Leveraging 1e pension plans to de-risk your balance sheet

26 June 2025

1e pension plans offer employees the flexibility to choose how a portion of their pension savings is invested. This self-determined investment approach allows employees to diversify their pension savings through a private wealth strategy. For sponsoring employers, 1e pension plans present an effective solution to mitigate pension balance sheet exposure in accordance with international accounting standards, such as IAS 19.

How does a 1e pension plan work?

When implementing a 1e pension plan, it must be established through a separate pension foundation distinct from the traditional base plan. However, it is possible to use the same provider for both pension plans, provided that the pension foundations remain separate.

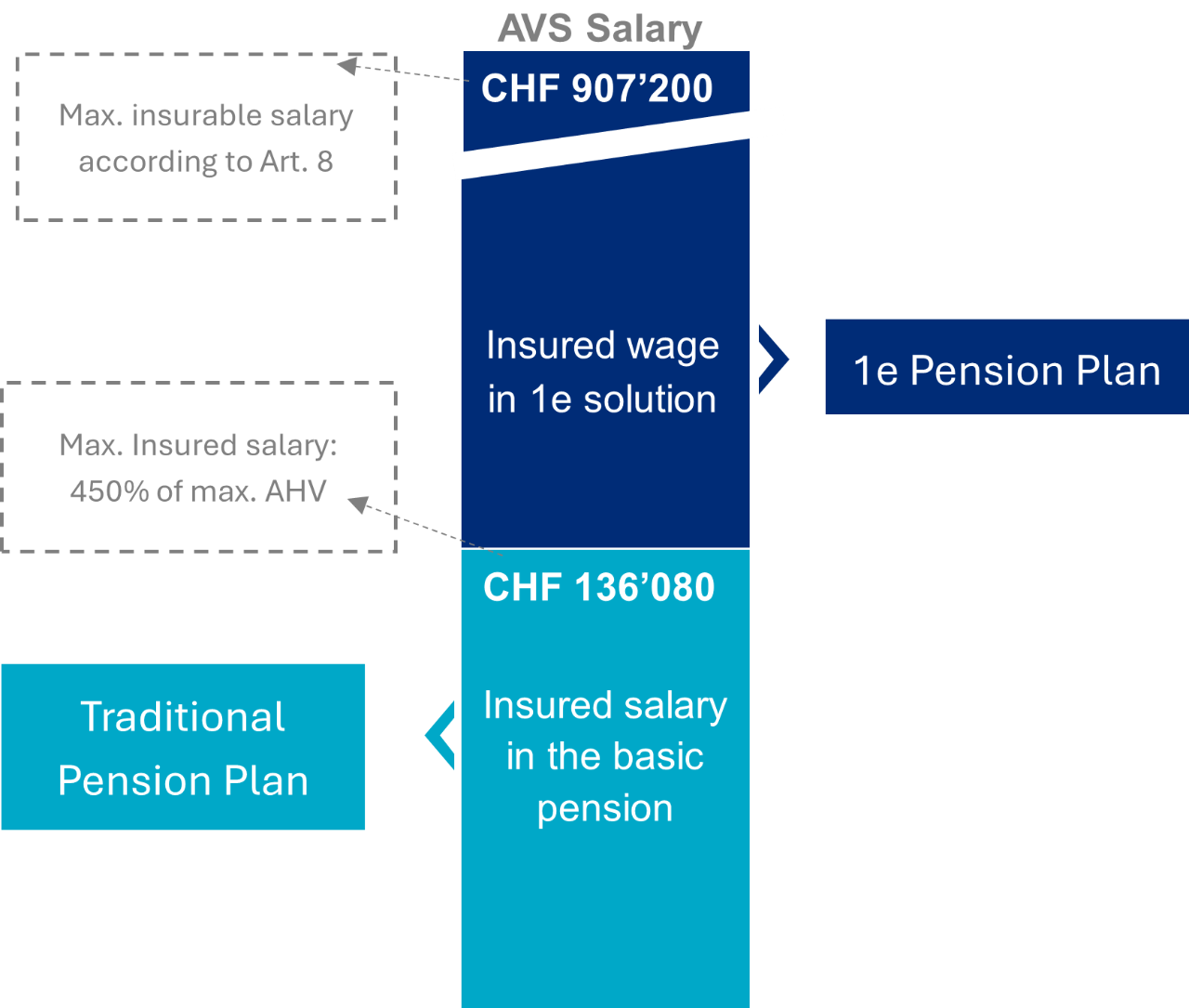

A 1e pension plan allows plan members to individually select their preferred investment strategy for their pension savings from a range of up to 10 different options. These strategies vary in their exposure to return-seeking investments, allowing members to choose a strategy that aligns with their personal risk capacity and risk appetite. Additionally, a low-risk strategy is typically available, designed to help maintain the level of retirement savings.

The asset performance generated within the chosen investment strategy is directly credited to the members’ retirement savings, usually without additional guarantees. This means that members fully benefit from potential gains but must also bear any losses from negative performance.

At retirement, a 1e pension plan generally offers, with some exceptions, only the option to withdraw a lump-sum benefit. This differs from traditional pension plans, where members can opt for a lifelong retirement pension. Furthermore, a 1e pension plan must provide insurance coverage for the risks of death and disability, similar to traditional pension plans.

What are the benefits and considerations for plan members and sponsoring employers?

Implementing a 1e pension plan offers multiple advantages for both plan members and sponsoring employers:

Benefits for plan members

- Investment choice: Plan members have the flexibility to choose how they want to invest their pension savings. A low-risk investment strategy is typically available, ensuring that members are not forced to take on investment risks.

- Direct profit credit: The entire net profit from investments is credited directly to the plan member’s pension savings, maximizing their retirement funds.

- No cross-subsidization: Redistribution of investment income or pension savings among plan members is excluded, meaning there are no cross-subsidies to other members.

- Voluntary contributions: Members can make voluntary purchases, similar to traditional pension plans, enhancing their retirement savings.

Benefits for sponsoring employer

- Favorable accounting treatment: Under international pension accounting standards such as IFRS (IAS 19) or US GAAP, 1e pension plans are typically classified as “Defined Contribution” (DC) plans rather than “Defined Benefit” (DB) plans, which are traditional Swiss pension plans with underlying guarantees. This classification can lead to a reduction in balance sheet liabilities and ongoing profit and loss costs upon implementing a 1e pension plan (DC treatment is subject to auditor approval).

- No underfunding risk: There is no risk of underfunding in a 1e pension plan, eliminating the possibility of extraordinary employer recovery contributions.

- Design flexibility: Employers enjoy a high degree of flexibility in designing the 1e pension plan, including eligibility criteria and benefit structures, which enhances the employer's attractiveness to potential employees.

- Increased employee engagement: The implementation of a 1e pension plan can lead to greater employee engagement in pension planning and retirement savings.

- Aligning with current market trends and benefits: The adoption of 1e pension plans is in line with current trends in the Swiss pension market, as more employers are rolling out these plans.

Are there any concerns surrounding 1e pension plans?

While 1e pension plans offer several advantages, they also transfer certain risks from the pension plan to the plan members, which can raise concerns for both plan members and sponsoring employers:

- Lack of guaranteed interest: Typically, pension savings in a 1e pension plan do not come with a guaranteed interest rate, meaning each plan member fully bears the risk of investment losses. It is essential to provide transparent clarification regarding the investment risks assumed by plan members.

- Potential for investment losses: Job changes during market downturns can lead to investment losses. Depending on the provider, there may be solutions available to mitigate this risk. Additionally, an amendment to Swiss pension law addressing this issue is currently pending.

- Limited retirement benefit options: Generally, retirement benefits are offered only as a lump-sum payment. While some providers may allow for the election of an annuity, this option often comes with very low conversion rates.

- Implementation challenges for employers: From the sponsoring employer's perspective, there is a significant coordination and communication effort required during the implementation phase and beyond. Engaging external expertise can facilitate this process and enhance plan members' engagement with their pension savings.

When considering the implementation of a 1e pension plan, a key success factor is to transparently assess and discuss these concerns with key stakeholders within your organization. Many organizations have already navigated this process, and at Mercer, we have the experience to guide you through it with our independent advice.