Domestic partner benefits remain popular but present challenges

August 20, 2025

The US Supreme Court’s 2015 decision in Obergefell v. Hodges (135 S. Ct. 2071), which made same-sex marriage legal nationwide, appears to have had little effect on domestic partner benefits. Most states that had domestic partnership registries before 2015 continue to allow registrations, and surveys indicate that employers continue to offer domestic partner benefits. Despite the acceptance and prevalence of domestic partner benefits, they pose complex legal, tax, administration and other compliance issues. Employers need to understand and effectively communicate these issues to employees with domestic partners. This GRIST summarizes the major issues, provides a tax-dependent flowchart and a domestic partner checklist for employers and includes two charts summarizing applicable state laws.

Domestic partner benefit practices and issues

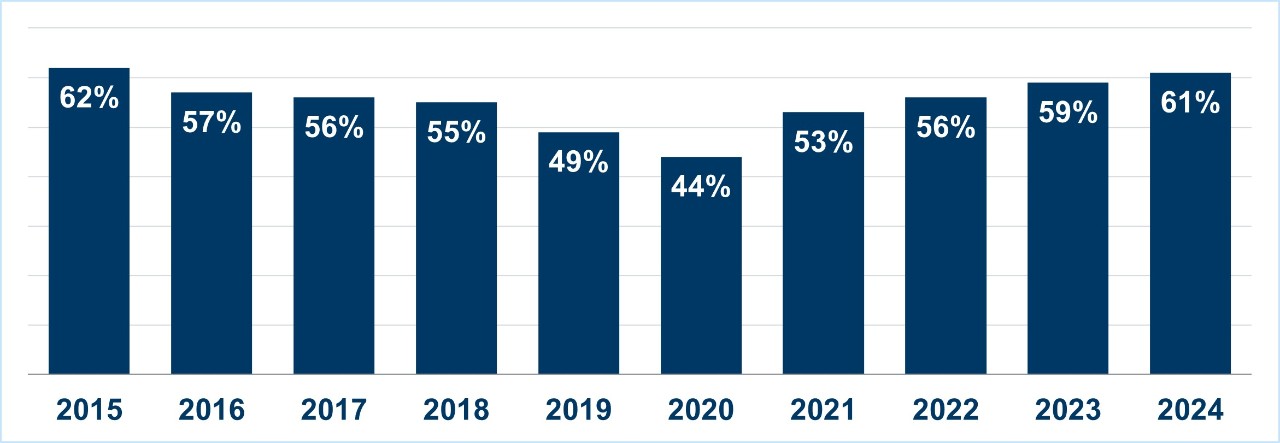

Survey. Mercer’s 2024 National Survey of Employer-Sponsored Health Plans showed that 61% of employers with 500 or more employees offer domestic partner benefits, only slightly less than in 2015:

-

Diversity, equity and inclusion (DEI)Every year, the Human Rights Campaign Foundation issues the Corporate Equality Index (CEI), a national benchmarking tool on corporate policies, practices and benefits pertinent to LGBTQ+ employees. Domestic partner coverage is one of the criteria affecting an employer’s overall CEI rating. The CEI specifically requires equivalency in same- and different-sex domestic partner medical, family formation and other benefits, including adoption assistance, fertility coverage, foster care assistance and surrogacy.

-

Key issues

Beyond those considerations, employers must communicate to eligible employees the differences between a spouse and a domestic partner under federal and state laws and apply those differences in administering benefit plan provisions. As discussed later, differences arise primarily in these areas:

- State recognition of domestic partnerships and other types of relationships, and related insurance coverage mandates for recognized relationships

- Taxation of benefits (for nontax dependents)

- HSAs and high-deductible health plans (HDHPs)

- Other federal laws, including continuation coverage under the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA), unpaid leave rights under the federal Family and Medical Leave Act (FMLA) and military leave protections under the Uniformed Services Employment and Reemployment Rights Act (USERRA)

- Government-contracting requirements mandating domestic partner coverage

- Wellness programs for spouses/domestic partners

- Documentation, such as certification of relationship or its termination or declaration of tax status

- Medicare

Related resources

Non-Mercer resources

- FAQs for registered domestic partners and individuals in civil unions (IRS)

- Form W-2 reporting of employer-sponsored health coverage (IRS)

- Publication 501, Dependents, standard deduction and filing information (IRS)

- Publication 969, HSAs, FSAs and other tax-favored health plans (IRS)

- Treas. Reg. § 1.61-21, Fair market value of fringe benefits

- How Medicare works with other insurance (Centers for Medicare and Medicaid Services (CMS))

- Medicare and you (CMS)

- Revenue Procedure 2024-40 (IRS, Oct. 22, 2024)

- State civil union and domestic partnership statutes (National Conference of State Legislatures, March 10, 2020)

- Information Letter 2016-0012 on taxation of health coverage for domestic partners (IRS, Feb. 17, 2016)

- Information Letter 2016-0008 on taxation of health coverage for domestic partners (IRS, Feb. 17, 2016)

- Private Letter Ruling (PLR) 1415011 on HRAs and nontax-dependent domestic partners (IRS, April 11, 2014)

- PLR 200339001 on taxation of medical and dental benefits for domestic partners (IRS, Sept. 26, 2003)

- PLR 200108010 on FMV calculation of domestic partner coverage (IRS, Feb. 23, 2001)

Mercer Law & Policy resources

- Roundup: State accrued paid leave mandates (updated periodically)

- State paid family and medical leave contributions and benefits (updated semiannually)

- Puerto Rico’s benefit and leave laws sometimes differ from others (Aug. 12, 2024)

- Common-law marriage raises issues for employer benefits (March 3, 2020)

About the author(s)

Related insights