIs). An AEI is a COBRA qualified beneficiary who lost or will lose group health plan coverage (other than health flexible spending arrangement (FSA)) due to reduced work hours or involuntary employment termination and whose maximum COBRA coverage period overlaps the subsidy period. The subsidy is applicable to employees’ and family members’ premiums, but is not available to anyone eligible for other group health plan coverage or Medicare. The law also gives AEIs a second chance to elect COBRA if they didn’t have continuation coverage on April 1, 2021. However, those AEIs do not have to elect COBRA retroactive to the date on which they were initially eligible for COBRA.

Notice requirements

The ARPA creates a number of new notice requirements for employers. Employers must provide:

- Election notices with information about the availability of the premium subsidy to all COBRA qualified beneficiaries who have a qualifying event during the subsidy period

- In lieu of this notice, small employers (fewer than 20 employees) (and certain church plans covered by state law) with insured plans subject to state continuation requirements may provide qualified beneficiaries an alternative notice that includes subsidy information and an election form.

- Information about the premium subsidy and notice of a second chance to elect COBRA to all AEIs with qualifying events between Oct. 1, 2019, and April 1, 2021 (those enrolled in COBRA and those who did not elect or elected and later dropped)

- Employers do not need to provide information about the second chance to elect COBRA to anyone who is not an AEI and received a valid COBRA election notice prior to April 1, 2021.

- Advance notice to AEIs about the subsidy’s expiration, whether due to the end of the subsidy period or because the AEI’s maximum COBRA continuation period ends, if earlier

Employers can use the DOL’s model notices (available in both Word and PDF formats), revise existing notices to include the required subsidy information or create a separate subsidy explanation to supplement the existing COBRA election notice. Whichever approach is chosen, the law requires employers to distribute the following information:

- A description of the qualified beneficiary’s right to the COBRA subsidy and any conditions on entitlement

- A description of the option to enroll in different coverage, if the employer chooses to allow

- The forms necessary to establish subsidy eligibility

- Contact information for plan administrator and any other person relevant to the subsidy program

- A description of the second election period

- A description of qualified beneficiaries’ obligation to notify the plan to if they become eligible for other group health plan or Medicare coverage and the penalty for failure to do so

Model general COBRA notice and election notice

The model ARP general notice and COBRA continuation coverage election notice is a lengthy 14-page document (the first two pages are instructions). This model is for all qualified beneficiaries with a qualifying event between April 1 and Sept. 30 — even those ineligible for the subsidy because an event other than involuntary job loss or reduced hours triggered the COBRA right.

The model notice includes general COBRA information and details about the subsidy program. The notice also includes information about pubic exchange plans, ARPA’s increased premium tax credits, and the effect of COBRA coverage — and subsidy eligibility — on premium tax credit eligibility. The notice also contains a helpful list of factors for qualified beneficiaries to consider when deciding whether to enroll in COBRA, including:

- Premiums

- Provider networks

- Drug formularies

- Severance payments

- Service area

- Other cost sharing

The election form included with the model notice informs qualified beneficiaries that they have 60 days from the date of the notice to elect COBRA coverage. The election form makes a subtle reference to the outbreak period relief by suggesting some qualified beneficiaries may have additional time to elect due to a national emergency. However, if qualified beneficiaries want to receive the COBRA subsidy, they must elect within 60 days.

Another model form included is for employers allowing AEIs to change COBRA coverage to a different benefit option that costs the same or less than what they had on the last day of coverage. AEIs exercising this option must complete the change form within 90 days from the date of the notice, as well as timely complete the election form.

The model notice expires on Oct. 31. Employers should expect to use the normal COBRA model notices for all qualifying events occurring after the COBRA subsidy program expires on Sept 30.

Model alternative notice of ARPA continuation coverage election notice and form

A model alternative notice is available for small employers with fewer than 20 employees (and certain church plans that are covered by state law) that have insured plans subject to state continuation requirements. The notice contains information about the subsidy program and other coverage options. The model also includes a coverage election form and, if offered by the employer, a form for switching benefit options.

Model COBRA notice about extended election periods

Employers may use the model COBRA continuation coverage notice in connection with extended election periods for qualified beneficiaries currently enrolled in COBRA coverage due to reduced work hours or involuntary termination (AEIs), as well as those who would be AEIs if they had elected and maintained COBRA coverage. The notice describes the new COBRA rights and premium assistance created by ARPA. The model includes a COBRA election form for those not already enrolled and, if allowed by the employer, a form for AEIs electing to switch benefit options. Individuals have 60 days from the date of the notice to complete the COBRA election form (if not already enrolled) and 90 days to complete the change-in-benefits form (if offered).

Summary of COBRA premium assistance, request form and participant notification form

The Summary of the COBRA Premium Assistance Provisions under the American Rescue Plan Act of 2021 must be distributed with all of the above model notices. The one-page summary includes eligibility criteria, the 60-day election deadline, and the requirement for subsidy recipients to inform the group health plan of eligibility for other group health plan coverage or Medicare (and the penalty for failure to inform).

A two-page Request for treatment as an assistance eligible individual form is available for qualified beneficiaries to attest that they are eligible for the subsidy when electing COBRA. Qualified beneficiaries already enrolled in COBRA coverage can send this form separately to request the subsidy. However, employers presumably should provide the subsidy to AEIs already subject to COBRA, even if they don’t return this form. The employer or the plan completes the bottom of the form, approving or denying the request, and returns a copy to the applicant.

DOL has also provided a “participant notification” form that AEIs can use to notify the plan if they become eligible for other group health coverage or Medicare and therefore are ineligible for COBRA premium assistance.

Notice of expiration of premium assistance

Employers may use the DOL model Notice of expiration of period of premium assistance to notify AEIs 15 to 45 days before the premium assistance expires, either because the COBRA subsidy period or the AEI’s maximum COBRA coverage period is ending, whichever occurs earlier. The model notice specifies when the subsidy will end and why; whether COBRA can continue and for how long; and what other coverage options might be available, including a special enrollment period for public exchange coverage. The notice also describes how continued COBRA coverage after the subsidy period will affect eligibility for public exchange coverage and premium tax credits. Like the model general notice described above, this notice outlines factors to consider when choosing coverage options.

Notice failure

A failure to satisfy ARPA’s notice requirements will be considered a failure to notify qualified beneficiaries about their right to elect COBRA coverage. Such failures can expose the employer to excise tax penalties of $100 per day for each failure and litigation brought by qualified beneficiaries seeking damages, as well as legal fees and interest.

Timing requirements

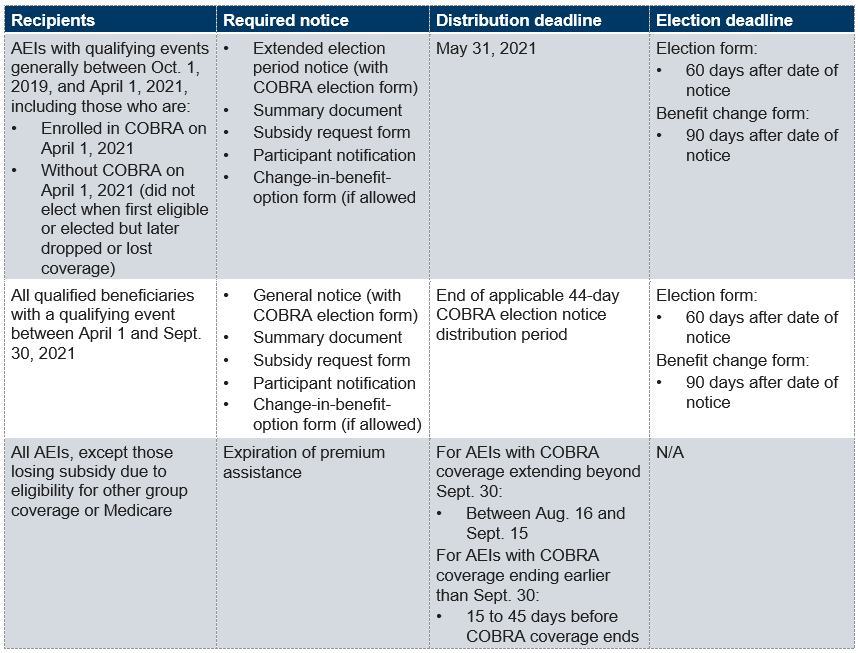

The table below provides an overview of election notice distribution and timing requirements.

DOL clarifications

The model notices and FAQs make a number of useful clarifications regarding the subsidy program:

- Involuntary termination or reduction of hours. The FAQs define involuntary termination as “not including a voluntary termination,” but give no additional information on what an involuntary termination is. Employees terminated for gross misconduct are not entitled to the subsidy since they are not entitled to COBRA. Gross misconduct is not defined under the FAQs, COBRA or its regulations and has been interpreted differently by various courts. Employers should discuss with counsel whether an involuntary termination is for gross misconduct before deciding not to provide COBRA (and the subsidy) to a former employee. DOL’s examples of a “reduction of hours” include reduced hours due to a change in a business’s operating hours, a change from full-time to part-time status, a temporary leave of absence or participation in a lawful labor strike, as long as the individual remains an employee at the time that hours are reduced.

- Public exchange coverage. Individuals with public exchange coverage may be eligible for the premium subsidy if they elect COBRA, but they cannot receive premium tax credits for exchange coverage during the same months they are enrolled in COBRA. Employees with exchange coverage who are eligible for subsidized COBRA coverage because of reduced work hours cannot receive premium credits for the exchange coverage, even if they don’t elect COBRA. AEIs will be eligible for a special enrollment period in the public exchange when the COBRA subsidy ends, and premium tax credits may be available if COBRA coverage ends or is discontinued.

- Time to elect COBRA with premium assistance. Qualified beneficiaries have 60 days from the date of the COBRA notice to elect subsidized continuation coverage. Although additional time to elect COBRA may be available due to the national emergency, if a qualified beneficiary doesn’t elect COBRA within 60 days, they will not be eligible for the ARPA premium subsidy. A similar 60-day deadline applies to those receiving the second election notice.

- Subsidy request. AEIs should complete and return the Request for treatment as an assistance eligible individual form (or a similar form) with the COBRA election form or, if already enrolled in COBRA, separately.

- Outbreak period relief. The election period for COBRA continuation coverage with premium assistance does not interfere with an individual’s existing COBRA election rights, including under the extended time frames provided by the outbreak period relief. The outbreak period relief also provides additional time for AEIs to make COBRA premium payments for periods beginning before April 1 and after Sept. 30, 2021. However, the relief does not apply to the COBRA subsidy notices or related election periods. Employers and plans must provide the notices within the time frames specified in ARPA, and AEIs must elect COBRA coverage within 60 days of the notice date to receive the premium subsidy.

- Premium repayment. Employers should not collect premium payments from AEIs and subsequently require them to seek reimbursement for periods of coverage beginning April 1 and preceding the date of the election notice, if the individual timely requests premium assistance. If AEIs have already paid the premium for a COBRA period covered by the subsidy, they should receive a refund or a credit against future payments (if requested).

Employer next steps

Employers should immediately identify the different groups of qualified beneficiaries who must receive each notice and work with COBRA administrators to ensure timely distribution of these notices and accompanying forms. Employers should also develop and maintain a recordkeeping system for completed Request for treatment as an assistance eligible individual forms and the required records related to the payroll tax offset, including each AEI’s:

- Social security number

- Subsidy amount

- Scope of subsidized coverage (one person or multiple people)

Employers are encouraged to use the DOL’s model notices and forms, since appropriate use is considered good-faith compliance with the content requirements for COBRA and ARPA election notices. However, employers should prepare to customize the model notices to inform qualified beneficiaries about the beginning and end dates of COBRA coverage. This can be tricky for those receiving a second election notice, in which case the start date is April 1 but the end date can vary.

Employers should be on the lookout for guidance from Treasury, which is expected to answer a number of outstanding questions related to the subsidy program.

Related resources

Non-Mercer resources

- COBRA premium subsidy webpage (DOL)

- Pub. L. No. 117-2, the American Rescue Plan Act (Congress, March 11, 2021)

Mercer Law & Policy resources

- Tracking federal COVID-19 laws affecting employee benefits, jobs (March 30, 2021)

- COBRA subsidies in COVID-19 rescue plan require employer action (March 29, 2021)

- Deadline relief continues for health plans and participants (March 4, 2021)