Growing with below investment grade fixed income

The fixed income universe encompasses a wide range of securities up and down the credit quality spectrum.

When constructing total portfolio solutions, investors often allocate to fixed income for liquidity and income. However, that view minimizes the full potential of the asset class. The fixed income universe encompasses a wide range of securities up and down the credit quality spectrum. When devising an asset allocation strategy, investors should consider all the tools available to them, incorporating investment grade (IG) and below-investment grade (Below IG) fixed income.

This paper defines the building blocks of the Below IG opportunity set and the role it plays in institutional portfolios to help drive growth. Subsequent publications will dive deeper into the credit quality spectrum and the potential opportunities we see active asset managers unlocking.

What is Below Investment Grade Fixed Income?

Below IG fixed income offers both higher income and opportunities for capital appreciation by assuming more credit risk. This diversifies the interest rate risk that is inherent in IG fixed income.

Below is a guide to Mercer’s various reference portfolios where Below IG can play an important role.

Figure 1: Below Investment Grade Fixed Income Overview

Broadly, investing in Below IG fixed income is effectively lending to borrowers with higher debt burdens and lower quality balance sheets compared to IG borrowers, thus offering a yield premium for the increased risk of default. Below IG sectors typically encompass high-yield corporate bonds, bank loans, and hard-currency emerging market debt, but can also be expanded to include other Below IG securities such as non-agency securitized debt (CLOs), preferred securities, and local currency emerging market bonds. With an opportunity set spanning geographies, currencies, varying degrees of liquidity and structures, and features such as fixed or floating interest rates, there are numerous alpha levers and risk factors that differentiate the segment.

Figure 2: Comparing Below IG and IG

(The representative blend of Below IG fixed income investments – 1/3 US HY, 1/3 Bank Loans, 1/3 EMD – provides investors with an extensive range of exposures, including floating rate instruments, lower credit quality bonds, and geographic diversity. This diversified blend allows investors to access various opportunities within the Below IG fixed income space, enabling them to potentially benefit from different market dynamics and enhance their overall investment strategy.)

The Role of Below Investment Grade Fixed Income in Institutional Portfolios

This fixed income segment has four important features: yield enhancement, fixed income risk factor diversification, inflation protection, and a rich opportunity set for active management. Importantly, Below IG fixed income allocations are often customized to prioritize the objectives most relevant to a particular client.

Figure 3: Role of a Below IG allocation

Return Seeking Features

Defensive Features

The increased yield derived from additional credit risk and the rich opportunity set for active management are important features. Below IG borrowers are often highly indebted, offering little protection to lenders and therefore attracting lenders by paying a premium. This premium can help enhance returns as yield is the primary component of fixed income returns over the long term. In addition, Below IG borrowers span a broad array of industries, geographies, credit profiles and lending needs that differ from the IG market. This opens numerous avenues to employ active management to distill a large opportunity set down to the most attractive opportunities such as borrowers or sectors benefiting from idiosyncratic catalysts or thematic tailwinds. This fixed income segment, however, can experience elevated volatility, creating a wider dispersion in potential outcomes for investors.

This dispersion of potential outcomes means that risk considerations are paramount, as credit losses can permanently impair portfolios. However, there are some sources of downside protection that Below IG fixed income offers in a portfolio context:

- Relative to IG bonds, they serve as a buffer against rising interest rates. Below IG bonds are less sensitive to changes in interest rates due to shorter maturities and high income payouts.

- Some securities have floating interest rates (bank loans, CLOs), which buffers bondholders from rising rates.

- They diversify risk factors by offering exposure across a range of industries, borrower profiles, lending structures, and geographies that diverge from IG markets. For example, the inclusion of hard currency emerging market debt involves lending to emerging sovereign nations. These nations’ economies may have different economic or demographic policies and experience trends that result in a differentiated lender profile compared to domestic IG borrowers.

Figure 4: Correlation over 30 years and 3 months ending March 24

To help quantify potential diversification benefits, the below analysis outlines three portfolios with varying exposures to below IG fixed income. Overall, Below IG fixed income demonstrates an increased correlation with equities, providing lower diversification benefits than those offered by IG fixed income. It also has larger drawdowns than IG fixed income. Nonetheless, it still offers some diversification benefit. As demonstrated by this simplified model, a mix of equities, Below IG fixed income and IG fixed income may result in the most efficient portfolio as measured by return per unit of additional risk taken, rather than a portfolio of just equities and IG fixed income with similar volatility. The more diversified portfolio, however, underperforms an 80%/20% equity/IG fixed income portfolio but demonstrates much lower volatility. Which portfolio is appropriate depends on client objectives.

Figure 5: Simple Asset Allocation Scenarios

The State of Below Investment Grade Fixed Income Today

A significant factor in today’s investment landscape impacting the relative attractiveness of Below IG fixed income is current yields. Today’s yield levels are much more attractive than in the past decade. The US 10-Year Treasury yield, a measure of risk free returns, yielded 4.2% at the end of Q1 2024 relative to less than 1% four years ago. When high base rates are paired with a credit spread to compensate for additional credit and liquidity risk, the all-in yield on Below IG quickly becomes attractive.

Figure 6: US 10-Year Treasury Yield over 20 years

The Below IG fixed income market today is not without risks. One consistently surprising feature of this yield environment is the fact that the increase in interest rates has not resulted in the severe domestic and global recessions that were widely predicted. Instead, companies continue to be able to service debt and defaults remain benign, a result of a healthy economy and borrowers locking in debt during the period of low interest rates. Valuations across the fixed income credit market have quickly become “rich” (as demonstrated by credit spreads falling in the below chart), creating an environment for investors where all-in yields remain attractive but spreads are relatively tight. Against this backdrop, security selection and active management remain paramount.

Figure 7: High Yield Credit Spread over 20 years

Conclusion

Appendix

Source: MSCI BarraOne. For illustrative purposes.

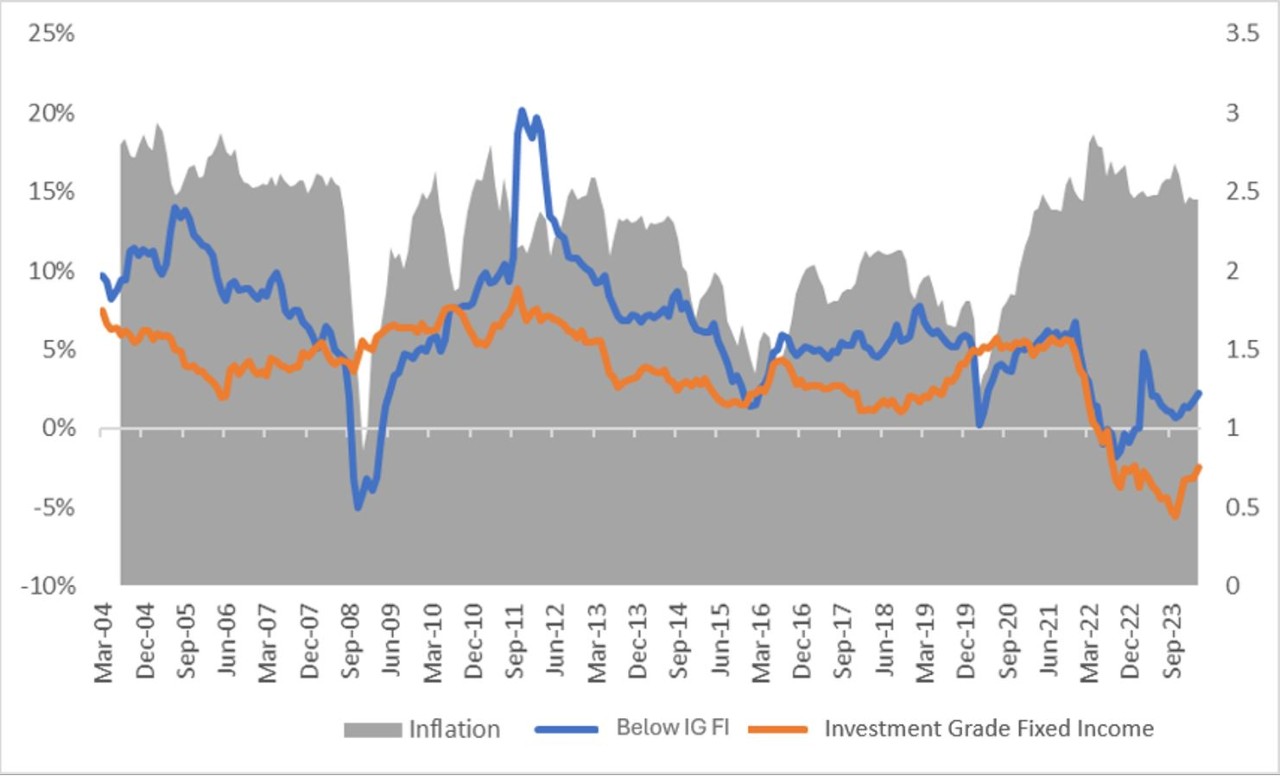

Figure 9: Inflation & Rolling 3-Year Returns Performance: Below IG vs Bloomberg US AGG

Source: Bloomberg & FRED. For illustrative purposes.

Article contributors:

Elijah McGowen, Senior Investment Researcher

Laura Nguyen, Investment Associate