Inflation protection considerations

Building inflation protection into portfolios requires broad diversification across a number of asset classes and strategies.

As a consequence of unprecedented levels of accommodative monetary policy during the pandemic, inflation is now rearing its head swiftly and extremely, further exacerbated by surging energy and food costs, extended periods of supply chain disruptions and major geopolitical events. Beyond these very short-term drivers, we believe long-term inflation risk has increased due to a number of structural reasons, as outlined below.

Portfolio construction needs to reflect increased inflation risk. Traditional portfolios, dominated by equities and bonds, have performed exceptionally well through the benign environment of disinflationary growth and negative equity-bond correlations over the last decade. But in an environment of persistently higher and more volatile inflation, such portfolios could suffer if not pro-actively positioned for different inflation scenarios.

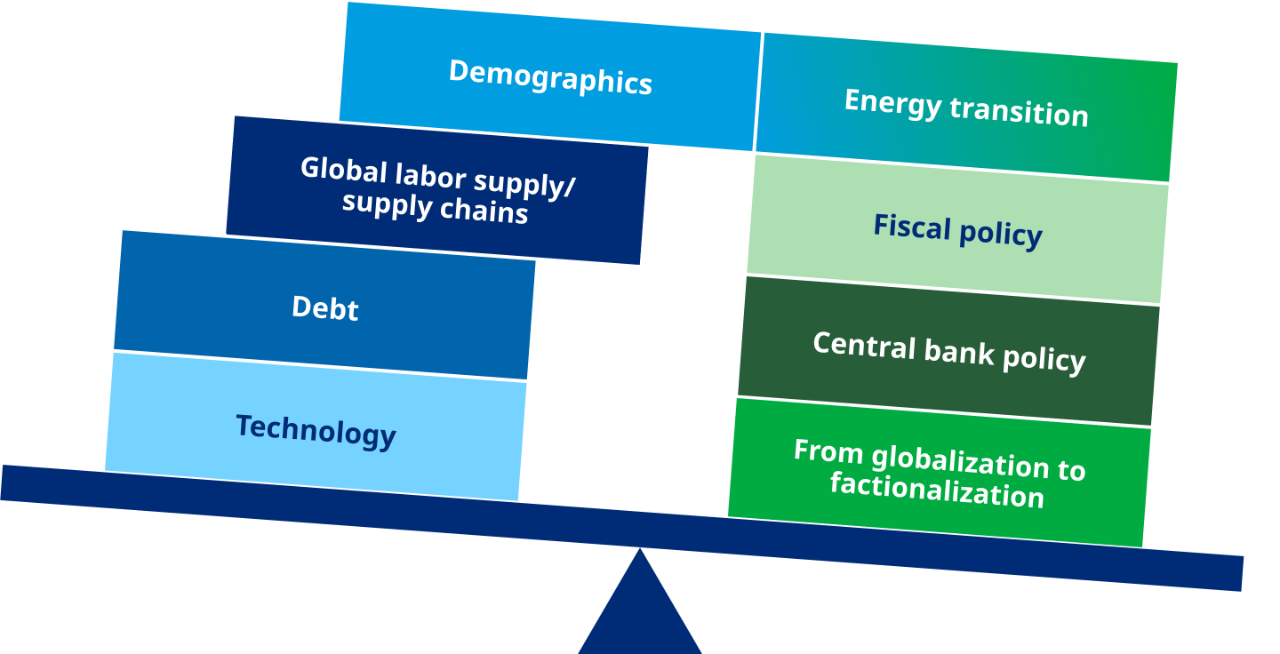

Factors that determine the course of inflation

Drivers of disinflationary pressures

Drivers of inflationary pressures

The impact of inflation on conventional portfolios

Many portfolios have been constructed during and for disinflationary environments. Dominated by equities and bonds and alternative asset classes like private equity, real assets and more aggressive credit-oriented fixed income strategies, they have performed strongly throughout the past two decades. The secular trend of declining yields increased discounted values of dividends and coupon payments was an additional tailwind.

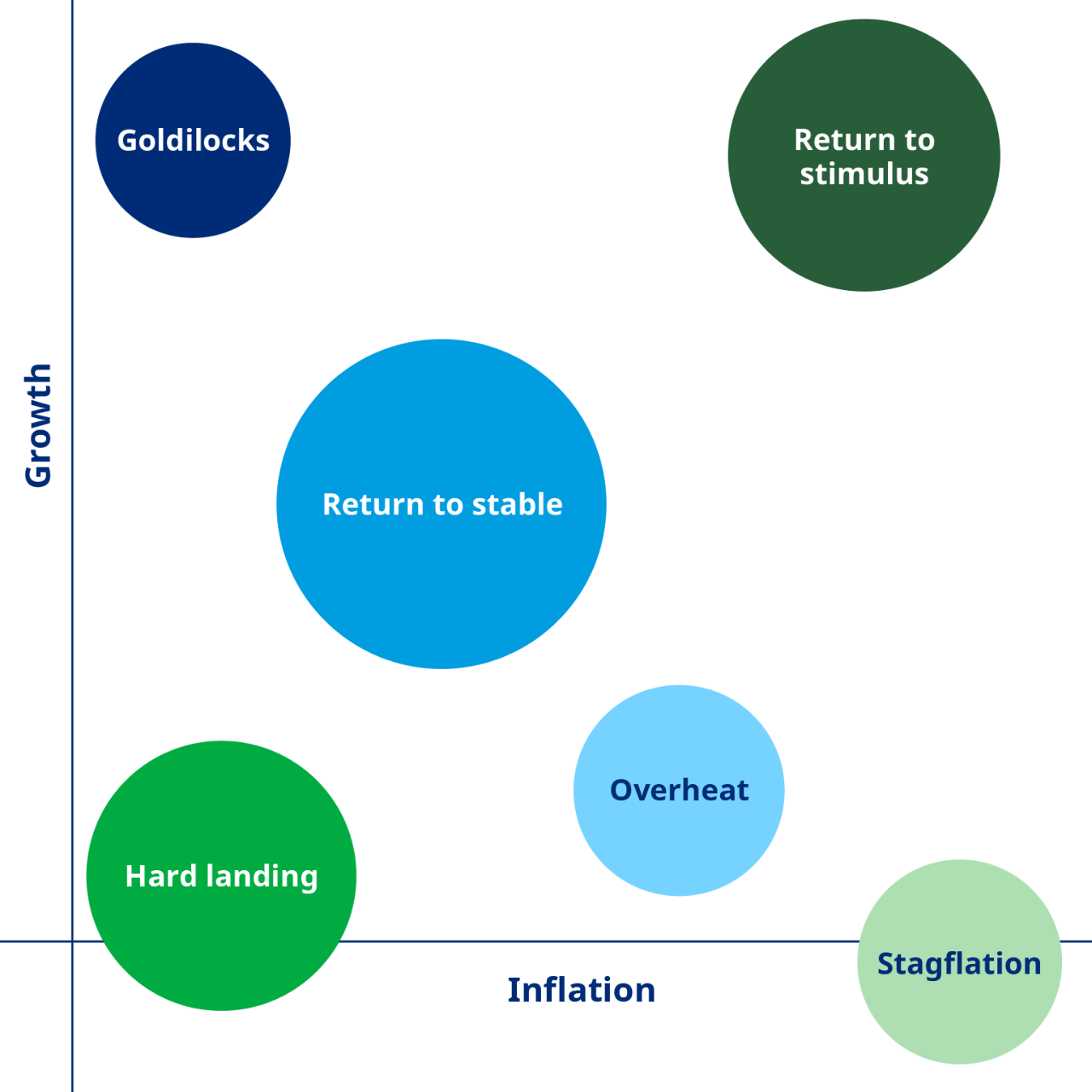

An environment of structurally higher inflation changes this equation. First of all, portfolios need to be better positioned for inflation eroding real returns and have sufficient exposure to asset classes that keep up with inflation. Second, portfolios need to not just position for recurring transitions between recessionary and non-inflationary growth environments (bottom of the chart) but add an inflation dimension (top of the chart).

Figure 2

Structurally higher inflation also impacts portfolio constructions beyond just protecting portfolios against the direct consequences of inflation.

Portfolio diversification was supported by the typically negative correlation between equities and fixed income in disinflationary times, especially in major stress events, when it was needed most. Why was that? With inflation being structurally low and cyclical, rising inflation was associated with economic growth that benefited equities and hurt government bonds due to central banks tightening policy preemptively and vice versa. So, when one part of the portfolio went up, the other part went down.

However, however, in an environment when inflation is structurally high, rising inflation and monetary tightening is not necessarily associated with economic growth anymore so both equities and bonds suffer at the same time. Portfolios become harder to diversify which increases complexity for portfolio construction. Asset allocators need to work much harder to build downside protection into portfolios.

Although some portfolios will employ inflation protection through investing in inflation-linked bonds, which also come with limitations, few portfolios appear comprehensively hedged against a broader range of inflation scenarios that we may now be facing.

How to assess the direction of prices

Scenario analysis is particularly useful at times like these, when the probability of a regime shift — specifically, a shift to a higher inflation regime — has increased. History has shown us how frequently regimes have shifted between secular inflation and disinflation.

This has informed our decision to allow for future inflation regimes to be materially different from that of the past four decades, even though a return to a benign disinflationary environment is also a possibility.

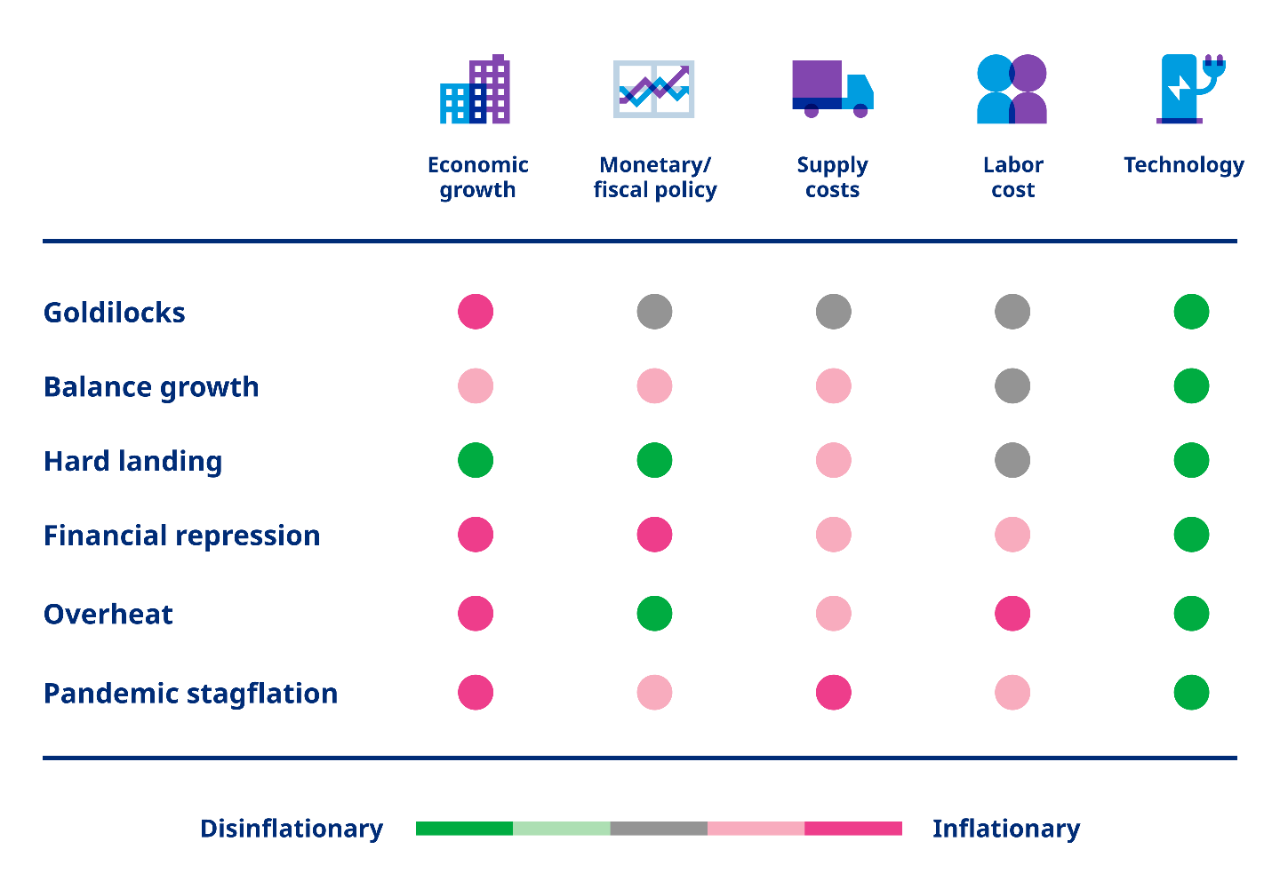

Figure 3 considers different scenarios of how economies and markets could behave under different conditions. These are forward-looking assessments set over a three-year time horizon. They span inflationary and disinflationary conditions, cost-push and demand-pull drivers of inflation, and strong and weak growth, factoring in the influence of central bank and government policy.

Our Inflation protection — building robust portfolios report provides more detail on how we expect different strategies to perform across these different scenarios over a three-year time horizon.

Defining your inflation protection strategy

There is no single strategy that best protects against all these inflationary scenarios, meaning that a diversified blend of asset classes and strategies is required to provide broad inflation protection for portfolios.

Most sophisticated, institutional portfolios already have assets that protect against growth-oriented and/or long-term inflation scenarios, such as infrastructure or real estate, which they could complement with commodity-oriented strategies. Other inflationary scenarios, especially stagflation, leave most portfolios vulnerable. Here, commodity-oriented strategies and gold may prove valuable additions to portfolios.

Scenarios in which inflation is met with an aggressive rate response as experienced in 2022 leave portfolios vulnerable to duration risk. They are first a reminder to revisit traditional downside protection sleeves, but they also highlight the potential benefits of floating-rate fixed income assets to portfolios.

Ultimately, the mix of assets appropriate for an investor will depend on a range of factors, including the investor’s existing asset mix and time horizon, under which scenarios the portfolio is most vulnerable, and other investor-specific constraints — such as sensitivity to climate transition risks and ESG considerations.

Questions to help guide inflation protection strategies

- What inflation-sensitive assets already exist in the portfolio, such as equities and real assets?

- Over which time horizon these inflation-sensitive assets provide protection?

- Under which economic scenario the portfolio most vulnerable?

- The type of inflation protection needed; that is, general CPI or specific types (education, healthcare)?

- The liquidity budget and its impact on the ability to invest in private assets with longer lock-up periods?

- The governance budget and thus tolerance for complexity and monitoring of strategies?

- The importance of environment, social and governance (ESG) and non-financial considerations?

Three considerations when reviewing your inflation risks

-

Inflation is not a homogenous phenomenonIt can manifest in different ways, and the risk posed by different scenarios evolves over time.

-

There is no silver-bullet strategyThat works all the time and across all scenarios, a diversified exposure across a range of assets is a more pragmatic solution.

-

Traditional portfoliosDominated by equities and fixed income are ill-suited for inflation.

Global Strategic Research Director, Mercer

US Deputy Head of Capital Markets

Before you access this page, please read and accept the terms and legal notices below.

You’re about to enter a website intended for sophisticated, institutional investors and the information contained herein is not intended for investors who are not qualified purchasers as defined in the US Investment Company Act of 1940. Information about Mercer strategies is provided for informational purposes only and does not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities, or an offer, invitation or solicitation of any specific products or the investment management services of Mercer, or an offer or invitation to enter into any portfolio management mandate with Mercer.

Mercer makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss. Any person unable to accept these terms and conditions should not proceed any further. Mercer reserves the right to suspend or withdraw access to any page(s) included on this website without notice at any time and accepts no liability if, for any reason, these pages are unavailable at any time or for any period.