S&P 1500 Pension Funded Status Decreased by 2 Percent in January

February 9, 2023

United States, New York

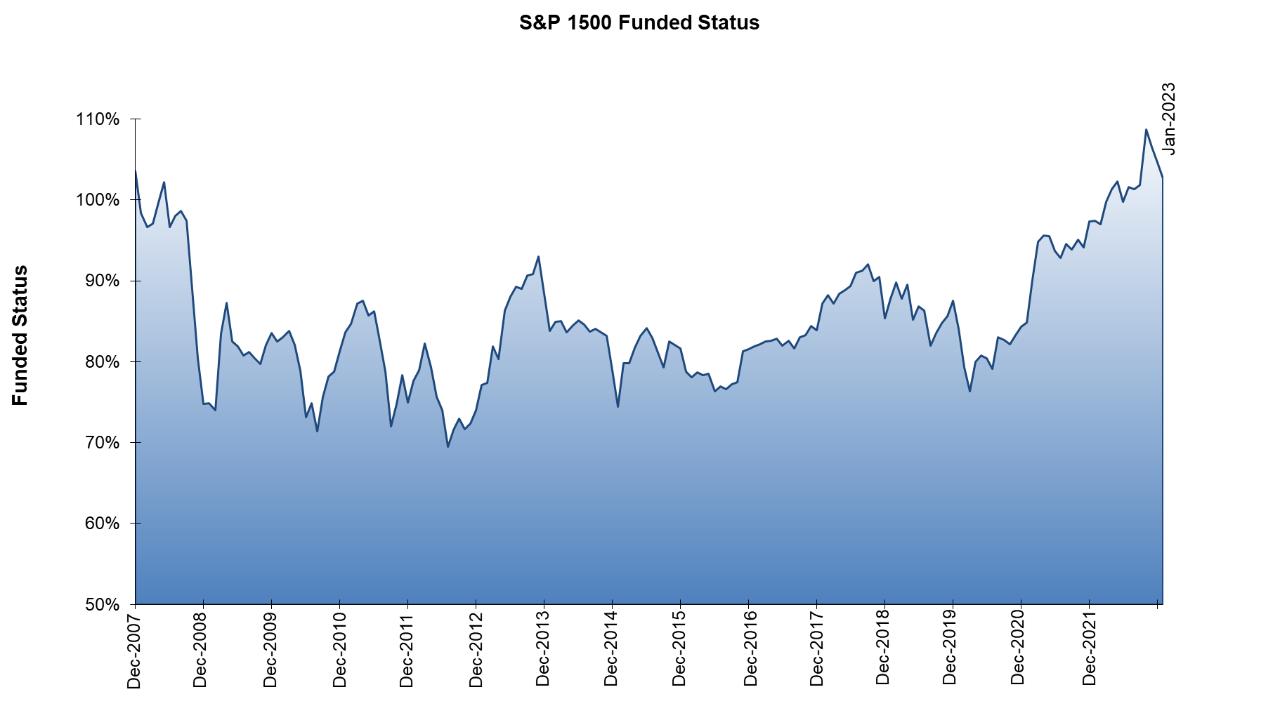

The estimated aggregate funding level of pension plans sponsored by S&P 1500 companies decreased by 2 percent in January 2023 to 103 percent as a result of a decrease in discount rates partially offset by an increase in equity markets. As of January 31, 2022, the estimated aggregate surplus of $54 billion USD decreased by $22 billion USD as compared to a surplus of $77 billion USD measured at the end of December according to Mercer,1 a global consulting leader and a business of Marsh McLennan (NYSE: MMC).

The S&P 500 index increased 6.18 percent and the MSCI EAFE index increased 8.05 percent in December. Typical discount rates for pension plans as measured by the Mercer Yield Curve decreased from 5.24 percent to 4.77 percent.

“Pension funded status for the S&P 1500 fell two percent in January as plummeting discount rates offset a strong start to 2023 for equity markets,” said Scott Jarboe, a Partner in Mercer’s Wealth Business. “Equities increased on continuing signs that inflation may be slowing and in anticipation the Fed may continue to slow interest rate hikes. However, discount rates fell around 50 bps in January, increasing liabilities significantly resulting in a net drop in funded status. With funded status continuing to decrease, plan sponsors may see the window of opportunity fading on some de-risking and risk transfer opportunities. However, certain risk transfer strategies, such as lump sum windows, may be more attractive now that rates have dropped significantly since late last year.”

Mercer estimates the aggregate funded status position of plans sponsored by S&P 1500 companies on a monthly basis. Figure 1 (below) shows the estimated aggregate surplus/(deficit) position and the funded status of all plans sponsored by companies in the S&P 1500. The estimates are based on each company’s latest available year-end statement2 and by projections to January 31, 2023 in line with financial indices. The estimates include U.S. domestic qualified and non-qualified plans, along with all non-domestic plans. The estimated aggregate value of pension plan assets of the S&P 1500 companies as of December 31, 2022 was $1.73 trillion USD, compared with estimated aggregate liabilities of $1.65 trillion USD. Allowing for changes in financial markets through January 31, 2023, changes to the S&P 1500 constituents, and newly released financial disclosures, at the end of January the estimated aggregate assets were $1.82 trillion USD, compared with the estimated aggregate liabilities of $1.77 trillion USD. Figure 2 shows the discount rates used in Mercer’s pension funding calculation.

Notes for editors

Information on the Mercer Yield Curve is available at http://www.mercer.com/pensiondiscount.

The Mercer US Pension Buyout Index may be accessed at https://www.mercer.com/en-us/insights/investments/market-outlook-and-trends/pension-buy-out-index.html.

Unless otherwise stated, the calculations are based on the Financial Accounting Standard (FAS) funding position and include analysis of the S&P 1500 companies.

Source: Mercer, January 2023

Figure 2: High Quality Corporate Bond Yield and S&P 500 data points

| Date | High Quality Corporate Bond Yield | S&P 500 Index |

December 31, 2011 |

4.55% |

1,257.60 |

December 31, 2012 |

3.71% |

1,426.19 |

December 31, 2013 |

4.69% |

1,848.36 |

December 31, 2014 |

3.81% |

2,058.90 |

December 31, 2015 |

4.24% |

2,043.94 |

December 31, 2016 |

4.04% |

2,238.83 |

December 31, 2017 |

3.56% |

2,673.61 |

December 31, 2018 |

4.19% |

2,506.85 |

December 31, 2019 |

3.18% |

3,230.78 |

December 31, 2020 |

2.32% |

3,756.07 |

December 31, 2021 |

2.76% |

4,766.18 |

March 31, 2022 |

3.67% |

4,530.41 |

April 30, 2022 |

4.35% |

4,131.93 |

May 31, 2022 |

4.38% |

4,132.15 |

June 30, 2022 |

4.64% |

3,785.38 |

July 31, 2022 |

4.35% |

4,130.29 |

August 31, 2022 |

4.70% |

3,955.00 |

September 30, 2022 |

5.41% |

3,585.62 |

| October 31, 2022 | 5.73% | 3,871.98 |

November 30, 2022 |

5.12% |

4,080.11 |

December 31, 2022 |

5.24% |

3,839.50 |

| January 31, 2023 | 4.77% | 4,076.60 |

About Mercer

1 Figures provided by Mercer Investments LLC.

2 Source of financial statement data: Standard & Poor’s Capital IQ. Standard and Poor’s is a division of The McGraw-Hill Companies, Inc. This may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of THEIR CONTENT, INCLUDING ratings. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold, or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.