DB pensions weather headwinds to end Q2 in a stronger position: Mercer

Toronto, July 4, 2023

Positive asset returns and an increase in bond yields led to a continued improvement in the financial positions of most Canadian defined benefit (DB) pension plans in the second quarter of 2023.

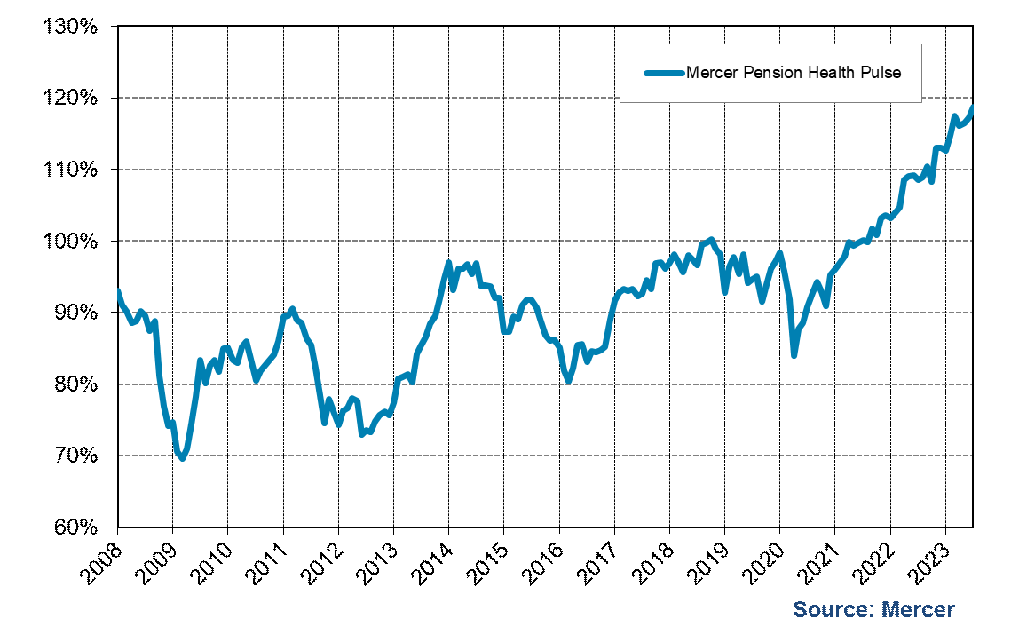

The Mercer Pension Health Pulse (MPHP), a measure that tracks the median solvency ratio of the DB pension plans in Mercer’s pension database, increased from 116% at the end of the first quarter of 2023 to 119% at June 30, 2023. This increase occurred despite a scare around the U.S. debt ceiling, and the lingering after-effects of the banking crises.

In the quarter, pension funds’ investment returns were mostly positive. Combined with increases in bond yields, which reduced DB plan liabilities, this led to improvements in the financial position of most DB plans.

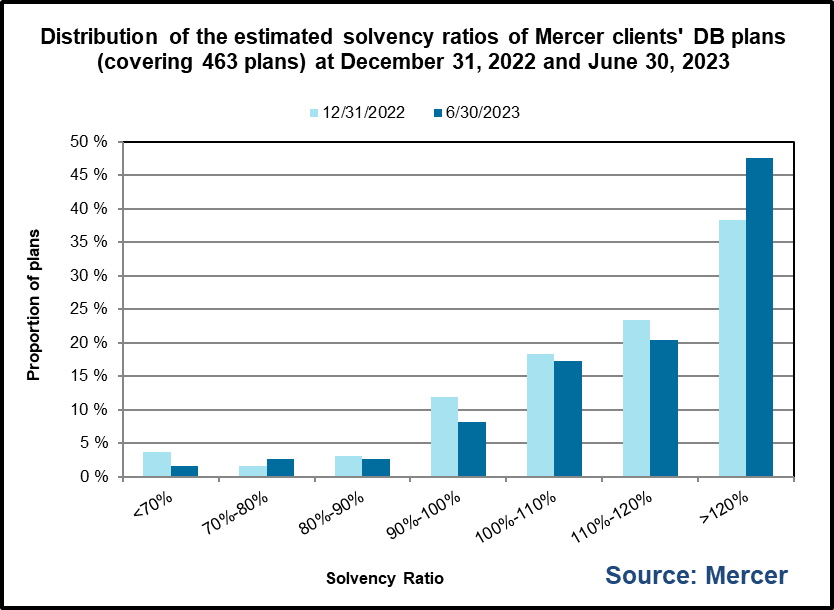

Of the plans in Mercer’s pension database, at the end of the second quarter 85% are estimated to be in a surplus position on a solvency basis (vs. 83% at the end of Q1). Approximately 8% are estimated to have solvency ratios between 90% and 100% (vs. 9% at the end of Q1), 3% are estimated to have solvency ratios between 80% and 90% (vs. 4% at the end of Q1), and 4% are estimated to have solvency ratios less than 80% (unchanged from the end of Q1).

“DB pension plans’ funded positions continue to benefit from higher interest rates, with many plans now in surplus positions,” said Ben Ukonga, Principal and leader of Mercer’s Wealth business in Calgary. “The question that should now be on plan sponsors’ minds is how best to manage this surplus, and potentially locking it in, in order not to re-experience the dark days of significant pension deficits.”

While market conditions have been favourable to DB pension plans, many risks remain. Inflation continues to be elevated, and remains above central banks’ target ranges despite the significant actions already taken by many central bankers globally. In Canada, after pausing the increase of its key policy interest rate in January 2023, the Bank of Canada increased the rate again in June 2023. A rate that was 0.25% at January 2022 now sits at 4.75% at June 2023. Will further increases be required if the Bank of Canada continues to believe (or their data suggests) that inflation will remain high? Or will the recently reported decline in inflation lead to another pause?

The question remains: what impact will these interest rate increases have on the investing and spending plans of Governments, corporations and households, and their respective abilities to service the debt loads accumulated over the years? Some organizations have already announced downsizing plans, and many households are struggling with the impact of higher inflation on personal spending and higher interest rates on mortgage costs – all of which could lead to a reduction in spending and investing. Will these reductions be enough to bring down inflation? In addition, are the spending plans of the Federal Government, unveiled in the 2023 Federal budget, at odds with the inflation reduction aims of the Bank of the Canada? Will this require the Bank of Canada to continue with its interest rate increases and quantitative tightening, more than it otherwise would?

And moving forward, is a recession on the table? Globally, there is the risk of central banks overshooting the required policy restrictions to reduce inflation, causing a harder slowdown in the global economy than is warranted and increasing the risk of a hard landing global recession. Many market observers already believe a recession is on the horizon, although opinions differ on how deep and long it will be.

The global markets breathed a collective sigh of relief with the raising of the US Government debt ceiling. But political polarization in the United States will likely continue to worsen, especially with the 2024 Presidential election cycle kicking off. Will there be another standoff soon, adding to global uncertainty?

Further, with continued geo-political tensions between the US and China, the war in Ukraine, and increased calls for a decoupling of global supply chains (and an increase in “friendshoring”), the global economy is in a delicate balance and could easily tip into a recession.

For DB plans in surplus positions, plan sponsors should not only be thinking of how best to utilize the surplus, but also how best to protect that surplus if a recession were to occur. They should be evaluating what impact alternative market conditions will have on the surplus, plan financial position and their business. Will they be able to withstand a downside event like the significant market decline experienced in March 2020 at the onset of the COVID-19 pandemic? And what impact will such a downside event have on their pension plan and organization? They should be reviewing their risk appetite, risk exposures and governance processes, and making the necessary adjustments to ensure they are well prepared for whatever the future holds.

“Despite the improved financial positions of most DB plans, DB plans sponsors need to remain vigilant given the level of uncertainty that still exists”, concluded Ukonga. “Plan sponsors should understand and be comfortable with the risks they are taking and hedge or transfer the risks they do not want to retain.”

From an investment standpoint

A typical balanced portfolio would have posted a return of 2.1% over the second quarter of 2023. The global economy continued to show resilience with consumer demand, normalization of supply chains and low energy prices. However, high core inflation remained a risk with global central banks continuing to maintain their tight monetary polices.

Global equity markets increased through the majority of the quarter, but returns were divergent depending on the region. Headline inflation did not materially change since the end of March, pressuring central banks to further increase key interest rates around the world. In the U.S., a resilient economy supported by strong labour markets led to risk asset outperformance despite the regional banking stability issues and debt-ceiling uncertainty over the period. EAFE markets delivered positive returns backed by stable economic data supporting a soft landing outlook, but currency impacts diminished returns in Canadian dollars. Emerging markets ended the quarter reporting negative returns due to ongoing geopolitical instabilities, China’s weak growth figures and currency movements.

Bond returns were generally negative, as yields rose and credit spreads widened slightly in the U.S. Broad commodity returns finished the quarter in the negative, partially driven by oil prices. Oil prices fell, despite announcements of production cuts from OPEC and purchases by the US Department of Energy to replenish the Strategic Petroleum Reserve. REITs also posted negative returns as high rates continued to impact valuations. From a style perspective, growth significantly outperformed value, in spite of rising yields, given that optimism over developments in AI favored growth stocks.

Canadian equities underperformed during the quarter, relative to its global peers. The materials sector declined the most as commodity prices largely fell, while the information technology sector saw the largest gains as investors look to capitalize on the recent AI trend. In real estate, slower volumes have persisted putting the market in price discovery mode, with pricing gaps between sellers and buyers. Private buyers, specifically those less dependent on leverage, accounted for the majority of transaction volumes, followed by fund managers and REITs. Vacancy in Industrial ticked up slightly for the first time in recent periods, as record industrial completions became available; while rent growth has slowed, leasing activity still largely favors property owners.

Canadian bond prices was mixes during the quarter with performance over the past week pushing many indexes into positive territory. Bond yields increased in May and again in June. While short-term rates rose significantly, long-term rates remained relatively unchanged. Long-term bonds outperformed corporate and universe bonds during the period, while mid-term rates remained lower than both short and long-term rates. Canadian dollar appreciated against the US dollar and the Euro, dampening equity returns for Canadian unhedged investors.

“U.S. equities have rallied since the beginning of 2023 driven by information technology and consumer discretionary stocks. Market concentration is reaching all-time high levels. When a few stocks increase in value and index weight, investors can be rewarded with higher returns. Market stress or idiosyncratic events can however, cause a reversal in price, leading to greater losses. Investors should be prudent in understanding their exposure when allocating to broad market indices. It is important to remain disciplined and rebalance the indexed portion of the portfolio to policy on a regular basis.” said Venelina Arduini, Principal at Mercer Canada.

The Bank of Canada maintained its pause on interest rate hikes early in the quarter, However, in June, the Bank recognized that tighter monetary policy may be required to bring inflation closer to its target and raised interest rate by 25 basis points. The U.S. Federal Reserve, on the other hand, increased their target rate by 25 basis points in May, but announced a pause in June. This pause was due to latest release of inflation data showing meaningful declines. The Bank of England surprised investors with a 50 basis points hike (vs the expected 25 basis points) in June following stickier inflation and wage growth reported in the country.

The Mercer Pension Health Pulse

The Mercer Pension Health Pulse tracks the median ratio of solvency assets to solvency liabilities of the pension plans in the Mercer pension database, a database of the financial, demographic and other information of the pension plans of Mercer clients in Canada. The database contains information on almost 500 pension plans across Canada, in every industry, including public, private and not-for-profit sectors. The information for each pension plan in the database is updated every time a new actuarial funding valuation is performed for the plan.

The financial position of each plan is projected from its most recent valuation date, reflecting the estimated accrual of benefits by active members, estimated payments of benefits to pensioners and beneficiaries, an allowance for interest, an estimate of the impact of interest rate changes, estimates of employer and employee contributions (where applicable), and expected investment returns based on the individual plan’s target investment mix, where the target mix for each plan is assumed to be unchanged during the projection period. The investment returns used in the projections are based on index returns of the asset classes specified as (or closely matching) the target asset classes of the individual plans.

About Mercer

Mercer, a business of Marsh McLennan (NYSE: MMC), is a global leader in helping clients realize their investment objectives, shape the future of work and enhance health and retirement outcomes for their people. Marsh McLennan is a global leader in risk, strategy and people, advising clients in 130 countries across four businesses: Marsh, Guy Carpenter, Mercer and Oliver Wyman. With annual revenue of $23 billion and more than 85,000 colleagues, Marsh McLennan helps build the confidence to thrive through the power of perspective. For more information, visit mercer.com, or follow on LinkedIn and X.