China's next economic chapter

4 mins read

At the start of July, the Chinese government marked 100 years since the founding of the Chinese Communist Party – it is now busy laying the groundwork for the next century. The economy is a key element in its program, and important shifts are planned, such as an emphasis on balanced growth—rather than growth at any costs—and ongoing liberalisation in financial markets.

Investors should take note as understanding China’s economic cycles and policies is important for driving asset allocation and portfolio construction. China’s role in the global economy is large and the economy is still experiencing rapid change, which can bring many investment opportunities. Although now the world’s second-largest economy by nominal GDP, China is still very much an emerging economy as per capita income is low by global standards at around $10,000 USD. This means it takes a large weighting in many emerging market portfolios. But even for those not invested in emerging markets, it exerts a substantial gravitational pull on the global economy. The Chinese consumer market is now the biggest in the world in certain sectors and demand is important for companies as different as Australian mining stocks, French makers of luxury goods, and Starbucks (which has more stores in China than any other country after the US).

The importance of financial stability in China’s economy

Financial stability is a focus as the Chinese economy is transitioning to the next phase of development. At the centenary celebrations in Beijing, President Xi Jinping declared the country to be a “moderately prosperous nation”, a goal met because of the tremendous growth since the start of economic liberalisation in 1978.

One of the most eye-catching of the current targets is to double per capita income by 2035 from around $10,000 USD in 2020 to $20,000. China’s per capita income level is similar to Russia but behind middle-income countries such as Chilli or Roumania. Chinese policy makers aim to achieve this by boosting productivity growth, transitioning to higher value chain activities and strengthening technological innovation.

Central economic planners have shifted to focus on growth quality over quantity. To achieve China’s longer-term economic plans, the economy must expand on a sustainable basis. This means policymakers will need to stabilise the debt ratio at current levels by ensuring credit grows no faster than nominal GDP.

Although the Chinese economy has a good medium-term record, it alternates periods of frenzied growth with intervals where the government is furiously trying to cool it down. The most recent example was the response to the global financial crisis, when Beijing unleashed significant fiscal stimulus. Subsequent excess capacity and internal imbalances, including rapid debt accumulation, meant the brakes were slammed on, resulting in slower economic growth between 2013-2016.

Only recently, through deleveraging, industry consolidation and rationalisation, has the economy been able to return to its stable growth trend. Beijing appears to have taken the lessons of 2008 and 2009 to heart – as an example look at the response to the pandemic. During the depths of the crisis, Chinese policymakers exercised restraint and avoided large fiscal stimulus. Monetary policy was eased only temporarily, and, by the end of 2020, interest rates were back up to pre-crisis levels. Beijing's policy response was the complete opposite to US and other developed economies where governments slashed interest rates and spent billions to sustain demand.

Chart 1: China 1yr Government Bond Yield

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

Safeguarding financial stability also involves stabilising risks across the economy. Since the beginning of 2016, the government has gradually moved away from an ‘implicit guarantee’ framework for financial markets, moving towards risk-based pricing. This policy seeks to open up sources of financing across the economy and improve the efficiency of debt and capital markets at allocating capital. Such measures provide several advantages including reducing reliance on the banking sector, to encourage international fund flows into China’s financial markets and to enhance financial intermediation.

A key issue for the Chinese economy: deleveraging

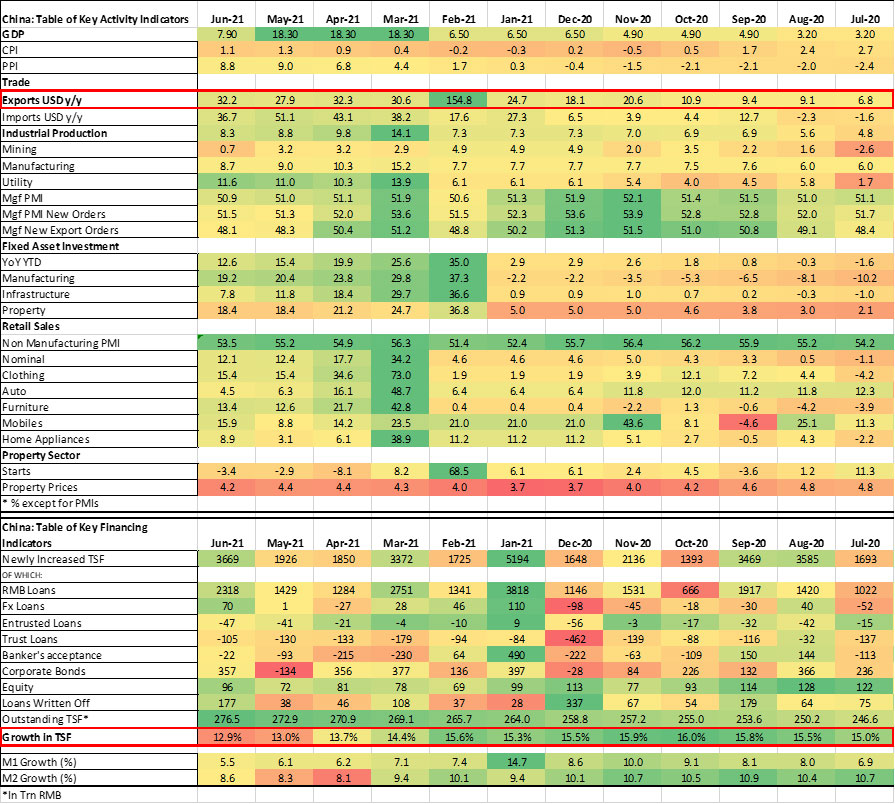

The mindset of Chinese policymakers on deleveraging has been countercyclical; they look to tighten credit during periods of strong growth and favourable external conditions and to ease when growth is soft. Looking at our scorecard for the Chinese economy, growth has been exceptionally strong over the past nine months:

Table 1

Chinese authorities brought the pandemic under control by the end of the second quarter in 2020, and it was the only G20 country to see its economy expand in 2020. Official statistics put GDP growth at 2.3%. Over the first half of 2021, production and consumption sectors continued expanding and domestic tourism around the May 1 annual holiday exceeded pre-pandemic levels.

External economic conditions are very positive, too, driven largely by the ongoing economic reopening across the world and accommodative US fiscal policy. This has created an environment of rising consumption and demand for goods, which has benefited Chinese exports. Exports have expanded for the last 12 consecutive months (See Table 1). China’s real economic growth for 2021 is expected to reach around 8.5% based on consensus forecasts.

Based on these favourable growth conditions, policymakers in China have tightened credit extensively this year. As a result, China’s overall pace of credit growth has continued to decline sharply over the past eight months with total social financing (a broad indicator of credit) down from 16.0% to 13.0% (Table 1). The M1 and M2 (chart 1) money supply indicators (measuring the cash most readily available in wallets, deposits and savings accounts) have also fallen from their peak in 2020 and China’s “credit impulse” (which measures the growth in new financing as a share of GDP) has declined as well (chart 2).

Chart 1: China M1 and M2 Growth

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

Chart 2: China Credit Impulse

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

Source Bloomberg. Bloomberg L.P.: ©2021 Bloomberg L.P. all rights reserved. Bloomberg, Bloomberg professional, Bloomberg financial markets, Bloomberg news, Bloomberg trademark, Bloomberg bondtrader, and Bloomberg television are trademarks and service marks of Bloomberg L.P. a Delaware limited partnership.

As already noted, stabilising the debt ratio means credit growth should not exceed nominal GDP growth, and this is close to being achieved. China’s nominal GDP growth, which does not adjust for inflation, is expected to reach around 12% in 2021 based on guidelines set in the National People’s Congress in March 2021. With total credit growth in China at around 13%, policymakers should be close to realising their objective by around September this year. More recently Chinese authorities have cut the Reserve Requirement Ratio by 50 basis points, which is a sign of more relaxed policy settings. This is likely to support a rebound in credit from the start of the fourth quarter, which is seasonally a stronger period for credit expansion in China in the lead up to the Lunar New Year in 2022, traditionally a time for solid consumer spending.

Easing across credit policy will be favourable for economic growth, and this is likely to come when the external outlook dims a little. Growth momentum in the US, easily China’s largest export market, has already peaked, and higher inflation there will likely result in some marginal tightening from the US Federal Reserve. I expect Chinese policymakers will be ready to recalibrate policy as necessary and will be in a stronger position to ease off the brakes with the growth in debt stabilised.

In conclusion

While China’s leadership celebrated on July 1, their economic policymakers should also have permitted themselves their own specific party. A disciplined and counter-cyclical framework for credit control has supported the economy during the depths of the pandemic without putting too much pressure on financial stability. Admittedly, the aggressive infection control in China reduced economic damage; there was no need for the extreme action seen in other countries. Nevertheless, policymakers in Beijing have room to offer mild stimulus to support medium term growth in the economy at a time when other countries may start applying the breaks.

Before accessing this website you must read and accept the following terms and legal notices.

You are about to enter a website intended for sophisticated, institutional investors based in Europe. The information contained herein is intended only for investors who are Professional investors or Eligible Counterparties as defined in Markets in Financial Instruments Regulations 2017 (the “MiFID II Regulations”). Any person unable to accept these terms and conditions should not proceed any further.

In Europe, Mercers Outsourced Chief Investment Officer, Delegated Solutions and other Investment Services delivered through Mercer Funds are delivered by Mercer Global Investments Europe Limited (“MGIE”). Mercer Global Investments Europe Limited, trading as Mercer, is regulated by the Central Bank of Ireland. Registered Office: Charlotte House, Charlemont Street, Dublin 2, Ireland. Registered in Ireland No. 416688.

Information about Mercer strategies and solutions is provided for informational purposes only and does not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities, or an offer, invitation or solicitation of any specific products or the investment management services of Mercer, or an offer or invitation to enter into any portfolio management mandate with Mercer. None of the content on Mercer.Com should be considered as advice. No actions should be taken based on this content without first obtaining professional advice. Mercer makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss. Past performance does not guarantee future results. The value of investments can go down as well as up, so you could get back less than you invest.

Mercer reserves the right to suspend or withdraw access to any page(s) included on this Website without notice at any time and accepts no liability if, for any reason, these pages are unavailable at any time or for any period. The solutions, products and services described in these pages are not available in all jurisdictions.