IRS expands pre-deductible preventive care for HSA-qualifying health plans

Guidance Evolution

Under Internal Revenue Code Section 223, HSAs are tax-favored accounts that individuals can use to pay for medical expenses. HSAs are subject to a variety of rules that determine account holders’ eligibility to contribute, the taxability of withdrawals and the HDHP coverage that must be paired with HSAs.

HSA-compatible HDHPs must satisfy certain requirements, including minimum annual deductibles and maximum in-network out-of-pocket (OOP) expenses for self-only or family coverage. HDHPs generally can’t pay for covered benefits other than preventive care before participants have met the minimum annual deductible. Until then, HDHP enrollees must pay the full cost of medications and services that aren’t considered preventive care. Enrollees can use their HSA funds, if available, to pay these expenses.

An HDHP can set a lower deductible for preventive care than for other benefits or waive the deductible and charge only a preventive care copayment. This type of preventive coverage does not prevent an HSA owner from making or receiving tax-free HSA contributions. Guidance on what precisely is “preventive care” that HDHPs can cover before any deductible has been evolving since 2004.

Preventive Care Safe Harbor

Section 223(c)(2)(C) provides a safe harbor that lets HSA-qualified HDHPs waive the deductible for preventive care benefits. Although the law does not define “preventive care,” IRS Notice 2004-23 says that pre-deductible HDHP coverage for preventive care can include:

- Periodic health evaluations like annual physicals, including tests and diagnostic procedures

- Routine prenatal and well-child care

- Immunizations for children and adults

- Smoking-cessation programs

- Weight-loss programs

- Various screening services, such as mammograms or glaucoma screenings

For a complete list of covered screenings, see the appendix in Notice 2004-23.

Certain drugs and medications qualify as preventive care. In Notice 2004-50, IRS addresses a series of Q&As on HSA compliance issues. Q&A-27 clarifies that in certain cases, drugs and medications can qualify as pre-deductible preventive care when someone is at risk for developing a disease that’s not yet clinically apparent (i.e., is asymptomatic) or needs to prevent the recurrence of a disease from which the individual has recovered. Examples include statin drugs that reduce cholesterol to prevent heart disease and angiotensin-converting enzyme (ACE) inhibitors to prevent a recurrence of heart attack or stroke. Drugs used as part of preventive care programs described in Notice 2004-23, such as obesity weight-loss and tobacco-cessation programs, also can satisfy the safe harbor.

Any ACA-required preventive service falls within safe harbor. IRS Notice 2013-57 provides that pre-deductible HPHP benefits can include any preventive service for which the Affordable Care Act (ACA) requires non-grandfathered health plans to provide first-dollar, in-network coverage. In other words, an HSA-compatible HDHP can cover ACA preventive care at no cost to participants who have yet to meet the deductible. However, HSA-qualifying HDHPs can still impose deductibles or other participant cost-sharing for preventive care benefits not mandated by the ACA, even if they fall within the IRS safe harbor.

Safe Harbor Limitations

Guidance on what services do not qualify for the preventive care safe harbor has also been evolving over time.

Treatments for existing illness don’t qualify. The original guidance in Notice 2004-23 specifies that services to treat an “existing illness, injury, or condition” are not preventive care. However, Q&A-26 of Notice 2004-50 clarifies that a treatment which is incidental or ancillary to pre-deductible preventive care falls within the safe harbor if performing another service would be unreasonable or impracticable. For example, an HDHP may cover surgical expenses for removing polyps found during a preventive colonoscopy before the deductible is met.

State-mandated cost-free coverage doesn’t qualify. Notice 2004-23 notes that state laws do not determine what preventive benefits an HSA- qualified HDHP can cover without imposing a deductible. So if a state law requires insurers to cover — with a lower or no deductible — a service not defined as preventive care for the IRS safe harbor, the plan may not qualify as an HDHP and its participants won’t be eligible to make HSA contributions.

In Notice 2004-43, the IRS provided transition relief allowing insured health plans to qualify as HDHPs through 2005 even if they covered pre-deductible state-mandated benefits not recognized as preventive care under the safe harbor. Similar transition relief in Notice 2018-12 lets HDHPs provide pre-deductible coverage of male contraceptives or sterilization until 2020 in states requiring these benefits without cost.

Additions to Preventive Care Safe Harbor

Part of last month’s executive order on healthcare cost and quality transparency directs the Treasury Department to issue guidance expanding the use of HSAs by people with chronic conditions. Existing guidance bars HSA-qualified HDHPs from providing first-dollar coverage of disease-management services for individuals with chronic conditions — like insulin, eye and foot exams, and glucose-monitoring supplies for diabetics.

Some employers and health policy advisers have long advocated that pre-deductible HDHP coverage should include secondary preventive services for chronic conditions. Some advocates have specifically called for allowing first-dollar HDHP coverage for targeted, evidence-based, secondary preventive services that prevent chronic disease progression and related complications. In theory, expanding the safe harbor to include these services would improve patient-centered outcomes, add efficiency to medical spending and enhance HDHPs’ attractiveness.

Certain Drugs, Services and Supplies for Specific Conditions Now Viewed as Preventive Care

In response to the July executive order, IRS and Treasury, in consultation with HHS, published Notice 2019-45 expanding the preventive care safe harbor to allow pre-deductible HDHP coverage of specific medications and supplies for certain chronic conditions. According to the agencies, the added items are low-cost and clinically proven to keep a chronic condition from getting worse or triggering a secondary condition that is expensive to treat. The agencies also claim there is “medical evidence supporting the high cost efficiency (a large expected impact) of preventing exacerbation of the chronic condition or the development of a secondary condition.”

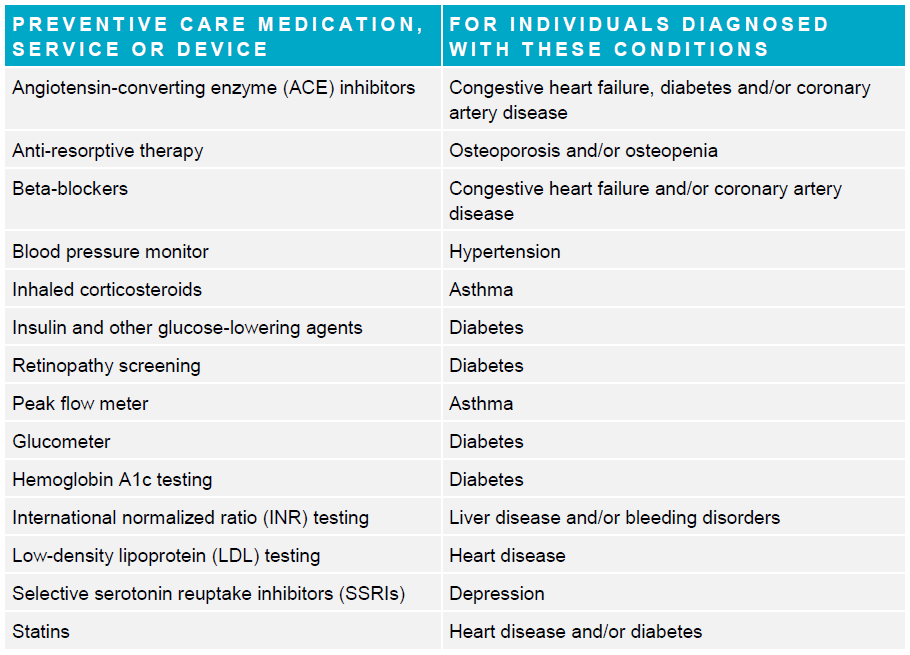

The following table shows which medical services and items used to treat certain chronic conditions are now recognized as preventive care eligible for pre-deductible HDHP coverage.

Limitations on coverage of the new items. The listed items are treated as preventive care only when prescribed for someone with the specified chronic condition and for the purpose of preventing the condition from getting worse or triggering a secondary condition. Unless listed in Notice 2019-45, items and services to treat secondary conditions or complications that occur despite any preventive care do not fall within the safe harbor.

Room for interpretation? Treasury and IRS stress that although other medical drugs, supplies and services may meet the cost and clinical efficacy criteria used to develop the new guidance, only items specifically listed in Notice 2019-45 are treated as preventive care for chronic conditions.

Pre-deductible HDHP coverage can still include other types of preventive care recognized in earlier guidance — specifically, Notices 2004-23, 2004-50 and 2013-57. Unlike Notice 2019-45, the list of preventive care items and services in Notice 2004-23 is expressly not exclusive of other items that could be considered preventive for purposes of the safe harbor.

Clarifications Needed

Notice 2019-45 may not include all items and services related to chronic conditions that some plans have been covering as preventive care based on previous guidance. Those plans will have to assess whether they can continue to justify pre-deductible coverage under prior guidance or must drop that coverage for any items and services related to chronic conditions not identified in Notice 2019-45.

For example, the new list identifies blood pressure monitors as preventive care when prescribed for individuals with hypertension, but not blood pressure medications like ACE inhibitors and beta-blockers unless prescribed for someone with congestive heart failure, diabetes or coronary artery disease. HDHPs that provide pre-deductible coverage for other blood pressure medications or for ACE inhibitors and beta-blockers when prescribed for conditions other than those listed will have to evaluate whether continuing this pre-deductible coverage is permissible. HDHPs that cover antidepressants other than SSRIs as preventive care likewise will have to evaluate whether to continue or narrow that coverage.

The scope of some of the items listed in Notice 2019-45 has also raised questions. For example, the new list covers blood glucose meters for diabetics, but does not include test strips or related supplies. Clarification as to whether or not these related items qualify as preventive care would be helpful.

Employer Next Steps

HSA-qualified HDHPs offer tax advantages for employees and employers. An HSA is one of the few savings vehicles that offers a triple tax advantage to the owner: pretax or tax-deductible contributions; tax-free earnings (investment, interest) on accumulated funds; and tax-free distributions for qualified medical expenses. If an employer makes HSA contributions (e.g., seed, matching, wellness incentive, etc.) on an employee’s behalf, those amounts are excluded from the employee’s gross wages and are deductible by the employer as a business expense. An employer's HSA contributions (including an employee's pretax contributions through a cafeteria plan) are not subject to federal income tax withholding or Social Security, Medicare, federal unemployment (FUTA) or railroad retirement taxes if the employer reasonably believes at the time of payment that the contribution will be excludable from the employee's income.

The expanded list of preventive care for items and services to manage chronic conditions is a welcome development for employers and health policy advocates looking to increase HSA-qualified HDHP participation. However, Notice 2019-45 may not go far enough. The items and services chosen for identified chronic conditions are limited, and other common chronic conditions have been left off the list.

In light of this new guidance, employers should consider the following:

- Review current preventive care coverage in any HSA-qualified HDHP in light of the new guidance, keeping these points in mind:

─ HDHPs must cover ACA-required preventive care at no cost to participants who have yet to meet to the deductible.

─ HDHPs are allowed — but not required — to provide pre-deductible preventive care benefits meeting the IRS safe harbor.

─ Heightened risk of violating the HSA eligibility criteria if a HDHP continues to cover items or services pre-deductible that are not specified as preventive in official guidance.

- Decide which preventive care items allowed by the safe harbor to provide pre-deductible after assessing employee needs and costs to the plan. Expanding pre-deductible coverage for items and services related to chronic conditions could increase enrollment in and utilization of the HDHP.

- Consider the timing of any change in pre-deductible coverage. Midyear changes to plan coverage are possible if allowed under the plan document and summary plan description (SPD). However, the plan may have to provide notice — in advance if the change affects information in the plan’s summary of benefits and coverage (SBC) — to plan participants, particularly if eliminating items or services from the plan’s preventive care category. Consult with vendors like third-party administrators or pharmacy benefit managers to identify other administrative challenges to implementing midyear changes.

The IRS, Treasury and HHS anticipate revisiting the list of items and services that qualify as preventive care for chronic conditions only every five or 10 years. However, regulators may issue clarifying guidance sooner than planned if Notice 2019-45 proves difficult to implement.

Related Resources

Non-Mercer Resources

- Notice 2019-45, Additional Preventive Care Benefits Permitted To Be Provided by a High Deductible Health Plan Under § 223 (IRS, July 17, 2019)

- Executive Order 13877, Improving Price and Quality Transparency in American Healthcare To Put Patients First (Federal Register, June 27, 2019)

- Notice 2018-12, Transition Relief on Application of Section 223 to Certain Health Plans Providing Benefits for Male Sterilization or Male Contraceptives (IRS, March 5, 2018)

- Health Savings Account-Eligible High Deductible Health Plans: Updating the Definition of Prevention (University of Michigan Center for Value-Based Insurance Design, May 14, 2014)

- Notice 2013-57, Preventive Health Services Under Public Health Service Act Section 2713 and Preventive Care for Health Savings Accounts (IRS, Sept. 9, 2013)

- Notice 2004-50, Health Savings Accounts — Additional Q&As (IRS, Aug. 9, 2004)

- Notice 2004-43 (IRS, June 18, 2004)

- Notice 2004-23 (IRS, March 30, 2004)