Safeguarding healthcare affordability in a time of inflation

As plan sponsors work to adapt benefit strategies for 2024, they have to prepare for the impact of inflation on their health plan costs. But inflation is also creating financial stress for employees at all income levels – and making it harder for low-earners simply to meet normal monthly expenses, let alone handle an unexpected medical bill. In our 2022 National Survey of Employer-Sponsored Health Plans, about two-thirds of large employers (those with 500 or more employees) said that “improving healthcare affordability” was an important or very important health program priority for the next few years.

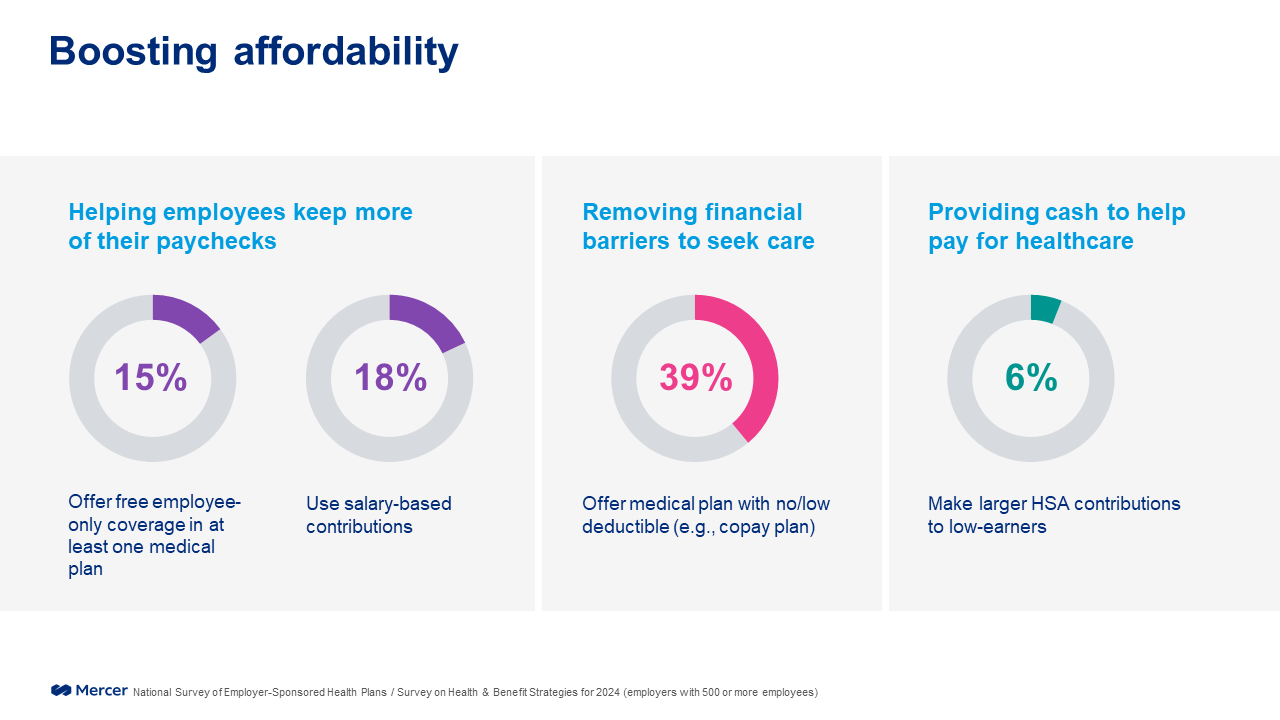

In our recent Survey of Health and Benefit Strategies for 2024, we asked about three ways employers can boost healthcare affordability. One is by lowering the cost of coverage to help employees keep more of their paychecks. Some large employers – 15% – are offering free employee-only coverage in at least one medical plan, up from 11% in last year’s survey. Others are tying the size of the paycheck deduction to the level of pay. In 2022, according to the National Survey, the use of salary-based contributions rose just slightly among all large employers (from 17% to 18%), but from 29% to 34% of employers with 20,000 or more employees.

Another way to address affordability is to ease financial barriers to seeking care. High deductibles can be hard for those with little savings or chronic health conditions. Well over a third of large employers offer a plan option with no deductible or a very low deductible and minimal out-of-pocket cost when care is needed, such as a copay plan. Finally, to make a high-deductible plan more manageable, some employers are providing larger HSA account contributions to employees who earn less.

Other support for financial wellness

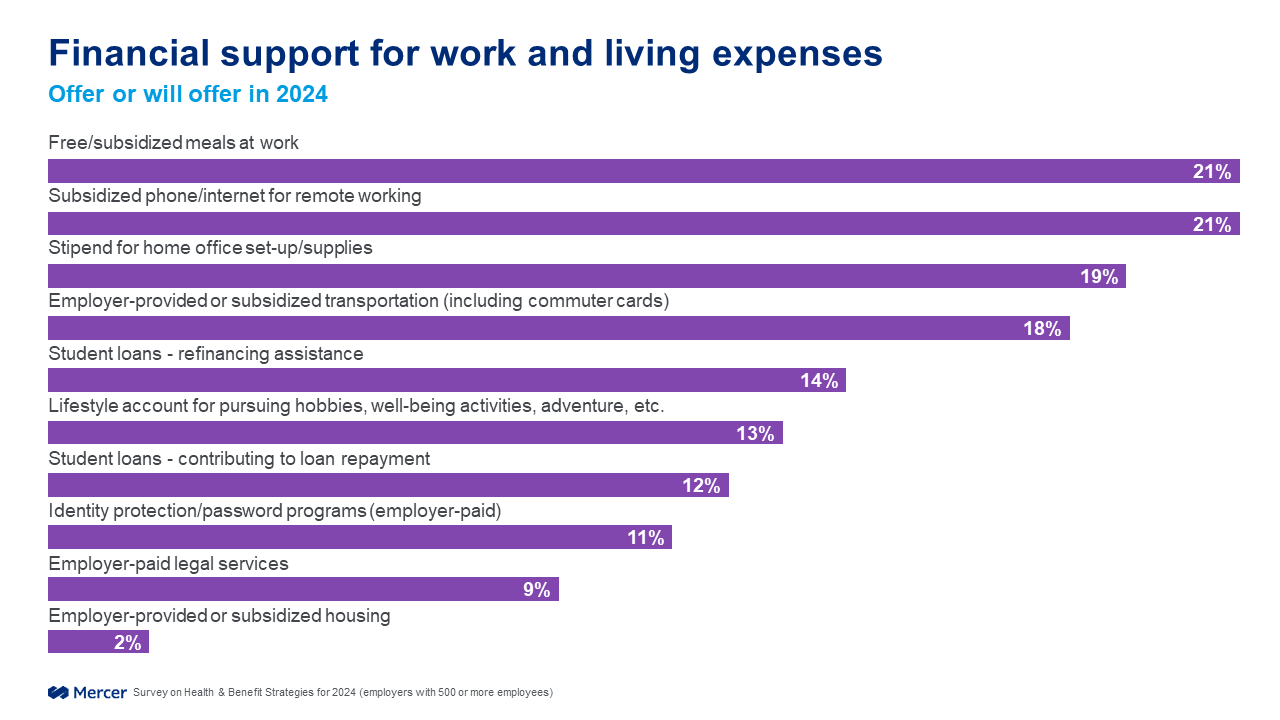

Employers are providing other forms of support to address financial wellness. Free or subsidized meals at work are offered by 21% of large employers or planned for 2024, and employer-provided or subsidized transportation (such as a commuter card) is provided by 18%; both benefits may also serve to encourage employees to work onsite. At the same time, about the same percentage of employers are assisting those working remotely by subsidizing phone and/or internet costs (21%) or providing a stipend for setting up and maintaining a home office (19%).

Student loans can be a major financial burden, and 12% of large employers will contribute to loan repayment, while 14% provide refinancing assistance.

A small but growing number of organizations offer “lifestyle accounts” to help employees to afford life-enhancing pursuits such as hobbies, well-being activities, or adventure. The survey found 13% of large employers offer a lifestyle account or plan to in 2024. While this benefit is most common among high-tech employers (32%), it is also offered by nearly one in ten employers in wholesale/retail.

Looking ahead to 2024, it seems likely that employers will be challenged to absorb higher healthcare cost increases. But budget concerns must be balanced with the need to safeguard healthcare affordability. And, especially in a time of inflation, employees value benefits that support their financial well-being – an important consideration for employers looking to differentiate themselves in a tight labor market.

The Mercer Survey on Health & Benefit Strategies for 2024 was designed to discover how employers will prepare for rising health care costs while continuing to adapt benefit strategies for 2024 to improve attraction and retention and better meet the needs of the whole workforce. The survey was conducted from February 14 through March 10, 2023. The results in this post are based on 512 organizations with 500 or more employees. In total 721 organizations participated, from all industries and sizes (fewer than 500 employees: 29%; 500-4,999 employees: 45%; 5,000 or more employees: 26%).