2023 health FSA, other health and fringe benefit limits now set

IRS Rev. Proc. 2022-38 gives the 2023 contribution and benefit limits for health flexible spending arrangements (FSAs), qualified small-employer health reimbursement arrangements (QSEHRAs), long-term care (LTC) policies, transportation fringe benefits and adoption assistance programs. The 2023 figures reflect the increase in the average chained Consumer Price Index for All Urban Consumers (C-CPI-U) for the 12 months ending Aug. 31, 2022, after applying statutory rounding rules.

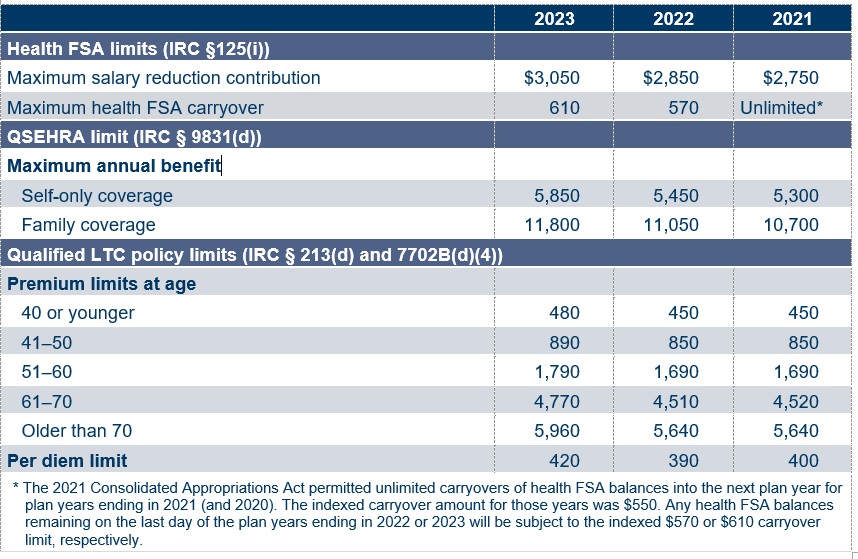

Health FSA, QSEHRA and LTC limits

This table shows the 2023 adjusted amounts for health FSAs, QSEHRAs and qualified LTC policies, along with the limits for 2022 and 2021. The health FSA carryover limits shown reflect the maximum unused funds that can carry over to the next plan year.

The 2023 adjusted amounts for health savings accounts (HSAs), HSA-qualifying high-deductible health plans, excepted-benefit HRAs, out-of-pocket maximums in non-grandfathered group health plans and various indexed amounts for the ACA’s employer-shared responsibility provision were announced earlier this year.

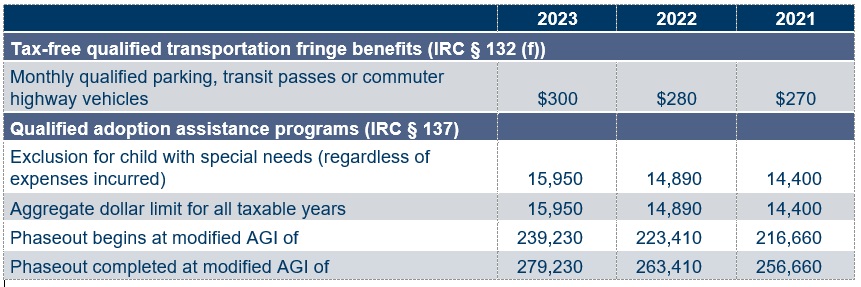

Qualified transportation fringe benefits and adoption assistance programs

This table shows the 2023 adjusted figures for qualified transportation fringe and adoption assistance benefits set by Rev. Proc. 2022-38, along with amounts for 2022 and 2021.

Related resources

Non-Mercer resources

- Rev. Proc. 2022-38 (IRS, Oct. 18, 2022)

- IRS provides tax inflation adjustments for tax year 2023 (IRS, Oct. 18, 2022)

- Notice 2020-33 (IRS, May 12, 2020)

Mercer Law & Policy resources

- Affordability percentage for employer health coverage will shrink in 2023 (Sept. 14, 2022)

- 2023 transportation and health FSA limits projected (July 19, 2022)

- 2023 HSA, HDHP and excepted-benefit HRA figures set (May 3, 2022)