Don’t Go Chasing Waterfalls, or Long End Rates

American hip-hop group TLC released their hit single “Waterfalls” in May of 1995, with a very simple message: “Don’t go chasing waterfalls, please stick to the rivers and the lakes that you’re used to”. At the time, 10-year Treasury yields were at 6.63% and the annualized inflation rate as measured by the consumer price index was 2.8%. With yields once again at multi-decade highs, investors would be wise to take a closer look at their benchmark exposure and remember the wisdom of TLC’s lyrics. Don’t go chasing waterfalls, or in this case, yields. For investors evaluating interest rate exposure, we believe in the current market environment it is prudent to stick to a benchmark-neutral duration stance, rather than extending out the curve in an attempt to “lock in” higher yields.

Given that rates are at multi-decade highs, we have heard increased chatter around the “need to lock in these yields” by extending out the term structure and buying longer-maturity assets. In our opinion, this could be a mistake. While the prospect of higher yields might seem attractive, history suggests that the rate curve is likely to steepen in the future. In such a scenario, assets with maturities of 10-30 years are expected to perform less favorably compared to those with maturities of 5-6 years over the next few years. In simpler terms, investors who have a long benchmark-relative duration strategy, such as holding a Bloomberg U.S. Long Government/Credit index (Long Government/Credit index) with a duration of approximately 13.5 years, may face significant risks from their duration positioning, especially when compared to a Bloomberg U.S. Aggregate index (Aggregate index) investor with a duration of around 6.15 years. Furthermore, the power of duration risk is strong. Locking in higher yields by extending out the curve into longer-maturity assets also means taking much greater duration risk. This has a powerful impact on your expected return profile and leads to much higher volatility of returns, as we will illustrate below.

Let us pause to explore a few key reasons why we believe that the broad rate curve is biased towards steepening from here: Current valuations and anticipated Federal Reserve (Fed) policy rate cuts.

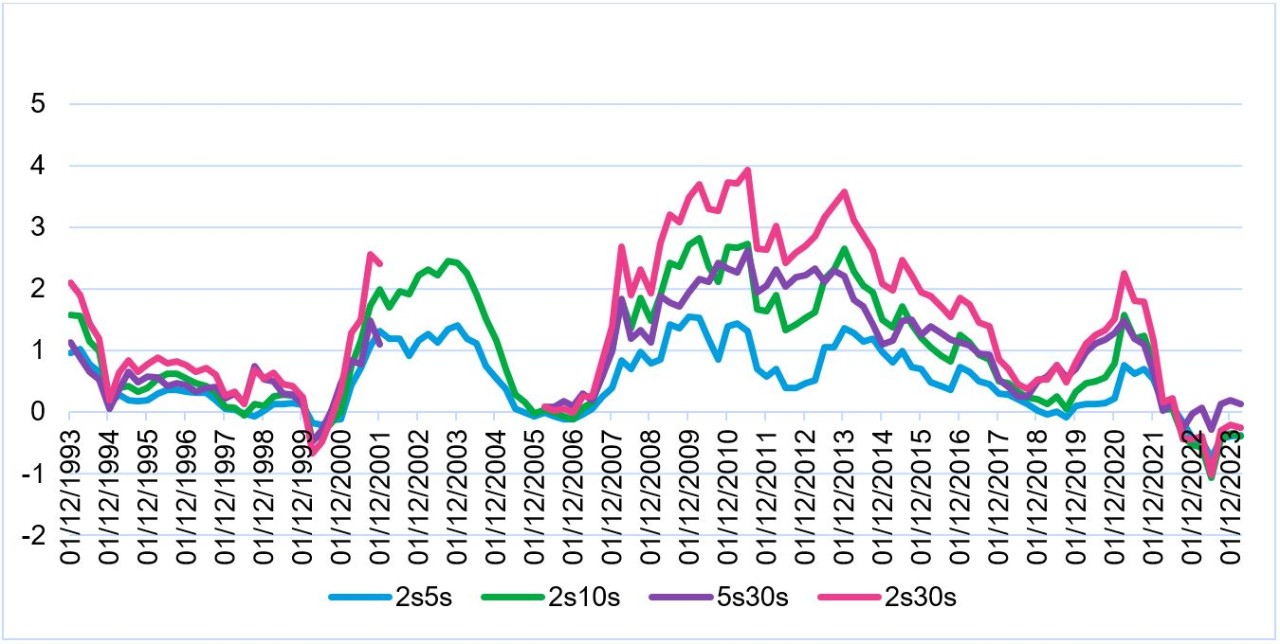

Presently, the broad rate curve rests at extremely flat, and in some cases inverted, levels (chart 1). Looking back over time, we typically do not see the curve remain inverted for long, and we expect history to eventually repeat itself. Going forward, the curve could re-steepen to more historically average levels. As this normalization happens, 10-30y assets would underperform 5-6y assets. Investors must therefore be wary of holding structurally longer-duration assets to prevent potential underperformance vs. the Aggregate index.

Chart 1: Historical Rate Curve Chart

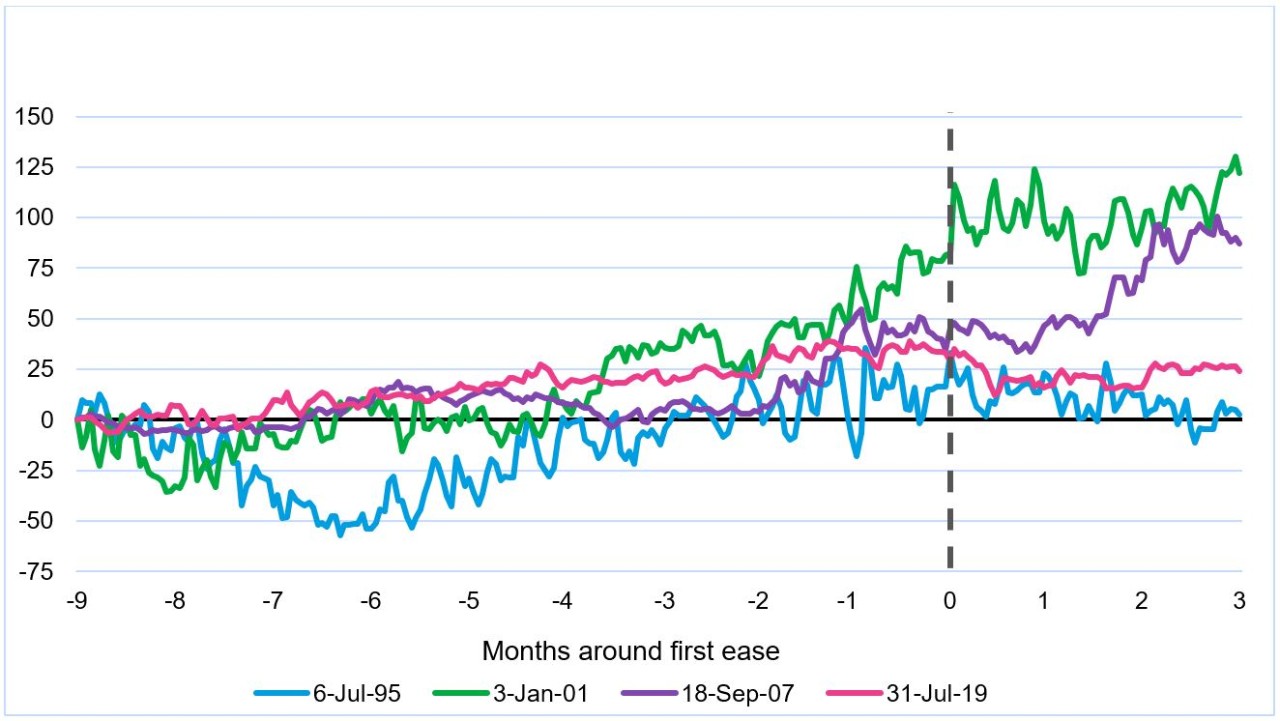

Chart 2: Cumulative change in 5s/30s Treasury curve in the months around the first ease in a Fed easing cycle*; bp

Source: JP Morgan

*Dates used: 7/6/1995, 1/3/2001, 9/18/2007, 7/31/2019

The story is similar in 1995, with the 5s30s curve steepening 75bps trough to peak, while the curve steepening in 2001 was even more pronounced: 30y assets underperformed 5y assets by 150bps during the nine-month period surrounding the first policy cut in 2001! As the Federal Reserve prepares to embark on a rate-cutting cycle, investors should be wary of extending duration beyond their policy benchmark, and being caught flatfooted as the yield curve begins to normalize and longer-duration assets potentially underperform.

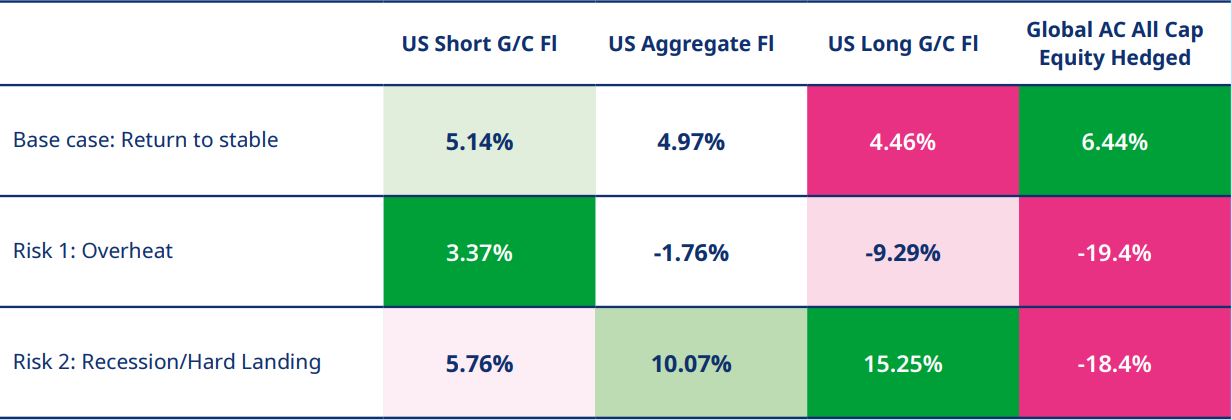

Let us take a moment to examine how an index with a longer maturity (and duration) profile could be expected to perform in various economic scenarios. We ran an analysis to illustrate how a Long Government/Credit index would perform relative to the Aggregate index and the Bloomberg 1-3 Yr U.S. Gov/Credit index (Short Government/Credit index) in three potential market scenarios. Turning our attention to chart 3 below, we see the expected performance of each of the three indices in the Mercer base-case economic scenario, as well as two risk scenarios – overheat and hard landing.

Chart 3: Expected Annualized Return

When considering the base-case scenario in isolation, the three fixed-income indices have similar expected returns, and it is not readily apparent that there is a strong case to be made for why investors should not extend out the curve to Long Government/Credit. However, when the expected returns under the two “risk” scenarios are factored into the analysis, the power of duration becomes evident. The volatility of returns for a long-duration Government/Credit index is extremely high, with sharp losses in the scenario where inflation remains higher than expected, for longer than expected. This performance analysis illustrates the risks of extending your exposure relative to your base index, as the volatility of returns for a Long Government/Credit index is much higher and shows a bigger downside risk versus Aggregate index exposure.

In conclusion, investors should not chase yields and extend out to longer-maturity assets. Extending means taking greater duration risk, which can lead to much higher volatility of returns. From a monetary policy perspective, and a valuation perspective, now is not the time to move into longer-maturity exposure. There are compelling reasons to believe the curve is biased to re-steepen from here, which could mean longer-duration assets underperform. If you have discovered out-of-benchmark duration exposure while reviewing your portfolio, now is a wonderful time to realign. Don’t let your duration creep, creep.