COBRA subsidies in COVID-19 rescue plan require employer action

Fully subsidized COBRA coverage is one of many health policy provisions in the American Rescue Plan Act (ARPA) (Pub. L. No. 117-2) enacted March 11. The federal government will subsidize 100% of COBRA premiums for qualified beneficiaries who otherwise would lose employer health coverage due to involuntary termination or reduced work hours. Applicable to employees’ and family members’ premiums, the subsidy will last from April 1 to the earlier of Sept. 30 or the expiration of an individual’s COBRA coverage period. The subsidy is not available to individuals eligible for other group health plan coverage or Medicare. The departments of Labor (DOL), Treasury and Health and Human Services (HHS) will administer the subsidy program and should soon issue guidance, model notices, and tax forms and instructions. Once guidance is issued, employers will need to take immediate action to provide new COBRA notices and a special election period. The law directs the agencies to conduct public outreach to inform employers, group health plan administrators, insurers, public assistance programs, states and other entities about the subsidies.

Subsidy overview

The temporary subsidy is intended to help people afford the cost of maintaining health coverage under federal and state coverage-continuation laws. (For simplicity, this GRIST refers to all of these laws as COBRA, which is short for the federal mandate enacted by Consolidated Omnibus Budget Reconciliation Act of 1985.) The subsidy is equal to 100% of the cost of COBRA coverage (including the 2% administration fee) for qualified beneficiaries who will lose or have already lost employer-provided coverage due to involuntary separation from employment or reduced work hours. The subsidy is only available from April through September 2021.

Federal COBRA basics. Under the federal COBRA law, a private employer with 20 or more employees that sponsors a group health plan must let individuals elect to continue their health coverage when it would otherwise end for certain reasons (such as job loss, divorce or the employee’s death). Qualified beneficiaries with COBRA rights include employees, spouses and dependents who would lose coverage because of the event. Employers can charge individuals electing COBRA the full cost of coverage, plus an additional 2% to cover administrative costs. Individuals who lose employer coverage because of job loss (voluntary or involuntary) or a reduced work schedule can elect to continue COBRA coverage for up to 18 months (36 months for other qualifying events). Employers and qualified beneficiaries must meet notice and other obligations under COBRA.

State continuation basics. Employers with fewer than 20 employees don’t have to provide federal COBRA coverage. However, many states have enacted “mini-COBRA” laws that require small employers sponsoring fully insured group health plans to offer continuation coverage. According to a Kaiser Health News report, all but six states have a mini-COBRA law, and at least one without – Montana – is considering adopting one.

Déjà vu? The new COBRA subsidy is similar to the one enacted by the American Recovery and Reinvestment Act of 2009 (ARRA). That subsidy covered only 65% of the cost of COBRA coverage but lasted a longer time. Until agencies issue guidance on the ARPA COBRA subsidy, the ARRA guidance (for example, IRS Notice 2009-27) may provide insight into how the program might work. However, the variety of agency relief already provided in response to the COVID-19 pandemic and the social and economic challenges unique to the pandemic might alter some of the past guidance.

Covered plans

The subsidy is available for continuation coverage under health, dental, vision and other group health plans (like health reimbursement arrangements) but not for continuation of health flexible spending arrangements (FSAs). Coverage for COBRA qualified employees (or ex-employees), spouses and dependents is eligible for the subsidy.

Most employer health plans are subject to federal COBRA through the Internal Revenue Code, ERISA or both. COBRA applies to state and local government employer plans through the Public Health Services Act. Church plans (fully insured and self-funded) are not subject to federal COBRA due to a narrow exception in the law, but fully insured church plans may be subject to state continuation laws. Determining whether a plan is a church plan can be difficult and requires a detailed analysis of the organization’s activities and the closeness of the religious affiliation.

Subsidy-eligible COBRA qualified beneficiaries

The subsidy is available for COBRA coverage from April 1 to Sept. 30 for individuals who would otherwise lose employer group health plan coverage due to involuntary job loss or reduced work hours. To receive the subsidy, individuals must be in their initial 18-month COBRA coverage period (i.e., the loss of employer coverage resulting from a COBRA-qualifying event must have occurred after Oct. 1, 2019). Individuals cannot receive the subsidy if they are eligible for other group health coverage or Medicare. Some of these so-called assistance-eligible individuals (AEIs) must be offered a second opportunity to elect COBRA coverage (see “Second election period” below).

Involuntary job loss or reduction in hours

The subsidy is available for COBRA coverage elected after involuntary job loss or reduced work hours. The law does not define “involuntary” but specifically excludes individuals terminated for gross misconduct. Guidance on the previous COBRA subsidy program noted that each termination’s facts and circumstances determine whether it is involuntary and provided a series of examples. Whether the agencies modify that earlier guidance for particulars related to the COVID-19 pandemic remains to be seen. For example, will “involuntary” include pandemic-related reasons outside the employee’s control, such as the need to stay home to care for a minor child whose school or place of care has closed?

The law does not appear to require a reduction in work hours triggering loss of coverage to be involuntary for an individual to qualify for the COBRA subsidy. Confirmation from the agencies would be welcome.

Not eligible for other group coverage or Medicare

Existing rules allow early termination of COBRA coverage if an individual is covered by — not merely eligible for —another group health plan or Medicare. In contrast, mere eligibility for another group health plan or Medicare eliminates eligibility for the subsidy. After the subsidy period begins, the disqualification occurs for the months of COBRA coverage beginning on or after the date the individual first becomes eligible for the other coverage.

Other group health coverage. Eligibility for other group health plan coverage — such as a plan sponsored by a new employer or the employer of a spouse, parent, or domestic partner — terminates eligibility for the COBRA subsidy. For this purpose, group health plan coverage does not include an excepted-benefit plan, a health FSA or a qualified small employer health reimbursement arrangement (QSEHRA). But exactly how this limitation applies to subsidy eligibility for excepted benefits is unclear.

Example. Laura is an AEI enrolled in subsidized COBRA major medical coverage. Laura’s spouse starts a new job and can enroll herself and Laura in the employer’s group medical plan with coverage effective May 1. Laura loses subsidy eligibility as of May 1, even if Laura’s spouse doesn’t enroll Laura in the plan. If Laura’s spouse can enroll family members in only the employer’s excepted benefits like vision or dental coverage, Laura will not lose her subsidy eligibility.

Example. Liam is an AEI enrolled in subsidized COBRA dental coverage. Liam’s spouse starts a new job and can enroll herself and Liam in the employer’s group dental plan with coverage effective May 1. Does Liam lose subsidy eligibility as of May 1? Guidance on this type of issue is needed.

Medicare coverage. Eligibility for the subsidy ends when an individual with COBRA coverage becomes eligible for Medicare. This generally happens when an individual turns 65, receives a disability determination from the Social Security Administration or is diagnosed with end-stage renal disease.

Notice requirement. Subsidy-eligible individuals must notify the plan if they become eligible for other group health plan or Medicare coverage. The DOL will establish the timing and form of this notice. Failure to provide the notice could result in an IRS penalty of $250 for each failure. If the failure is “fraudulent,” the penalty can equal 110% of the subsidy received after eligibility ended. Though not defined in the law, fraudulent likely means an intentional failure to provide the required notice; confirmation from the agencies would be helpful. Penalties won’t apply if the failure had a reasonable cause and was not due to willful neglect.

Subsidy period

The COBRA premium subsidy is available only from April through September and will end earlier if an AEI becomes eligible for other group health coverage or Medicare (as discussed above). Eligibility (or loss of eligibility) for the COBRA subsidy affects only the cost — not the duration — of an individual’s COBRA continuation coverage. Receipt of the subsidy doesn’t affect whether or how long someone is eligible to continue COBRA coverage:

- If an individual’s COBRA coverage period ends before Sept. 30, the subsidy ends as well.

- If an individual’s COBRA coverage period ends before April 1, that person is not eligible for extended coverage or the subsidy.

- If an individual’s COBRA coverage period continues past September, the individual will have to pay the COBRA premium to maintain the coverage.

Here are some examples:

- Alice was laid off and lost her group health plan coverage on Nov. 1, 2020. Alice elected COBRA coverage and has been paying the required monthly premium. Alice can continue this coverage for 18 months, but she will receive the COBRA subsidy only from April through September 2021. After September, Alice will be responsible for paying COBRA premiums if she wants to continue coverage.

- Adam was laid off and lost his group coverage on Jan. 1, 2020. Adam elected COBRA coverage and has been paying his monthly premiums. Adam does not have to pay COBRA premiums for his final three months of COBRA coverage — April, May and June 2021.

- Aaron was laid off and lost his group health plan coverage before Oct. 1, 2019. Aaron elected and continued COBRA coverage for 18 months through March 2021, but he was responsible for paying the premiums (barring application of the outbreak period relief). Aaron is not eligible for any COBRA subsidies because his coverage period ended before April 1, 2021.

Less expensive coverage option

COBRA coverage typically is the same coverage an individual had immediately before the qualifying event. Under ARPA, employers may (but are not required to) allow AEIs to choose a different plan that costs the same as or less than the coverage held at the time of the qualifying event. However, AEIs cannot elect, as an alternative to major medical coverage, a plan that provides only excepted benefits, such as a stand-alone dental or vision plan, an employee assistance program (EAP), a health FSA, an on-site health clinic or a QSEHRA. In addition, the alternative plan has to be available to the employer’s active employees.

Since AEIs pay no premiums during the subsidy period, they won’t see any savings from switching to lower-cost coverage, unless COBRA coverage continues after the subsidy period ends. In fact, AEIs might see out-of-pocket costs increase (and maybe even reset) when switching to a lower-cost plan. Nevertheless, employers can choose to offer the option to switch, and AEIs have 90 days after getting a notice of this option to make the switch.

Application to other COBRA coverage unclear. The subsidy is available for all group health plan coverage that is subject to COBRA (except health FSAs), including excepted benefits like dental, vision and some EAPs. However, the law is not clear on whether the option to switch to less expensive coverage applies to these excepted benefits that are not major medical plans. For example, can an AEI choose a less expensive dental or vision plan for the subsidy period? Clarification from the agencies would be helpful.

Second election period

Covered plans will have to give a special 60-day COBRA election period to individuals who would be subsidy-eligible but did not elect COBRA, or who elected COBRA but dropped it or had it canceled for failure to pay premiums. This second election period applies only if the COBRA coverage period would still be in effect as of April 1 if the AEI had elected COBRA coverage when first eligible.

Required notice and election period. Employers or plan administrators must provide the special election notice by May 31. The second election period runs from April 1 until 60 days after the new COBRA notice “is provided” to the individual. The date on which the notice “is provided” likely means the date the notice is sent rather than received, but confirmation from the agencies is needed. Any delay in sending the notice extends the second election period. However, employers may want to wait for DOL’s model notice, which is expected by April 10 (see “Required employer notices” below for more information).

COBRA coverage period. AEIs getting a second election opportunity do not have to elect COBRA coverage retroactive to the date they were first eligible. Instead, coverage elected during the second election period begins when the subsidy period begins on April 1. However, the normal 18-month COBRA coverage period for all second-chance AEIs is measured from the date of the original qualifying event (involuntary job loss or reduced hours) and loss of coverage. The subsidy does not extend the applicable COBRA coverage period. Here are some examples:

- Jim, an AEI, first became eligible for COBRA coverage on May 1, 2020, but didn’t elect it. During the second election period, Jim can elect COBRA coverage effective April 1, 2021, and pay no premiums through September. Jim’s COBRA coverage can continue through October 2021 (the end of the 18-month coverage period) if he pays the premium for that month.

- Judy, an AEI, became eligible for COBRA coverage on Dec. 1, 2019. She elected COBRA coverage, but lost it when she failed to pay the premiums for January and February 2020. Judy can elect coverage effective April 1, 2021, and pay no premium for April and May. Judy’s 18-month COBRA coverage period will end after May.

- Jon became eligible for COBRA on Sept. 1, 2019. Jon is not eligible for the second COBRA election period because the 18-month coverage period applicable to Jon’s COBRA right expired before April 1, 2021.

Required employer notices

Covered plans will have to identify subsidy-eligible individuals and provide them a notice explaining these new rights. Covered plans will also need to provide advance notice informing COBRA beneficiaries about the subsidy’s end date. This notice is due 15 to 45 days before the subsidy expires. DOL is responsible for developing model notices that employers can use.

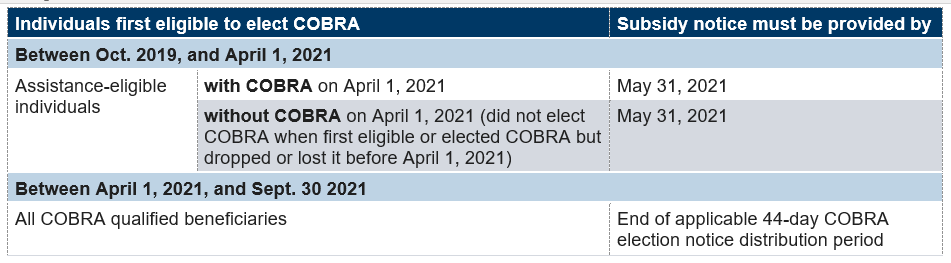

Subsidy availability and second election notice

Everyone who becomes eligible for COBRA for any reason during the subsidy period (April 1 through Sept. 30) must receive information about the subsidy as part of the regular COBRA election notice process. The law seems to require providing this notice even to individuals who are ineligible for the subsidy because an event other than involuntary job loss or reduction in hours triggered the COBRA right. AEIs who have already elected COBRA and have a coverage period extending past April 1 must also receive information about the subsidies. Qualified beneficiaries who never elected COBRA or who elected and later dropped or lost it must receive notice about the subsidy and the second election opportunity, unless their original 18-month coverage expired before April 1.

The next chart outlines the timing of notice distribution to different groups of COBRA-eligible individuals.

DOL to issue model notice by April 10. The law requires DOL to issue a model notice by April 10. While the law outlines content requirements for the notice, some details are unknown. Employers may want to wait for the model rather than risk having to send a corrected notice.

Required content. Employers can use the DOL model notices when issued or create their own notices about the subsidy and second election period. Whether provided as a separate document or incorporated into an existing COBRA notice, the information must be clear and understandable. Since anyone becoming eligible for COBRA coverage between April 1 and Sept. 30 apparently must receive a notice about the subsidy, employers may wish to emphasize the requirements for subsidy eligibility to help avoid confusion.

The notice must contain the following information:

- A description of the qualified beneficiary’s right to the COBRA subsidy and any conditions on entitlement

- A description of the option to enroll in different coverage, if the employer chooses to allow

- The forms necessary to establish subsidy eligibility

- Contact information for plan administrator and any other person relevant to the subsidy program

- A description of the second election period

- A description of qualified beneficiaries’ obligation to notify the plan to if they become eligible for other group health plan or Medicare coverage and the penalty for failure to do so

The DOL model notice or other guidance is expected to give more details on the required content, including what information is necessary for an individual to establish subsidy eligibility.

Subsidy expiration notice

Covered plans must inform COBRA enrollees about the subsidy’s expiration 15 to 45 days in advance of the end date. This advance notice is required for COBRA enrollees with a coverage period extending until or beyond the Sept. 30 end of the subsidy period and appears to be required when someone’s COBRA coverage period will end before Sept. 30. DOL likely will issue clarifying guidance with the model notice, which is due by April 25. The notice is not required if the subsidy is ending because an individual has become eligible for other group health coverage or Medicare.

The notice must clearly and unambiguously specify the date when the subsidy will expire for the individual. The notice must also make clear that the individual may be eligible to continue COBRA coverage without the subsidy.

Employers may want to confirm that the notice includes information about coverage available through the marketplace. Marketplace coverage may be more affordable than unsubsidized COBRA coverage for some, since Congress has expanded eligibility and increased subsidies for ACA marketplace coverage through 2022. In the past, the federal marketplace has offered a special enrollment period when an employer COBRA subsidy ends. Whether the federal marketplace will offer similar special enrollment period to COBRA enrollees when the federal subsidy ends or extend the current COVID-19-related special enrollment period beyond Aug. 15 remains to be seen. Information on this point from HHS would be helpful.

Notice failure

A failure to satisfy ARPA’s notice requirements will be considered a failure to notify qualified beneficiaries of their right to elect COBRA coverage. Such failures can expose the employer to excise tax penalties of $110 per day for each failure and litigation brought by qualified beneficiaries seeking damages, as well as attorney fees and interest.

Interaction with outbreak period relief

To provide relief during the COVID-19 National Emergency that began March 1, 2020, the agencies extended the deadlines for a number of employee benefit plan requirements, including the time for plans to provide COBRA election notices and for qualified beneficiaries to elect COBRA coverage. The deadline relief applies during the “outbreak period,” defined as the period from March 1, 2020, through 60 days after the announced end of the COVID-19 National Emergency.

COBRA subsidy notice and second election

Whether the outbreak period relief will apply to the second COBRA election opportunity or a plan’s deadlines to provide the required COBRA subsidy notices is unclear. Excluding these COBRA subsidy matters from the outbreak period relief would ensure speedy assistance to individuals needing subsidized coverage. This exclusion would also ensure employers can promptly claim the corresponding tax credit for the quarter in which individuals received subsidized coverage (see “Subsidy mechanics” below). A delay due to outbreak period relief would require employers to file corrected quarterly forms to claim the applicable credits. Clarification from the agencies about the interaction of the outbreak period relief with the COBRA subsidy’s second election period and required notices would be welcome.

Other COBRA deadlines

The outbreak period relief may still apply to other COBRA deadlines before and after the subsidy period. AEIs who didn’t elect COBRA or who elected but dropped or lost it can use the second election chance to activate coverage during the subsidy period (unless their original COBRA coverage period has expired). As the law reads, these individuals don’t have to elect or pay for coverage retroactive to their first month of eligibility. But if applicable, the outbreak period relief may still provide them time to elect and pay for coverage back to the first month of eligibility.

Example. Jim, an AEI, became eligible for COBRA coverage on May 1, 2020, but he didn’t elect it. During the second COBRA election period, he elects coverage effective April 1, 2021, and pays no premium for April through September.

─ Can Jim still elect COBRA coverage retroactive to May 1, 2020, using the outbreak period relief?

─ If Jim can and does elect COBRA coverage retroactive to May 1, 2020, does he have extended time to pay the premium due for those months of retroactive coverage, using the outbreak period relief?

─ When Jim’s subsidy expires, if he wants to continue his coverage through October (the end of his original 18-month COBRA period), will his deadline for paying the October premium be subject to the outbreak period relief (assuming the COVID-19 National Emergency is still in effect)?

Until regulators provide other guidance, the COBRA election period and premium payment deadlines occurring during the outbreak period are still subject to the outbreak period relief. Therefore, those deadlines are eligible for extensions of up to one year or the end of the outbreak period, whichever occurs first.

Subsidy mechanics

AEIs pay nothing during the subsidy period. Employers cover the premium cost for AEIs by paying the carrier or, in the case of self-funded plans, absorbing the cost. Employers will be reimbursed for these costs as described below. If an AEI pays the COBRA premium for a month in which the subsidy applies, the employer must refund the individual within 60 days of the payment date.

Tax credit for employers

Most employers sponsoring insured or self-funded group health plans covered by the law will be reimbursed by the federal government for 100% of each eligible individual’s COBRA premium (including the administrative fee) for April through September 2021. The subsidy will take the form of a Medicare payroll tax credit, which could result in direct payment to employers whose Medicare tax liability is less than the credit.

Multiemployer plans and insurance carriers. Premium subsidies are available for COBRA coverage provided by Taft-Hartley multiemployer plans and state-mandated continuation coverage provided by insurers to employer plans exempt from the federal COBRA law (employers with fewer than 20 employees). These other entities will be able to claim the tax credit.

Payroll tax offset

Employers will claim the subsidy by reporting 100% of eligible individuals’ premium costs (including administration fees) as an overpayment of Medicare payroll taxes reported quarterly on Form 941 or more frequently by offsetting payroll tax deposits during the quarter. Employers likely will be able to claim the credit against their total payroll tax liability rather than against payroll taxes directly owed on behalf of the eligible individual. The credit is refundable and may be advanced. If the credit exceeds the Medicare taxes owed for the quarter, the excess is treated as an overpayment and refunded to the payer.

Forms and instructions are expected. For other advance COVID-19-related credits, IRS has permitted employers to reduce tax deposits or use Form 7200 to claim the credit before filing the quarterly Form 941. IRS guidance is expected to confirm this approach.

No double benefit. Employers’ gross income will be increased by the amount of the credit. In addition, employers cannot use the same payroll amounts to claim both the COBRA subsidy credit and either the employee retention credit under the Coronavirus Aid, Relief and Economic Security (CARES) Act or the credit for emergency paid sick or family leave under the Families First Coronavirus Response Act (FFCRA).

Employer reporting required

Employers must maintain certain information related to the payroll tax offset, although they may not need to submit this information when claiming the credit. Supporting documentation could include:

- Attestation of individual’s involuntary termination or reduction in hours, including the date

- Proof of eligibility for and election of COBRA continuation coverage during the relevant period

- Each AEI’s Social Security number, subsidy amount and scope of subsidized coverage (one person or multiple people)

Guidance from Treasury is expected.

Implications for individuals

The subsidy is not included in an individual’s taxable gross income. Recipients of the COBRA subsidy are not eligible for the Trade Adjustment Assistance program's health coverage tax credit (HCTC) for any month for which the COBRA subsidy is received. The HCTC offsets 72.5% of the cost of qualified health insurance — including coverage under COBRA or funded by certain voluntary employees’ beneficiary associations — for eligible trade-displaced workers and certain PBGC payees. The Consolidated Appropriations Act of 2021 has extended this credit through 2021.

Next steps for employers

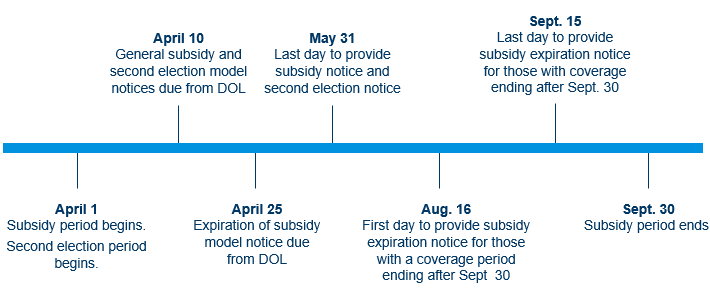

The COBRA subsidy program requires immediate employer action, including creating subsidy-related notices, coordinating with vendors and insurers, revising COBRA notice and payroll processes, and deciding whether to offer subsidy-eligible individuals the option to move to less expensive coverage. Important dates are noted in the the following timeline.

Other important dates to keep in mind:

- COBRA notices must be sent to newly qualified beneficiaries within 44 days of the qualifying event (barring application of the outbreak period relief).

- Employers must refund premiums paid by AEIs during the subsidy period within 60 days of the payment date.

- AEIs have 60 days to elect COBRA from the date the second election notice is sent.

- AEIs have 90 days to switch plans, if permitted by the employer, from the date the subsidy notice is sent.

- AEIs with COBRA coverage periods expiring before Sept. 30, 2021, apparently must receive a notice specifying the date the COBRA subsidy will end 15 to 45 days before the end date.

Employers should watch for evolving agency guidance that could affect legal obligations and internal and vendor plan processes. In the meantime, here are some important activities to get ready.

Identify individuals who became eligible for COBRA after Oct. 1, 2019. Most must receive enhanced notices, and some may be entitled to a second chance to elect COBRA coverage. Identify who within this group became eligible for COBRA due to an involuntary employment termination or a reduction in hours. This will help determine who must receive the required notices and how many people may be eligible to receive the subsidy.

Provide subsidy-related notice. Decide whether to use DOL’s model subsidy notice or create a custom notice incorporating required subsidy information. In either case, decide whether to integrate the subsidy information into the regular COBRA election notice or provide as a separate document. Because the subsidy program is temporary, a separate document included with the election notice may simplify administrative work. Consider highlighting the eligibility criteria and the individual’s obligation to inform the plan of eligibility of other group coverage or Medicare.

Consider temporarily redesigning severance programs. Unless agency guidance clarifies that employers can claim the full tax credit during the subsidy period when voluntarily subsidizing COBRA as part of their severance policies or practices, employers may want to reconsider how to structure this benefit in the short term. For example, if an employer provides taxable cash instead of subsidizing COBRA in the severance package, AEIs could receive COBRA free of cost with the federal subsidy and the employer could claim the full tax credit from April 1 through Sept. 30. Alternatively, for qualified beneficiaries with COBRA coverage beyond September, an employer could shift the severance benefit to subsidize the coverage period after Sept. 30. This way, the employer could claim the full tax credit and AEIs would receive free COBRA during the federal subsidy period and then have the employer severance benefit after the federal subsidy ends.

Coordinate with vendors and insurers. The subsidy program presents challenges for COBRA administrators, insurers and payroll vendors:

- COBRA administrators and insurers. If COBRA is administered by an insurer or a third-party administrator, employers should discuss how to help the vendor successfully administer the subsidy program. Vendor activities may include revising and sending COBRA election notices, eliminating charges for COBRA premiums, tracking each eligible individual’s subsidy period, and helping to refund premium payments by individuals entitled to the subsidy.

- Payroll vendors. Employers using payroll vendors should ensure the vendor is prepared to administer the subsidy program. This could include tracking each individual’s subsidy eligibility, as well as collecting and submitting information for claiming the payroll tax offset and reporting on Form 941.

- Stop-loss carriers. Employers with self-insured group health plans should contact stop-loss insurers to ensure coverage of individuals electing COBRA coverage during the second election opportunity.

Address internal processes. Employers need to address internal COBRA administrative processes and the linkages between internal and external COBRA and payroll functions. Key tasks include properly tracking AEIs, calculating the subsidies to recover through payroll tax processes and maintaining supporting documentation. Careful and timely communication between the COBRA and payroll functions is critical, as an overstatement of the subsidy will be considered an underpayment of payroll taxes, potentially triggering penalties. Employers should decide whether to claim the subsidy as an offset against payroll tax deposits or as an overpayment using Form 941. Payroll systems may need revisions to reflect the subsidy claims, and accounting procedures may need modifications to reflect the timing and method for claiming the payroll tax offsets.

Project additional costs. Consider projecting additional costs that could flow from implementation, including expenses from the potential increase in COBRA elections due to the second election opportunity, administrative costs of providing additional notices, and general internal expenses related to payroll and COBRA administrative changes

Related resource

- Pub. L. No. 117-2, the American Rescue Plan Act (March 11, 2021)