Ireland’s automatic enrollment system progresses

The design principles for Ireland’s Automatic Enrolment (AE) Retirement Savings system, announced on 29 March 2022, confirm that Ireland would have an automatic enrolment retirement savings system implemented by Q1 2024, if the enabling legislation passes. The main elements of the Cabinet-approved final system remain broadly similar to the original ”strawman” proposals presented for public consultation in 2018 and adopted, with revisions, as Government policy in 2019. As expected, the AE system would be a “soft mandatory” system that would automatically enrol eligible employees but allow them to opt out. AE would operate alongside, and complement, the existing occupational pension scheme system, and the government estimates that approximately 750,000 employees would be eligible and automatically enrolled in the first phase.

Highlights

Enrolment. Employees aged between 23 and 60 would be automatically enrolled in the system if they earn more than €20,000 a year and do not already contribute to an occupational pension scheme. Employees would be permitted to opt out prior to automatic enrolment and at certain times after joining. Noneligible employees could choose to opt in. The Department of Social Protection is expected to make recommendations on the prescribed standards and contribution levels that would apply to occupational schemes and allow their members to be exempt from the AE system. Until guidance is provided, employers are unable to fully consider the relative advantages and/or disadvantages of the AE system as compared to existing pension arrangements.

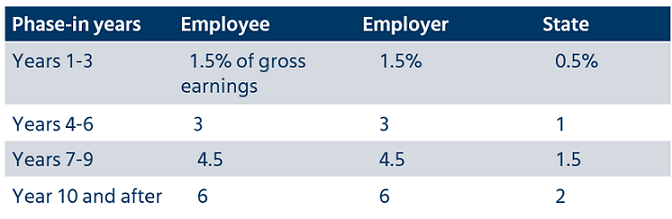

Contributions. Employers would be required to match the rate of contribution paid by employees up to a maximum earnings threshold of €80,000 per year. The Government would pay a top up based on 33% of the employee contribution. Contributions would be fixed and introduced on a phased-in basis as follows:

Tax treatment of contributions. Due to the Government’s top-up arrangement, the AE system would not be part of the current tax relief structure applicable to occupational schemes. Employee contributions would be deducted from after-tax income, and the AE system would be exempt from tax as a benefit-in-kind. Employer contributions would remain eligible for offsetting against corporation tax.

Investment funds. A choice of four investment funds would be offered: “conservative” (mainly government bonds or cash/cash equivalent); “moderate risk” (government bonds, blue-chip equities, stock exchange indices); “higher risk” (e.g. equities and property); and “default” (operating on a lifestyle basis). Employees could make fund switches at any time during the savings phase. There would be a maximum “envisaged” annual fund management charge of 0.5%.

Employment changes. Individuals would remain in the AE system when they change employment, i.e. the “pot follows the member.”

Benefit access. Employees would be able to have access to benefits only at the state pension age (currently age 66). Benefit options at retirement would be in line with the existing range of options under current revenue rules.

Central Processing Authority (CPA). A CPA would operate, coordinate, supervise and develop the AE system. The Department of Social Protection would set up the CPA, but the Pensions Authority would regulate it. The CPA would tender for four commercial investment companies to become “registered providers” (RPs). RPs would provide investment options and act as investment managers. Savers would have no direct contact with RPs — all interactions would be through the CPA. Employees would also not choose their fund providers. Contributions would be pooled by the CPA and allocated according to fund type among the RPs. Financial returns from the RPs for each fund type would also be pooled and allocated to savers’ accounts. Benefit drawdown options would be through existing commercial providers. The CPA could also tender for third party administration and accounting support.

Next steps

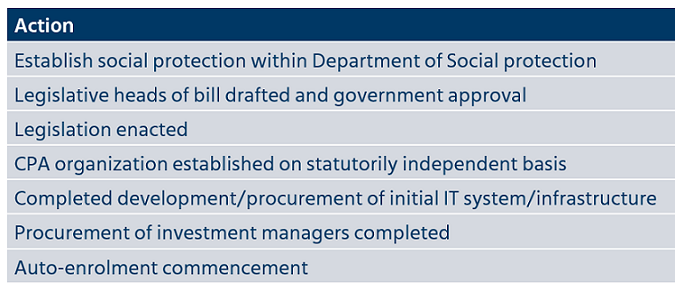

Employers should ensure that their payroll processes could support AE instructions and contribution remittance, but several details have to be finalized in upcoming legislation before the targeted first auto-enrolments in 2024. The government’s ambitious timetable is as follows:

Related resources

Non-Mercer resource

- Launch of the final design principles of automatic enrolment (AE) retirement savings for Ireland (Department of Social Protection, 29 March 2022)

Mercer Law & Policy resources

- Ireland updates auto-enrolment pension system implementation (22 November 2019)