ERISA plan sponsors are responding to heightened fiduciary risk

Although employers sponsoring ERISA-covered health and welfare plans have always had fiduciary responsibilities, concern about fiduciary risks has grown recently for a number of reasons, including newly available data as federal transparency requirements take effect, increased Department of Labor (DOL) focus on health plan investigations, and potential litigation. Employers are responding by reassessing their fiduciary roles and responsibilities, and revisiting strategies to manage risk.

Mercer recently surveyed 311 employers to learn their views on a number of health policy issues, including their ERISA fiduciary duties. Almost three-fourths of respondents indicated that they have taken notice: 28% said they have recently reassessed their welfare plan oversight and fiduciary responsibilities and another 43% plan to do so in the near future.

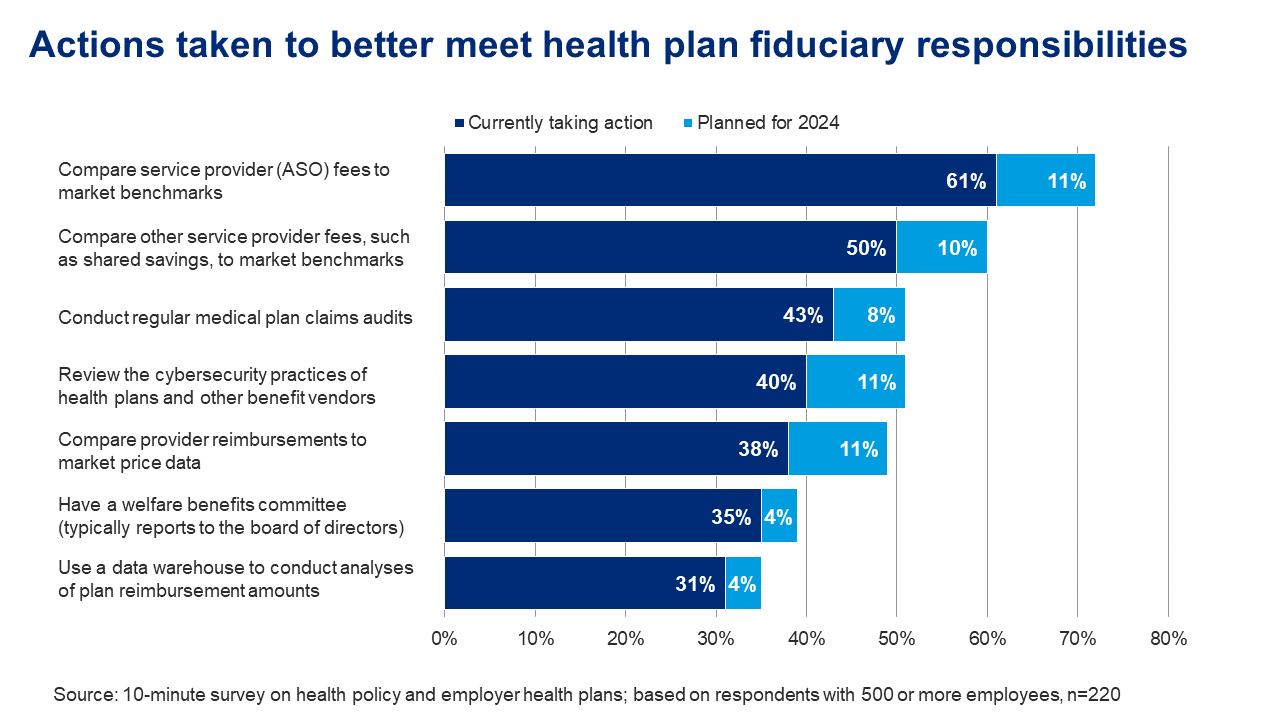

Many of the actions that employers can take to meet fiduciary responsibilities are already quite common, especially those focused on ensuring money spent on health coverage is spent wisely – for example, comparing ASO and other service provider fees to market benchmarks. In addition, about half of respondents conduct regular medical claim audits (or have one planned for 2024), which can help identify overpayments and other problems with provider reimbursement.

But employers are taking new actions to meet fiduciary responsibilities as well. Cybersecurity has become a central business function in recent years, and working to secure plan data is critically important. Two-fifths of survey respondents currently review the cybersecurity practices of health plans and other benefits vendors, while 11% plan to do so in 2024 and an additional 31% are at least considering it. As healthcare price information becomes available under new transparency requirements, some employers have begun comparing reimbursement levels in their provider networks to market price data.

Finally, by 2024 nearly two-fifths of respondents will have established a welfare benefits committee. Such committees are commonly used for retirement benefits and seem likely to continue to grow on the health and welfare side, with another 18% of respondents are considering this step.

With all that in mind, it’s a great time to think about a fiduciary check-up. Here’s a simple checklist to get started:

Ensure governance is up to date. Reassess with counsel relevant fiduciary roles, responsibilities, delegations, and processes. Review your fiduciary insurance policy to make sure it is appropriate.

Analyze plan costs. Understand how increased plan costs affect participants. Prepare to analyze those costs, as well as plan operations, using the vast amount of newly available transparency data. Although the transparency data currently is not easy to analyze, the data will likely become more useful over time. Just recently, CMS announced file standardization improvements to help deliver on the promise of hospital price transparency.

Monitor recent litigation and agency enforcement efforts. Track lawsuits and DOL enforcement priorities related to group health plans and their service providers. Some recent cases concern service provider fees (including “hidden” fees), cross plan-offsetting and plan failures to obtain data from service providers. Consider whether changes to plan operations are appropriate to reduce risk.

Focus on service providers. Select and monitor service providers based on their qualifications, quality of services, and compensation, including broker and consultant compensation disclosures. Review service provider agreements with legal counsel. Service providers should mitigate cybersecurity risks and make plan data available when required or requested.

Don’t forget the basics. Ensure timely compliance with ERISA’s reporting and disclosure requirements, including long-standing duties like filing a Form 5500 and newer obligations such as the written comparative analysis required under the Mental Health Parity and Addiction Equity Act (MHPAEA) and the first annual gag clause attestation required by Dec. 31, 2023. Review all other applicable fiduciary matters (e.g., ERISA plan asset and bonding issues) for compliance.

Document your work. Maintain files to document the steps your organization has taken to meet your fiduciary responsibilities, including updating plan documents and communications as needed.

For more information about ERISA fiduciary duties and data privacy and security, see our GRIST: Top 10 health, leave benefit compliance and policy issues in 2024.