SECURE 2.0 brings more changes to required minimum distribution rules

Required minimum distribution (RMD) changes made by the SECURE 2.0 Act (Div. T. of Pub. L. No. 117-328) come before IRS had a chance to finalize regulations for earlier RMD revisions made by the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE 1.0) (Div. O. of Pub. L. No. 116-94). Though not as far-reaching as the SECURE 1.0 changes, SECURE 2.0 increases — again — the age at which RMDs must begin. The new law also contains several provisions allowing defined contribution (DC) plan participants to take some or all of their account balance as an annuity and makes a few other minor changes.

Increase in age for RMDs — again

Under Internal Revenue Code (IRC) Section 401(a)(9), participants in employer-sponsored DC and defined benefit (DB) plans — including all qualified, 403(b) and governmental 457(b) plans — must begin receiving RMDs on the pretax portion of their account by the required beginning date (RBD). SECURE 2.0’s increase in the RBD triggering age (from 72 to 73 in 2023 and then 75 in 2033) is the latest in a series of changes since Section 401(a)(9) took effect in 1984.

Plan vs. statutory RBD. The RBD is the latest date to which a plan can let a participant defer starting distributions. But retirement plans may also force payments to start earlier at any time on or after the participant reaches normal retirement age (usually age 65). A plan with an earlier starting date may refer to that date as the RBD. However, for purposes of this article, RBD refers only to the statutory date, not any earlier date used by the plan.

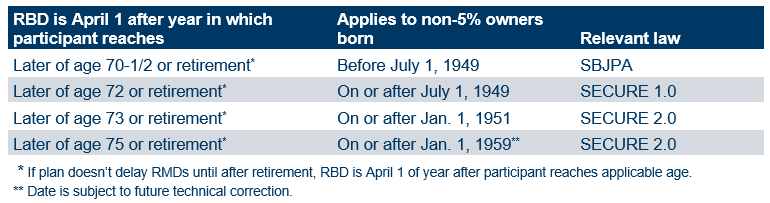

Statutory changes in RBD. Prior to the SECURE 1.0 Act, age 70-1/2 had been the triggering age for RMDs since Section 401(a)(9) first took effect. The Small Business Job Protection Act (SBJPA) of 1996 allowed — but didn’t require — plans to delay the start of RMDs until April 1 after the year in which a participant retires, and SECURE 1.0 and 2.0 retain this flexibility. Whichever date a plan uses — with or without the delay until after retirement — is a participant’s statutory RBD. (Special rules apply to 5% owners, as explained below.) The following table shows how the RBD has risen since the SBJPA.

Drafting error for participants born in 1959. Unfortunately, the new provision contains an apparent drafting error: Starting in 2023, the RMD triggering age is 73 for participants who turn 73 before Jan. 1, 2033, and age 75 for participants who turn 74 after Dec. 31, 2032. A participant born in 1959 will turn 73 in 2032 (i.e., before Jan. 1, 2033, with an RBD of 73) and will turn 74 in 2033 (i.e., after Dec. 31, 2032, with an RBD of 75). The Senate Finance Committee’s summary of SECURE 2.0 implies that these participants should have a triggering age of 75, but a technical correction would provide clarity.

Special rules for 5% owners. SBJPA extended the RMD trigger from age 70-1/2 to the later of 70-1/2 or retirement, but this change didn’t apply to employees who were 5% owners. Their RBD remained April 1 after the year they turned 70-1/2, even if still employed. The SECURE 1.0 and 2.0 increases to the triggering age apply to 5% owners, but their payments still must start even if they continue working. The remainder of this article assumes that participants are not 5% owners.

Is the new RBD mandatory or optional?

As happened with SECURE 1.0’s increase to the RBD, some employers might want to force participants to start taking benefits earlier than when SECURE 2.0 requires. For instance, after SECURE 1.0, some employers with DB plans providing very generous actuarial increases (which must start at age 70-1/2, regardless of the RBD — see next section) kept 70-1/2 as the triggering age under their plans for all participants. These employers may want to continue that approach, which is permissible under SECURE 2.0. However, payments before a participant’s statutory RBD under SECURE 1.0 or 2.0 (as applicable) likely aren’t RMDs for purposes of IRC Section 401(a)(9).

DB actuarial increases still start at 70-1/2

Section 401(a)(9)(C)(iii) requires an actuarial adjustment to DB plan benefits paid when a participant retires in a calendar year after reaching age 70-1/2. As revised by SECURE 1.0, however, the statute suggests that participants retiring between age 70-1/2 and their RBD won’t get an actuarial increase, although this apparently isn’t the result Congress intended. SECURE 2.0 doesn’t address this seeming oversight in its RMD provisions or through a technical correction. However, last year’s proposed IRS regulations clarify that participants retiring after 70-1/2 must get actuarial increases from April 1 after the year they turn 70-1/2.

Provisions encouraging lifetime income in DC plans

SECURE 2.0 makes several additional changes to the RMD requirements to promote lifetime income options for DC plan participants, who otherwise may have little protection against longevity risk (i.e., the risk that they will outlive their savings).

Commercial annuities

DC plans now have greater flexibility to offer participants commercial annuities with certain protections otherwise prohibited by current regulations. Under Treasury Regulation Section 1.401(a)(9)-6, annuities purchased using retirement plan assets generally can’t increase except in a few specified ways. The regulations provides additional exceptions for commercial annuities to provide limited inflationary gain adjustments, dividends arising from actuarial gains or accelerated payments after the employee’s death, but only if the payments satisfy a strict actuarial test. In practice, this test has prevented plans from offering commercial annuities with some protective features, such as a return-of-premium death benefit. In turn, the lack of these protections has made many DC participants reluctant to purchase a commercial annuity, potentially subjecting them to significant longevity risk.

To counter these effects and encourage individuals to purchase annuities, SECURE 2.0 makes a statutory exception for commercial annuities with several attractive features that might otherwise be restricted by the actuarial test. Examples include guaranteed annual increases of up to 5%, lump sums that shorten the payment period or accelerate the receipt of up to a year’s worth of payments, or a return-of-premium death benefit. This provision took effect immediately upon SECURE 2.0’s enactment on Dec. 29, 2022.

Qualified longevity annuity contracts (QLACs)

QLACs let employees use a portion of their retirement savings to purchase an annuity starting as late as age 85 without violating the RMD rules. The contract is exempt from RMDs until payments begin, so a participant can defer taxes on the QLAC premium while gaining some longevity insurance.

However, the 401(a)(9) regulations contain several restrictions widely perceived as reducing the usefulness of these contracts. To make QLACs more attractive, SECURE 2.0 directs Treasury to make the following regulatory changes:

- Premiums. The dollar limit on QLAC premiums is raised from $125,000 to $200,000 (annually indexed), and purchases are no longer limited to 25% of the account balance.

- Joint-and-survivor benefits after divorce. Former spouses can receive survivor benefits under a previously purchased QLAC pursuant to a qualified domestic relations order (QDRO) or similar divorce or separation instrument.

- “Free look” periods. QLACs may include provisions that give individuals up to 90 days to rescind the purchase.

The increased premium limit took effect for contracts purchased on or after Dec. 29, 2022, while the joint-and-survivor and free-look provisions apply retroactively to contracts purchased on or after July 2, 2014. Taxpayers may rely on a reasonable good-faith interpretation of the law before Treasury amends its regulations.

Partial annuitization

DC plan participants can now credit annuity payments against their annual RMD from their plan accounts. Previously, when a participant purchased an annuity (not a QLAC) with a portion of a DC plan account, the annuity and the remaining account were subject to RMDs determined separately. If the annual annuity payment exceeded the RMD that would have applied had the premium remained in the plan, the total payments (i.e., the annuity plus the RMD from the plan) exceeded the RMD that would have been due if the participant hadn’t purchased an annuity. Under SECURE 2.0, a participant in this situation can elect to apply the excess annuity payments toward the plan RMD due on the remaining account balance, so the total distribution is the same regardless of whether the participant took an annuity.

The changes took effect immediately on SECURE 2.0’s enactment, but Treasury must amend its regulations for this change. In the meantime, individuals may rely on a reasonable good-faith interpretation of the law.

Other changes

The law makes three other minor changes to the RMD rules.

Surviving spouse election to be treated like employee

Surviving spouses may elect to be treated like the employee for determining when RMDs must begin from a DC plan. (Previously, this treatment was automatic.) Spouses making this election will also have their distributions determined using the longer distribution periods in the Uniform Life Table rather than the Single Life Table that would have otherwise applied. (A longer distribution period leads to smaller RMDs.) This aligns the rules for DC plans and IRAs. This change takes effect in 2024. However, the statute is not entirely clear on whether plans must offer this election to spouses.

No RMDs for DC Roth accounts before employee’s death

Participants no longer have to take RMDs from their DC plan Roth accounts before death. This treatment aligns in-plan Roth accounts with Roth IRAs. The change applies to taxable years beginning after 2023, but plans must still pay RMDs relating to earlier tax years (e.g., 2023 RMDs due April 1, 2024).

Reduction in excise tax for late RMDs

Individuals who fail to take RMDs from their retirement plans (DB and DC) are subject to an excise tax on the missed amounts. SECURE 2.0 reduces this tax from 50% to 25% for taxable years starting after Dec. 29, 2022. The tax is further reduced to 10% if the distribution and the associated tax are paid within a correction window as specified in the statute. Individuals may file for an abatement of the tax, while plan sponsors correcting the error though IRS’s Voluntary Correction Program may request a waiver of the tax on the participant’s behalf.

Plan amendments

Many plans will need an amendment to reflect the RBD changes, regardless of whether the plan maintains or changes its existing payment provisions (depending on plan terms). Plans may also need amendments for the surviving spouse and predeath RMD provisions. The plan amendment deadline for all SECURE 2.0 changes is the end of the first plan year beginning on or after Jan. 1, 2025 (2027 for governmental and collectively bargained plans). This deadline applies to sponsors implementing any of the act’s changes before the amendment deadline. For sponsors that first implement any optional changes after the amendment deadline, the usual discretionary timing rule will apply (i.e., amendments will be due by the end of the plan year in which the sponsor makes the change).

Anti-cutback relief. The anti-cutback rules of Code Section 411(d)(6) ordinarily prohibit plans from taking away an existing distribution option — including payments at a given RBD. However, SECURE 2.0 provides broad relief for the changes as long as plans are timely amended and operated according to the new requirements in the meantime. For example, plans that adopt the new RBD ages under SECURE 2.0 won’t be treated as eliminating a distribution option at age 72. The relief applies to any plan amendment reflecting the statute’s changes for employer-sponsored plans, including required amendments and discretionary amendments adopting the law’s optional provisions.

Related resources

Non-Mercer resources

- Div. T of Pub. L. No. 117-328, the SECURE 2.0 Act (Congress, Dec. 29, 2022)

- Summary of SECURE 2.0 Act (Senate Finance Committee, Dec. 19, 2022)

Mercer Law & Policy resources

- User’s guide to SECURE 2.0 (Jan. 18, 2023)