Rewards

95% of employers plan to invest in total rewards over the next 12 months.

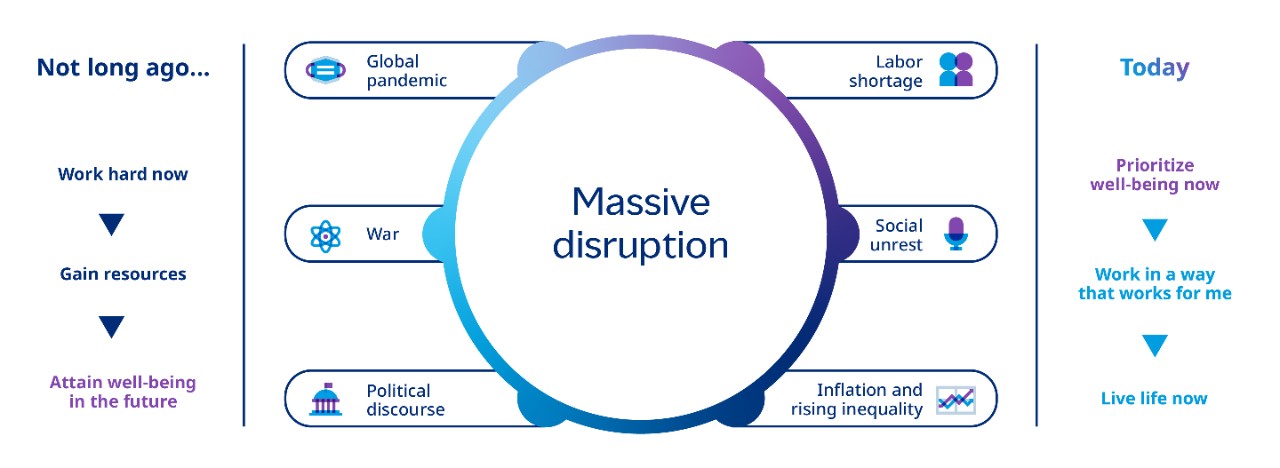

It's time for change

Four actions for getting started

-

Lead with listening

-

Get to the heart of the issue

-

Identify where you want to shine

-

Engage for impact

Amplifying intelligence in total rewards

-

Predictive performance analytics

-

Pay equity and transparency

-

Rewards and recognition

-

Executive compensation

Five strategies to future-fit total rewards

Job structures have become chaotic due to the pandemic, high turnover, hybrid work and changing workforce attitudes. Recent labor shortages, high inflation and demand for hot skills have driven salary expectations higher.

Many firms have added roles and expanded job titles without cohesive planning. As pay equity and transparency demands grow, this approach is unsustainable.

Simplifying job architecture and pay structures is crucial for fair compensation, especially if you plan to adopt skills-based pay. Start by auditing for redundancies and inequities, then use market analytics to value job activities, levels and skills. Simplification is critical to sustainable compensation.

Total rewards programs are a significant investment in your people. To optimize ROI, align your offerings with what matters most to your talent.

If your workforce is younger, prioritize relevant options like student loan assistance, wellness programs, enhanced learning and career opportunities over top-dollar retirement benefits. As diversity grows, a one-size-fits-all approach is unsustainable.

Offer flexibility with digital platforms that let employees personalize their rewards. Tools like the Mercer Rewards Optimizer™ help employers tailor packages to each employee segment, ensuring resources are directed to programs with the greatest impact.

Today's labor market has changed. Many firms adopted skills-based recruiting and flexible work models during the pandemic, leading to a dispersed talent pool. Now, employers compete across industries and geographies for the same talent.

For example, a Silicon Valley tech company now competes globally for tech-savvy employees, often against firms paying less in lower-cost areas. This competition spans industries from banking to retail.

To succeed, evolve your total rewards strategy to stay updated on broader market data and adapt your programs for critical jobs and workers. These steps are crucial for competing for top talent.

Are you maximizing your data? AI tools and analytics can uncover trends and insights for smarter decisions.

Auditing rewards programs ensure equitable decisions on salaries, incentives, and career advancement, reflecting core values of diversity, equity, and inclusion. In a transparent environment, top employers use data to make informed, fair decisions, identifying areas needing attention and living up to their values. Regardless of how progressive your company is, data can enhance your efforts.

Your total rewards team is like a sports team, with each member specializing in different areas. This specialization is efficient but crucial decisions require collaboration:

- How much budget do we need?

- How do we allocate bonuses to engage top performers?

- Where should we cut back on prioritizing critical areas?

Specialists must pool their knowledge and resources, using data and understanding employee needs. Open communication and a holistic approach are essential.

Teamwork connects these actions and ensures cohesive decisions about job structuring, spending and talent management. Breaking down silos fosters a unique, competitive employee experience.