Mental health parity compliance gets a boost in 2021 spending act

The Consolidated Appropriations Act, 2021 (CAA) (Pub. L. No. 116-260) requires group health plans and issuers that cover mental health/substance use disorder (MH/SUD) and medical/surgical (M/S) benefits to prepare a comparative analysis of any nonquantitative treatment limits (NQTLs) that apply. Beginning Feb. 10, plans must supply this analysis and other information if requested by federal regulators (the Department of Labor (DOL) for ERISA plans). This GRIST describes these new requirements, the process agencies must follow when requesting these disclosures and the impact on existing parity regulations. The new law also requires agencies to prepare an annual report to Congress on these requests and to issue compliance program and additional NQTL guidance. FAQs issued April 2 (FAQs Part 45) provides more details on agency expectations for health plan compliance.

What’s new for parity compliance?

In recent years, federal agencies have released several sets of FAQs, a disclosure request template and other compliance materials on NQTLs under the Mental Health Parity and Addiction Equity Act (MHPAEA). Many of these initiatives come in response to the 2016 passage of the 21st Century Cures Act (Pub. L. No. 114-255), which requires federal agencies to issue MHPAEA guidance and step up parity enforcement for NQTLs.

NQTLs consist of any limitations on the scope and duration of benefits that are not expressed numerically. Examples of NQTLs include medical-management standards that limit or exclude coverage based on medical necessity, prior-authorization requirements, and methods used to determine provider reimbursement rates. Under final regulations issued in 2013, the “processes, strategies, evidentiary standards and other factors” used to define plan terms and administer NQTLs for MH/SUD benefits must be comparable to and applied no more stringently than the ones used for M/S benefits.

According to DOL, the MHPAEA and ERISA’s disclosure and claims rules entitle health plan participants to request information about these “processes, strategies, evidentiary standards and other factors” used to apply an NQTL to MH/SUD and medical/surgical benefits. Participants can also request information about the plan’s medical-necessity criteria for both MH/SUD and M/S benefits.

The 2021 CAA adds two new requirements to health plans’ existing MHPAEA obligations: a comparative analysis and the duty to disclosure this analysis and related information to DOL on request.

Comparative analysis

The CAA amends ERISA to require that plans “perform and document comparative analysis of the design and application of NQTLs.” The law does not define the comparative analysis or explain how to document it. However, DOL, the Centers for Medicare & Medicaid Services (CMS), some states and other organizations have discussed and, in some instances, produced templates to complete side-by-side comparisons documenting that the processes, strategies, evidentiary standards and other factors used for NQTLs in six separate classifications meet parity standards. FAQs Part 45 provide more information on what plans should include in their comparative analysis, including the types of documents plans should make available to support the analysis.

Disclosure of comparative analysis and related information to DOL

ERISA plans must be prepared to disclose the new comparative analysis on request from DOL starting Feb. 10, 2021 — 45 days after the CAA’s enactment. DOL must request this information from at least 20 different plans per year. The agency can determine appropriate circumstances for making a request, but must do so when it learns of a potential parity violation or receives a complaint alleging a violation. If DOL concludes that a plan’s comparative analysis does not have enough detail to review, the agency must specify what additional information the plan should submit. While the risk of a DOL request for this information on or shortly after Feb. 10 is low, plans still need to prepare for these requests.

The CAA added identical provisions to the Public Health Service Act (PHSA) and the Internal Revenue Code. This means CMS must annually request at least 20 different comparative analyses as part of its parity enforcement for self-insured state and local governmental plans and any state insurance programs for which CMS enforces parity. It is not clear whether IRS must also make these disclosure requests since it shares jurisdiction with DOL on MHPAEA enforcement.

What parity information must plans provide on request?

The CAA’s list of specific information that health plans must disclose on request largely overlaps with information in DOL’s self-compliance tool for evaluating whether NQTLs comply with the parity law. DOL updated the tool in 2020 after gathering public comments on its content.

CAA parity disclosure

Under the new law, plans must make available to the DOL the following information:

- Terms — the specific plan and coverage terms on NQTLs for MH/SUD and M/S benefits and a description of these benefits, including which of the six parity classifications contains the benefit (i.e. inpatient in network, outpatient in network, pharmacy, etc.)

- Factors — the factors used to determine that the NQTLs should apply to the benefits

- Evidentiary standards — the evidentiary standards and any other sources on which the plan relied to back up the factors used to design the NQTL and justify its application to a benefit (see chart below for examples)

- Comparative analysis — a separate analysis of each NQTL for benefits in each classification “demonstrating that the processes, strategies, evidentiary standards and other factors used to apply the NQTLs” to MH/SUD benefits (in written terms and plan operations) are “comparable to and applied no more stringently” than those used to apply NQTLs to M/S benefits

- Findings and conclusions — the results of the comparative analysis giving the plan’s or issuer’s specific findings on what is and is not in compliance with the parity law

FAQs Part 45 state that the comparative analysis must contain a “detailed, written, and reasoned” explanation of the basis for a plan’s conclusion that NQTLs comply with the parity law. Conclusory or generalized statements about compliance without detailed supporting explanations and evidence is not sufficient. The analysis must include at least nine elements listed in the guidance:

- A description of the specific NQTL, plan terms and relevant policies

- Identification of the MH/SUD and medical/surgical benefit to which the NQTL applies within the benefit classification, noting which benefits are treated as MH/SUD and which ones are M/S

- For both MH/SUD and M/S NQTLs, the factors, evidentiary standards, or sources or strategies used in designing and applying the NQTL, including what factors carried more weight in the evaluation and why

- Any definitions that the plan uses to define factors or standards in a quantitative manner

- Any variations in how a guideline or standard applies to MH/SUD vs. M/S benefits, and how that variation is established

- If applying an NQTL based on specific administrative decisions, the analysis must include “the nature of the decisions, the decision maker(s), the timing of the decisions, and the qualifications of the decision maker(s)”

- If the analysis relies on any expert, an assessment of the expert’s qualifications and the extent to which the plan relied on the expert

- A “reasoned discussion” of the plan’s findings and conclusions about the comparability and stringency of the identified processes, strategies, evidentiary standards, factors and sources used to design and apply NQTLs, both as written and as applied

- The date of the analysis and the name, title, and position of all individuals participating in the analysis

The guidance also lists documents that plans might need to provide to support the comparative analysis. Examples include claim-processing policies and procedures, along with samples of covered and denied MH/SUD and M/S claims.

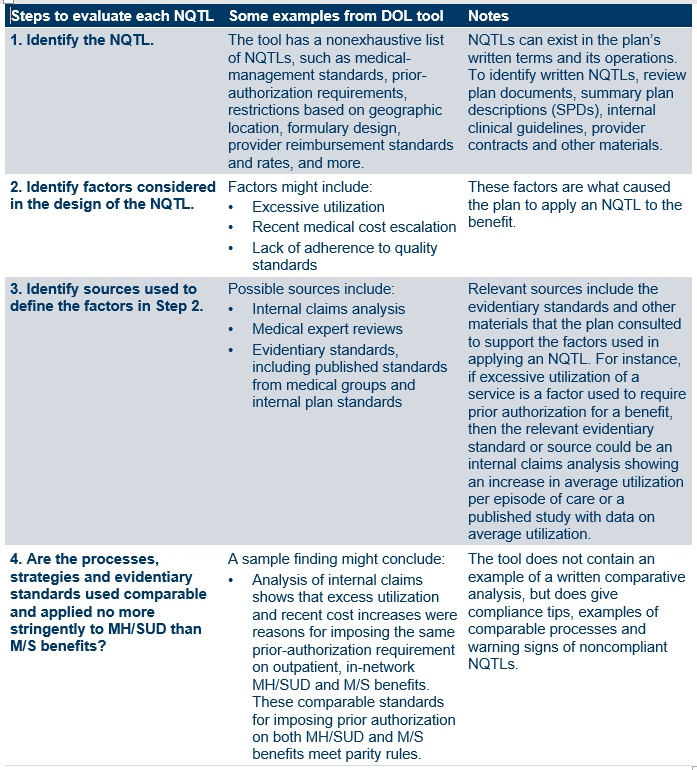

DOL self-compliance tool

Aside from information on a plan’s findings and conclusions, other elements of the CAA disclosure are almost identical to the steps listed in question 7 of DOL’s self-compliance tool. According to FAQs Part 45, plans that have already “carefully applied” the guidance in this tool are well-positioned to meet the CAA’s standards for the comparative analysis. The following chart summarizes DOL’s four-step NQTL compliance inquiry.

How does the CAA affect parity enforcement and regulation?

The CAA does not add much to DOL’s existing enforcement tools to investigate NQTL issues. The law adds no new civil penalties to ERISA, despite proposals to do so in some pending legislation. However, the required comparative analysis could provide more information to aid DOL parity investigations, which have increased in recent years. According to latest DOL enforcement fact sheet for fiscal 2020, the agency closed MHPAEA investigations of 180 health plans (the agency does not report on ongoing investigations) and noted two NQTL violations.

DOL can still require plans to correct parity violations, such as by reprocessing improperly denied claims. A federal court recently ordered that remedy in private class-action litigation that did not involve the federal government (Wit v. United Behavioral Health, No. 14-cv-02346-JCS (N.D. Cal. Nov. 3, 2020); remedies order stayed pending appeal). DOL also can refer violations to IRS, which can assess civil penalties of up to $100 a day, although whether the agency has ever done so is unclear. Other DOL penalties for failure to disclose certain information to participants or for specific fiduciary violations could also apply.

Defined corrective process. The CAA outlines a specific process to follow when DOL’s review of a plan’s comparative analysis indicates a parity violation has occurred. After DOL’s initial determination, the plan has to specify what actions it will take to correct the violation and/or provide an additional comparative analysis within 45 days. If DOL makes a final determination that the plan is still in violation, the plan must notify all enrollees about the noncompliance within seven days of DOL’s determination. The agencies will also share findings of compliance and noncompliance with the state where the group health plan is located or the issuer is licensed to do business. Documents or communications related to DOL’s recommendations to a plan will not be subject to disclosure under the Freedom of Information Act (FOIA). However, the CAA is not specific about the scope of information protected from FOIA disclosure.

New annual report naming violators. The CAA requires the agencies with MHPHEA oversight to issue an annual report to Congress and the public. The report must include, among other details, a summary of the comparative analyses reviewed during the year and the identity of each plan or issuer receiving a final determination of noncompliance. The first report is due by Dec. 27, 2021, with later reports due every Oct. 1.

Required new guidance. The Cures Act amended the PHSA to require that DOL, the Department of Health and Human Services (HHS) and the Treasury Department jointly issue a “compliance program guidance document.” This document builds on a 2016 DOL and HHS publication on warning signs that specific NQTLs could violate the law. The CAA adds this PHSA provision, along with the Cures Act’s provision calling for additional guidance, to ERISA and the Internal Revenue Code. This presumably requires DOL and IRS to participate in developing this joint guidance required by the Cures Act. Before CAA’s passage, however, DOL already noted these Cures Act obligations when it rolled out its updated self-compliance tool in last October.

- Compliance program guidance. The CAA requires the agencies to issue guidance with examples of prior findings of parity compliance and noncompliance. The guidance should include recommendations that encourage the use of internal controls to monitor compliance. (The updated DOL self-compliance tool already has a new section to encourage plans to develop formal parity compliance programs that include training, recordkeeping, detection and other strategies.) The document also must contain information about the process and timeline for participants to file complaints about parity violations and the relevant state, regional, or national office where complaints are filed. To create the new guidance, DOL and IRS must partner with the HHS Office of the Inspector General, which has developed compliance guidance for federal fraud and abuse laws that apply to certain healthcare organizations. The first guidance document is due 18 months after CAA’s enactment (June 2022) and must be updated every two years.

- Additional guidance. The CAA also requires the agencies to issue additional guidance on NQTLs, giving examples of methods for determining the “appropriate types” of NQTLs for both MH/SUD and M/S benefits. No due date is specified for this guidance, but the agencies must give the public 60 days to comment before the guidance is finalized.

Standards across the health coverage system. These new CAA requirements apply to all ERISA plans, including grandfathered plans, and to health insurers, including those in the individual, small and large group markets. The new requirements also apply to CMS-regulated self-insured state and local governmental plans that have not opted out of the mental health parity rules. Medicaid managed care plans, alternative benefit plans and certain Children’s Health Insurance Program (CHIP) plans will be deemed to satisfy the CAA requirements if the plans comply with similar Medicaid mental health parity documentation standards. Some of this documentation is already available on state Medicaid websites. MHPAEA does not apply to Medicare.

What should health plan sponsors do now?

Self-insured plan sponsors that have not yet conducted a NQTL comparative analysis will need to prepare one as soon as possible in case the agencies request this information. As some of the publicly available NQTL analysis templates demonstrate, reviewing every NQTL will take some time and involve scrutinizing clinical guidelines or provider reimbursement standards — a task typically conducted by the plan’s third-party administrator (TPA), not the plan sponsor. Employers should consider these steps:

- Contact TPAs and pharmacy benefit managers (PBMs) for the comparative analysis. State insurance laws may already require some TPAs and PBMs to prepare these analyses for insured plans. Other TPAs or PBMs may have independently done so for at least some NQTLs. Self-insured plan sponsors might ask TPAs and PBMs to conduct this analysis if they have not done so already. When negotiating contract terms with these entities or issuing requests for proposals (RFPs), sponsors should consider requiring this analysis as a prerequisite to engaging a new TPA’s or vendor’s services going forward. Even though an insured plan’s carrier is responsible for compliance, insured plan sponsors may want the carrier to confirm it has completed the analysis and will notify them if a federal or state authority finds a parity violation.

- Start comparative analysis. When vendors can’t supply the comparative analysis, sponsors might show good-faith efforts to comply by starting the comparative analysis now. Even a limited review of a handful of NQTLs triggering recent litigation may help mitigate risks until an in-depth analysis is completed. Consider a review of the NQTLs in plan documents as a starting point, and prepare a strategy and timeline for assessing NQTLs that require the involvement of the TPA or clinical experts. If DOL requests the comparative analysis before it’s complete, the employer and its legal counsel can request additional time to produce materials — a practice sometimes done for document requests during DOL audits. Plans will want to start with the four types of NQTLs noted in FAQs Part 45 as the focus of enforcement efforts:

- Prior-authorization requirements for in-network and out-of-network inpatient services

- Concurrent review for in-network and out-of-network inpatient and outpatient services

- Provider-admission standards, including reimbursement rates, for network participation

- Out-of-network reimbursement rates (described in the FAQs as the plan’s methods for determining usual, customary and reasonable charges)

- Prepare a compliance plan. Employers may want to consider a written compliance plan to “promote the prevention, detection and resolution of potential MHPAEA violations,” as recommended in DOL’s self-compliance tool. This program could include internal protocols to ensure service providers provide the documentation that the plan sponsor needs to assess parity compliance. Employers may need to take a strategic approach toward assessing compliance, since neither the CAA nor agency guidance specify the scope of the information needed for a comparative analysis.

- A compliance program could start with a review of specific areas — such as claim denials and appeals for MH/SUD treatment and prescription drugs — to identify potential issues for a deeper comparative analysis. In reviewing denied MH/SUD claims, the sponsor should determine whether an NQTL triggered the denial and, if so, whether the necessary comparative analysis has been performed and documented to demonstrate that the NQTL is permissible.

- In developing a strategy for items on which to focus, look at examples in agency guidance. For instance, FAQs Part 45 give an example of a complaint concerning prior-authorization requirements for coverage of buprenorphine to treat opioid use disorder. Plans might want to put this on the list of priority items when checking in with PBM vendors for the comparative analysis.

- FAQs Part 45 reiterate the agencies’ long-standing view that plans should be prepared to disclose the comparative analysis to participants and beneficiaries upon request. Any compliance plan should include a process for handling these requests.

- Keep up with parity and claims litigation. The biggest MHPAEA risk for large employer plans continues to be litigation, particularly challenges to NQTLs like claim-review criteria and medical-necessity standards. In the Wit case mentioned earlier, a federal court ordered a mental health service provider for insured and self-insured plans to correct ERISA violations by reprocessing more than 67,000 denied claims. The order also required the provider to use independent clinical guidelines instead of its own clinical guidelines, which the court concluded were skewed to benefit the provider's financial bottom line in violation of ERISA. The court held that the service provider violated ERISA’s claim-review and fiduciary standards by applying overly narrow guidelines when determining whether requested services, such as residential treatment, were consistent with generally accepted standards of care. Some recent cases involve not only the TPA (as in Wit), but also the employer plan (see, for example, James C. v. Anthem Blue Cross and Blue Shield, No. 2:19-cv-38 (D. Utah June 24, 2020); and Raymond M. et al v. Beacon Health Options Inc., No. 2:18-cv-048-JNP-EJF (D. Utah, May 29, 2020)).

Related resources

- FAQs about MH/SUD parity implementation and the CAA 2021, Part 45 (DOL, HHS and IRS, April 2, 2021)

- Fact sheet, FY 2020 MHPAEA enforcement (DOL, Jan. 15, 2021)

- Pub. L. No. 116-260, Consolidated Appropriations Act, 2021 (Dec. 27, 2020)

- Remedies order in Wit v. United Behavioral Health, No. 14-cv-02346-JCS (N.D. Cal. Nov. 3, 2020)

- MHPAEA self-compliance tool (DOL, Oct. 23, 2020)

- The six step parity compliance guide (American Psychiatric Association, Kennedy Forum and Parity Implementation Coalition, Sept. 12, 2017)

- Parity compliance toolkit: Applying mental health and substance use disorder parity to Medicaid and Children’s Health Insurance Programs (CMS, Jan. 17, 2017)

- Pub. L. No. 114-255, 21st Century Cures Act (Congress, Dec. 13, 2016)

- Final MHPAEA rules (Federal Register, Nov. 13, 2013)

- DOL mental health parity and substance use disorder resources

- CMS/CCIIO MHPAEA resources

- CMS Medicaid parity resources