Why execution (not access) defines success in private markets

31 October 2025

In our view, access to private markets and alternatives has never been easier. Doing it well has never been harder. So how do you seek to build a portfolio that delivers rather than disappoints?

The case for private markets and alternatives is now widely accepted. Once a niche allocation for institutional giants, private equity, private credit, infrastructure and real estate are increasingly reshaping portfolios of all sizes – offering returns, diversification and capital market exposure that listed assets do not appear to replicate.

However, these opportunities come with higher fees, longer timeframes and a wider range of possible outcomes. According to Michael Forestner, Mercer’s Global CIO of Private Markets and Alternatives Portfolio Construction, execution is where performance can be made or lost.

“Separating good from great is probably the hardest thing to do,” he told financial advisers at Mercer’s recent Private Markets and Alternatives Masterclass, held in collaboration with Portfolio Construction Forum. “Once you’re exposed to private markets”, the results can depend on the portfolio details that are often overlooked.”

So what could financial advisers and wealth managers be watching for? Forestner points to three areas: secondaries, hidden costs and portfolio complexity.

Key takeaways

To build an effective portfolio with private markets and alternatives, financial advisers could consider:

-

Using secondaries to bypass the J-curve trap

-

Watching for hidden costs in new structures

-

Matching portfolio complexity to client objectives

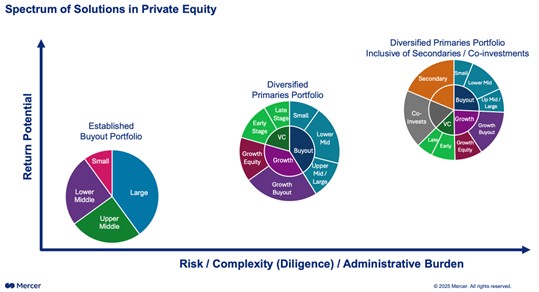

Use secondaries to bypass the J-curve trap

Private market investments typically bleed cash for several years before generating positive returns –the so-called J-curve effect. It’s considered to be structural, predictable and problematic for investors seeking steady performance.

Secondary markets can help flatten that curve.

Private equity generally breaks into three components: primary funds, co-investments and secondaries. Most financial advisers focus on primaries. But secondaries – which buy into existing private equity portfolios already generating returns – can produce positive cash flow within one to three years.

“Anytime we’ve had investors who skipped secondaries because there was something about them they didn’t like, they’ve tended to regret it,” Forestner said.

Secondaries can also reduce another hidden drag: uncalled capital. Commitments to primary funds can sit idle for years before being deployed, not earning anything in the meantime.

While secondaries may carry higher transaction costs, Forestner describes them as “the most evergreen strategy in private markets,” with consistent performance that may justify the premium.

Watch for hidden costs in new structures

Secondaries can help improve performance, but how financial advisers access them can matter. Semi-liquid fund structures appear to be gaining popularity, promising periodic redemptions, lower minimums and institutional-style diversification without decade-long lock-ups.

However, the fine print deserves scrutiny.

“Many semi-liquid funds hold each other’s shares,” Forestner cautioned. Instead of broad private market exposure, investors may be buying into a circular pool of the same underlying assets – sometimes with multiple fee layers that quietly erode returns.

Add the mandatory cash buffers required for redemption windows, and performance can lag even further.

“Some alternative funds are simply too expensive, relative to the underlying yield,” he said.

The key is understanding what you’re truly investing in: the real assets and the total fees, net of liquidity buffers.

“If you’re going to get into the semi-liquid space, you need to monitor these funds,” Forestner advised. “There might be a point where the portfolio shifts and you want to exit – but you’re unlikely to know unless you’ve done the work.”

Competition is likely to eventually compress fees for these newer structures. Until then, due diligence can separate financial advisers who deliver value from those who merely deliver access.

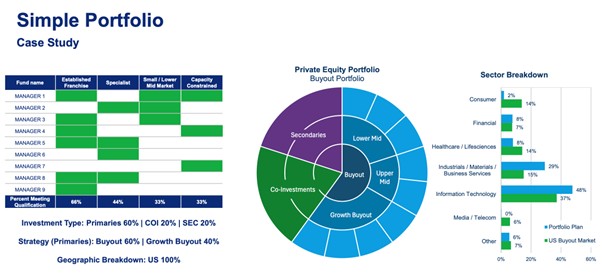

Match portfolio complexity to client objectives

Complexity adds value if it directly serves a client goal. Many private markets portfolios, Forestner noted, are more complicated than they need to be.

“Everything in the portfolio needs to have a purpose. What value are you bringing to your clients?” he said.

For private wealth clients or smaller institutions, a straightforward buyout-focused portfolio may be enough — offering trusted investment managers and steady strategies without venture-capital-style volatility.

“If it’s not complicated when you look under the hood, it’s a sleep-at-night portfolio,” Forestner said.

Both approaches can work. The key is matching portfolio design to the client’s risk tolerance, objectives – and your ability to execute.

Execution, Forestner warned, is exponentially harder in private markets.

“In public equities, picking a mediocre fund might cost you one or two per cent a year. In private equities, backing the wrong investment manager can mean the difference between top-quartile returns and capital you never see again.”

Before adding another layer of complexity, financial advisers could ask: What client outcome does this serve? Can I access genuinely differentiated investment managers? And do I have the due diligence resources to monitor them properly?

Close the construction capability gap

Private markets span multiple geographies, currencies, sectors and liquidity profiles – and every decision compounds over a decade or more. Without deep research capability, ongoing monitoring and access to leading investment managers, even well-intentioned allocations can disappoint.

The question may not be whether private markets deserve a place in client portfolios, but whether financial advisers have the infrastructure to manage them effectively.

Mercer works with financial advisers to bridge that gap. With approximately 3,000 professionals working to improve investment outcomes for participants both in Australia and around the world and covering over 7,000 strategies, Mercer helps construct institutional-grade private market portfolios – from investment manager selection and due diligence to liquidity management and ongoing oversight.

For financial advisers, that capability can be the difference between simply accessing private markets and delivering them with conviction.