A primer on ERISA’s preemption of state laws

In recent years, more states have enacted laws that may regulate private-sector employee benefits, such as employer-sponsored prescription drug coverage, or impose requirements on employers that don’t offer certain benefits. ERISA preemption plays a major role in considering the scope of a state benefit or insurance law and its applicability to employee benefit plans. However, determining whether ERISA preempts a particular state law isn’t always straightforward and can present challenges for employers, so the courts sometimes must step in to determine if preemption applies. This GRIST provides a basic primer on ERISA’s preemption of state laws, including various exceptions, exclusions and court rulings.

ERISA preemption

In enacting ERISA in 1974, Congress sought to provide national standards for employee benefit plans, including reporting, disclosures, fiduciary responsibilities, claims/appeals and remedies for noncompliance. To minimize the potential patchwork effect of each state enacting their own laws regulating employee benefits, Congress included a broad preemption of state laws that could interfere with the uniform administration of ERISA plans.

ERISA (29 US Code § 1144) generally preempts “any and all state laws” to the extent they “relate to” employee benefit plans, but a complex body of court decisions and federal guidance surrounds this issue. Only federal courts can ultimately determine whether ERISA preemption applies, though the Department of Labor (DOL) has issued its own preemption guidance from time to time. Courts have recognized that Congress, in adopting a broad preemption scheme, intended ERISA alone to regulate private-sector employee benefits and avoid conflicting state and local regulations. Plans and plan sponsors are subject to this uniform body of law, including core functions like reporting and disclosure, to encourage employers to continue to sponsor retirement benefits and health coverage. Nevertheless, certain exceptions and limitations apply to ERISA preemption.

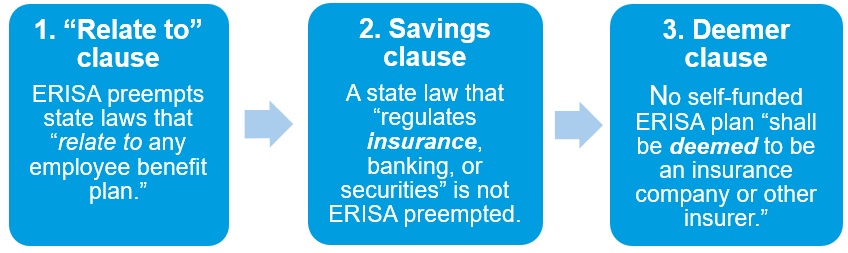

ERISA preemption framework

ERISA preemption generally involves a three-step analysis using three parts of the statute:

‘Relate to’ clause

The US Supreme Court said that a law relates to an ERISA plan if it “has a connection with or reference to” the plan. For example, in Shaw v. Delta Air Lines, Inc. (463 U.S. 85 (1983)), the court held that a New York nondiscrimination law that didn’t mirror a federal law could not require a self-funded ERISA plan to provide specific coverage. In Bergin v. Wausau Ins. Cos. (863 F. Supp. 34 (D. Mass. 1994)), a federal district court said a Massachusetts health coverage continuation law for divorced spouses can’t apply to a self-funded ERISA plan subject to COBRA (which is a part of ERISA).

However, the Supreme Court also held that such connections can’t “extend to the furthest stretch of its indeterminacy” (NY State Conference of Blue Cross & Blue Shield Plans v. Travelers Ins. Co., 514 U.S. 645 (1995)). One key preemption issue courts must weigh is whether a state law primarily relates to an employee benefit plan or is mainly a general payroll tax or business assessment that only incidentally relates to ERISA-governed plans. In Travelers, the court held that a law assessing a fee on all hospital payers has general applicability and an “indirect economic effect” on ERISA plans that might increase costs, but doesn’t directly regulate plans.

More recently, the court unanimously held that an Arkansas statute regulating only the relationship between pharmacy benefit managers (PBMs) and pharmacies does not make “reference to” or have an impermissible “connection with” ERISA plans (Rutledge v. Pharm. Care Mgmt. Ass’n (140 S. Ct. 474 (2020)). A later 8th US Circuit Court of Appeals ruling applied the principles in Rutledge to reject an ERISA preemption challenge to a North Dakota PBM law that imposes significant restrictions on PBMs (Pharm. Care Mgmt. Ass’n v. Wehbi, No. 18-2926 (8th Cir. Nov. 17, 2021)).

Savings clause

ERISA saves from preemption state laws regulating the business of insurance, banking or securities. A state law that relates to an employee benefit plan may still be valid if a court concludes that the law falls within this category. The US Supreme Court set the parameters for such a determination when it ruled that the law or practice being challenged must have the effect of transferring or spreading a policyholder’s risk and be an integral part of the policy relationship. In KY Ass’n of Health Plans, Inc. v. Miller (538 U.S. 329 (2003)), the court clarified that a state’s “any willing provider law” was specifically directed at entities engaged in insurance and met the test that a state law must “substantially affect the risk pooling arrangement between insurer and insured” to fall within ERISA’s savings clause. A state law is valid, even if it has a “minimal application to noninsurers.”

Deemer clause

A state cannot deem a self-funded employee benefit plan as insurance for the purpose of imposing state regulation. For example, in FMC Corp. v. Holliday (498 U.S. 52 (1990)), the US Supreme Court held that a Pennsylvania financial responsibility law for motor vehicles did not prohibit a self-funded medical plan from exercising its subrogation rights. The court summarized the deemer clause this way:

Our interpretation of the deemer clause makes clear that if a plan is insured, a State may regulate it indirectly through regulation of its insurer and its insurer’s insurance contracts; if the plan is uninsured, the State may not regulate it.

Uniform plan administration

A purported goal of ERISA is to establish standards of conduct for plan sponsors, administrators and service providers. Its preemption clause ensures that plan sponsors can apply uniform plan administration across states and needn’t comply with multiple, sometimes conflicting state laws. Plan administration — including reporting, disclosures and benefit payments — and enforcement are under the sole jurisdiction of federal regulators.

Reporting and disclosure

ERISA regulations (29 CFR Part 2520) require plan sponsors to provide participants with a summary plan description outlining benefits, eligibility and other plan details. Under federal law, plan sponsors also must provide summaries of benefits and coverage and other disclosures. With some exceptions, plans must file annual Form 5500 reports. In Gobeille v. Liberty Mutual Ins. Co. (577 U.S. 312 (2016)), the US Supreme Court noted that “extensive reporting, disclosure, and recordkeeping are central to, and an essential part of this uniform plan administration system.” The court held that preemption of a Vermont health plan reporting law “is necessary to prevent the States from imposing novel, inconsistent, and burdensome reporting requirements on plans.”

Benefit determination

An ERISA plan administrator generally has authority under the plan to determine benefit eligibility. In Egelhoff v. Egelhoff (532 US 141 (2001)), the US Supreme Court held that ERISA preempts a Washington law that revokes a spouse’s designation as beneficiary on divorce. The ruling allows plan sponsors to rely on a plan’s documents and procedures for determining the identity of beneficiaries without worrying whether state laws might impose different outcomes.

ERISA’s exclusive remedies

A law that regulates insurers may not necessarily be “saved” — even if a plan is insured — if the law would interfere with ERISA’s “exclusive remedy scheme” (29 US Code § 1132), which permits participants to seek promised benefits or other redress. In Pilot Life Ins. Co. v. Dedeaux (481 U.S. 41 (1987)) and Aetna Health Inc. v. Davila (542 U.S. 200 (2004)), the US Supreme Court ruled that a Mississippi bad-faith law and a Texas healthcare liability law weren’t saved from preemption. In both cases, the court held that Congress intended ERISA’s civil enforcement provisions to be the exclusive remedy. Any state-law cause of action that duplicates, supplements or supplants ERISA’s civil enforcement remedy conflicts with the clear congressional intent, according to the court. The Mississippi and Texas laws fell into this category and could not survive ERISA preemption.

Payroll deductions and automatic contribution arrangements

DOL’s longstanding view is that ERISA preempts state wage-withholding laws to the extent they limit, prohibit or regulate deductions from employees’ wages for contribution to ERISA-covered plans (DOL information letter (Dec. 4, 2018)). Despite the expansive language of ERISA’s preemption clause, the Pension Protection Act of 2006 (PPA) (Pub. L. No. 109-280) added a new provision to ensure that state laws wouldn’t interfere with automatic contribution arrangements in ERISA retirement plans (29 US Code § 1144(e)). An automatic contribution arrangement treats participants as if they elected to contribute a certain percentage of compensation to the retirement plan, unless they affirmatively elect a different percentage or opt out of contributing. Unlike ERISA’s general preemption clause, the PPA amendment requires annual participant notices with specific information about the automatic contribution arrangement. However, DOL’s implementing regulations state that ERISA preemption still applies if an automatic enrollment arrangement doesn’t meet all of the PPA amendment’s conditions (29 CFR § 2550.404c-5(f)(2)).

Preemption exceptions and exclusions

Some ERISA-governed plans may need to comply with certain state laws if Congress provided a specific exception or excluded particular categories of state activity from ERISA’s broad preemption scheme. In addition, ERISA doesn’t preempt the application of state laws to non-ERISA plans or benefit programs.

Specific preemption exceptions and exclusions

Though a plan may fall within the definition of an ERISA plan (29 USC § 1002(3)), preemption doesn’t apply to state laws in the areas described below.

Hawaii Prepaid Health Care Act

The Hawaii Prepaid Health Care Act (HPHCA) requires private employers to provide healthcare coverage for all eligible Hawaii employees. ERISA provides a specific carve-out for the HPHCA (29 USC § 1144(b)(5)(A)), allowing Hawaii to determine which healthcare benefits an employer may or must provide.

Multiple employer welfare arrangements (MEWAs)

ERISA defines a MEWA as any arrangement (whether insured or self-insured) providing health or other welfare benefits to employees (and their beneficiaries) of two or more employers that are not members of the same controlled group. The definition excludes plans maintained under one or more collective bargaining agreements by rural electric cooperatives or rural telephone cooperative associations. ERISA allows any state insurance law to regulate MEWAs to the extent it “is not inconsistent with” ERISA. In Advisory Opinion 2005-18A, DOL clarified that it won’t consider a state insurance law inconsistent with ERISA if it requires ERISA-covered MEWAs to meet more stringent standards of conduct or to provide greater protection to plan participants and beneficiaries than ERISA requires.

Specific exclusions

ERISA doesn’t preempt certain categories of state laws or activities, even if they relate to an ERISA-governed plan:

- Medicaid recoupment. Medicaid is generally the payer of last resort. States may collect payments from a liable third party, including an ERISA-governed group health plan, to recoup Medicaid benefits erroneously paid on behalf of Medicaid beneficiaries.

- Qualified medical child support orders. A qualified medical child support order (QMCSO) allows a nonemployee custodial parent to obtain health coverage for his or her child from the employee parent’s group health plan.

- Qualified domestic relations orders. A qualified domestic relation order (QDRO) creates or recognizes an “alternate payee’s” right to receive all or a portion of the benefits payable under a participant’s retirement plan.

- Generally applicable criminal laws. For example, a state could prosecute company executives for allegedly embezzling ERISA plan funds.

Non-ERISA plans

Certain plans and practices aren’t subject to any ERISA requirements. As a result, these plans may be subject to state laws:

- Church plans established and maintained by a church, a convention or association of churches, or an affiliated organization

- Governmental plans established or maintained by a state, local or federal government entity

- Plans established to comply with state-mandated short-term disability benefit programs

- State-mandated retirement savings programs — state or local programs requiring employers that don’t sponsor a retirement plan to automatically enroll their employees in a government-administered individual retirement account (IRA)

- Payroll practices — plans that pay all or part of an employee’s normal compensation from an employer’s general assets while the employee is absent due to sick or disability leave, vacation, military leave, jury duty or training

- Voluntary plans in which employees bear the full cost of the plan, participation is entirely voluntary, and the employer doesn’t endorse or benefit financially from the plan

- Miscellaneous plans and fringe benefits such as:

- Health savings accounts

- Workers’ compensation or unemployment plans

- Expatriate plans maintained outside the United States primarily for nonresident aliens

- Plans covering only self-employed individuals

- Adoption and tuition assistance programs

- Employee assistance programs that do not provide any health services

- Unfunded scholarship and dependent care plans, including dependent care flexible spending arrangements

- Other fringe benefits provided under the Internal Revenue Code (such as qualified transportation benefits)

- Severance plans that do not involve an administrative scheme

Plan sponsor considerations

While ERISA preemption somewhat buffers group health and retirement plans from state regulation, plan sponsors will want to note whether any given state law could affect their plans — even self-funded ones. If in doubt, employers should review a state law or pending bill with legal counsel to understand its scope and potential applicability. Sponsors also should keep in mind that ERISA doesn’t preempt other federal laws, including federal nondiscrimination, securities and health information privacy laws.

Related resources

Non-Mercer resources

- Pharm. Care Mgmt. Ass’n v. Wehbi, No. 18-2926 (8th Cir. Nov. 17, 2021)

- Howard Jarvis Taxpayers Ass’n v. Cal. Secure Choice Ret. Sav. Program, No. 20-15591 (9th Cir. May 26, 2021)

- Rutledge v. Pharm. Care Mgmt. Ass’n, 140 S. Ct. 474 (2020)

- Information letter (DOL, Dec. 14, 2018)

- Advocate Health Care Network v. Stapleton, 137 S. Ct. 1652 (2017)

- Gobeille v. Liberty Mutual Ins. Co., 577 U.S. 312 (2016)

- Multiple employer welfare arrangements under ERISA: A guide to federal and state regulation (DOL, August 2013)

- Advisory Opinion 2005-18A (DOL, Aug. 1, 2005)

- Aetna Health Inc. v. Davila, 542 U.S. 200 (2004)

- KY Ass’n of Health Plans, Inc. v. Miller, 538 U.S. 329 (2003)

- Egelhoff v. Egelhoff, 532 US 141 (2001)

- NY State Conference of Blue Cross & Blue Shield Plans v. Travelers Ins. Co., 514 U.S. 645 (1995)

- Bergin v. Wausau Ins. Cos., 863 F. Supp. 34 (D. Mass. 1994)

- FMC Corp. v. Holliday, 498 U.S. 52 (1990)

- Pilot Life Ins. Co. v. Dedeaux, 481 U.S. 41 (1987)

- Shaw v. Delta Air Lines, Inc., 463 U.S. 85 (1983)

- Metro. Life Ins. Co. v. Massachusetts, 471 U.S. 724 (1985)

Mercer Law & Policy resources

- Resources for tracking state and city retirement initiatives (March 2, 2022)

- 2022 health law and policy outlook (Feb. 24, 2022)

- Hawaii employee health and leave benefits may need special attention (Feb. 18, 2022)

- States update group health plan sponsor reporting obligations (Jan. 21, 2022)

- 2022 state paid family and medical leave contributions and benefits (Jan. 19, 2022)

- Seattle posts 2022 health expenditure rate for hotel employers (Aug. 17, 2021)

- San Francisco updates city option, 2022 health care expenditure rate (Aug. 12, 2021)

- Supreme Court upholds Arkansas law regulating PBMs (Dec. 10, 2020)

- Seattle healthcare expenditure for hotels survives ERISA challenge (Aug. 4, 2020)

- Justices’ Title VII ruling on LGBTQ bias has health benefit impacts (June 15, 2020)