Investing in Middle East private equity funds: the key is alignment

Limited partner perspectives

The Middle East private equity industry has faced some challenges in attracting institutional and international investment, with the alignment of the general partner (GP) and investor interests regularly cited as a deterrent to investing. This article outlines the key opportunities, why alignment is critical, and how limited partners (LPs) should consider alignment as part of the investment due diligence process.

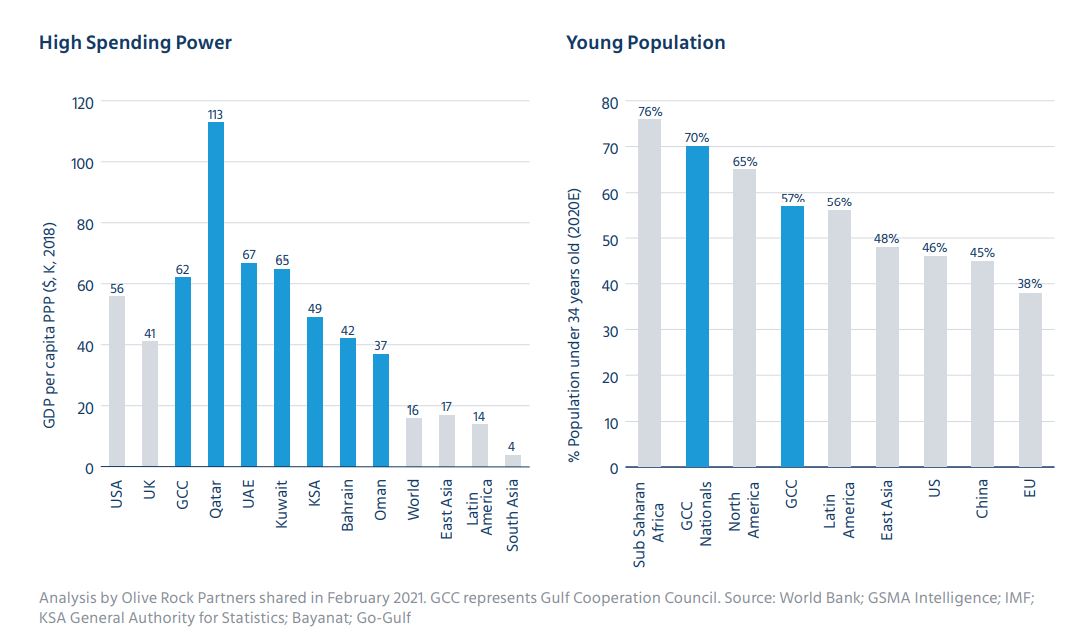

The Middle East boasts demographics conducive to investment, being home to a young population with a high spending power. Government initiatives have driven positive demographic shifts towards diversification and socioeconomic empowerment. Examples of these government initiatives include the Kingdom of Saudi Arabia’s (“KSA”) Vision 2030 as well as a region-wide focus on boosting labour participation rates and encouraging investment and entrepreneurship.

Chart:

Ongoing government funding programs, such as Saudi Arabia’s Private Sector Stimulus (“PSS”) program, and positive trends in the legal and regulatory framework, such as the new legislation allowing 100% foreign ownership of UAE businesses, further support private sector growth as the region seeks to diversify its economy away from oil.

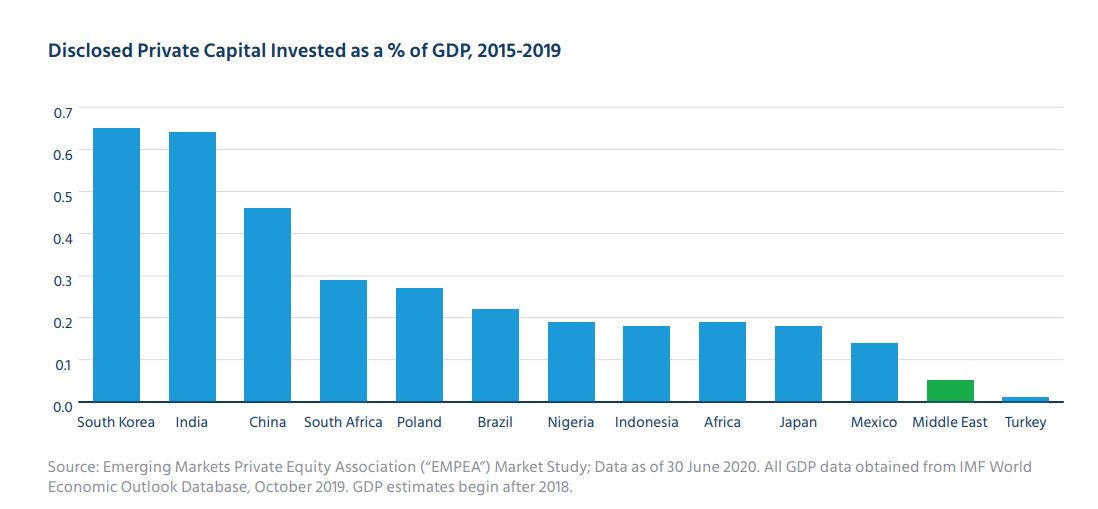

The Middle East is within an 8-hour flight from two-thirds of the world’s population and is strategically centred for trade flows between Africa, Europe and Asia. Despite this, penetration of disclosed private capital in the Middle East market lags other emerging markets significantly.

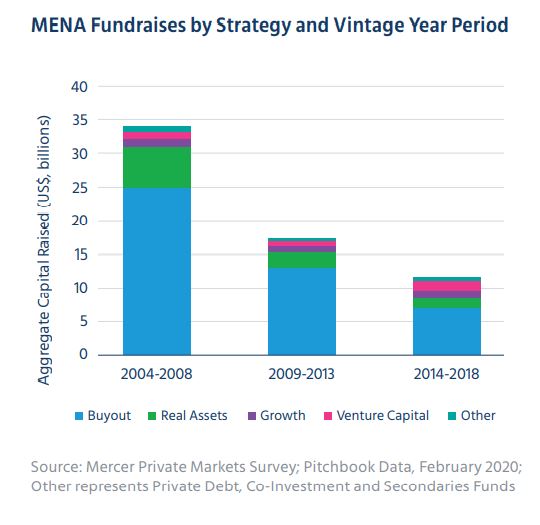

The majority of deal flow and investment is in the United Arab Emirates, representing 55% of private equity capital invested.2 Recent high profile investments, including Uber’s acquisition of Careem and Amazon’s acquisition of Souq.com, highlight the increasing activity of international strategic and private equity investors in the region.

Middle East start-ups continue to attract investment from international private equity investors such as L Catterton, 500 Startups and General Atlantic. Some of the notable tech start-ups in the region are listed below.

| Company | Description | Date of Last Financing Round | Investors |

|---|---|---|---|

| Fetchr | a Middle East delivery service | August 2020 | New Enterprise Associates, BECO Capital, Iliad Partners |

| Property Finder | a technology-based real estate platform | November 2018 | General Atlantic, VNV Global, Xplorer Capital, Pegasus Capital |

| Jamalon | the region's largest online bookstore | March 2019 | Wamda Capital, Endeavour Catalyst, 500 Falcons, Sanded Partners |

| Anghami | a music-streaming platform | January 2021 | Endeavour Catalyst, Middle East Venture Partners, Shuaa Capital, Samena Capital |

Despite its prospects, international LP appetite for Middle East private market funds continues to be muted, with the Middle East consistently scoring low on the attractiveness scale in EMPEA’s investor surveys3. According to participants in Mercer’s Middle East GP survey, many investment teams were not appropriately aligned with distribution of carried interest, ownership of the management company and through commitment to the fund.

In Mercer’s experience, private equity's success depends on the expertise and stability of the investment team, with appropriate checks and balances in place. It is challenging to build an attractive long-term track record with centralized control, weak long-term incentives and high attrition. Any one of those characteristics can act as a deterrent for institutional and long-term investors and limit fund raising.

From Mercer’s deep experience in reviewing private equity funds globally, a clear and appropriate alignment between an investment team and the fund’s LPs has the benefit of safeguarding LP interests.

There are many tenets of assessing the alignment of the fund and its LPs. The key components of alignment are:

-

Team incentives:

a. The fund should have a GP commitment of at least 1.0% with cash commitment from the investment team, or “skin in the game.”

b. The compensation structure for the investment team should be in line with market compensation structures and include allocation of carried interest.

c. Carried interest should be distributed to the investment team and should have a vesting structure over several years to encourage tenure.

-

Protective legal clauses:

a. The fund should be governed by a Limited Partner Advisory Committee (“LPAC”) with its appropriate authority, including access as needed to fund auditors and valuation agents.

b. The fund’s terms should include a Key Person Clause, whereby the departure of (a) key person(s) results in the suspension of investment activities until the LPAC votes to resume activities or remove the GP.

c. The fund’s terms should include for-cause or no-fault divorce clauses, giving the LPAC or LPs the authority to remove the GP.

d. In addition, the fund structure and legal domicile should be aligned with global standards with appropriate regulatory oversight.

-

Fund management fees:

a. The management fee should be appropriate for the strategy and size of the fund.

b. Other expenses should be considered, including the organizational expenses, any subscription fees or fees charged to portfolio companies.

Fund terms and business practices should be questioned appropriately as part of the investment due diligence process. Any changes to the fund terms should be negotiated prior to the fund commitment.

GPs in the Middle East are generally open to reconsidering their alignment structures to meet the criteria required by investors, particularly when those requirements are common international institutional standards. Investors with a robust and institutional due diligence process, and the commitment to working with GPs to incorporate appropriate alignment frameworks, have a higher chance of success in their Middle East private equity portfolios.

Mercer is an investment specialist and has worked with multiple clients with a Middle East investment mandate and has advised on the investment into ten Middle East funds. Mercer also works with clients to develop investment policies and procedures to ensure that the important elements of due diligence are addressed appropriately.

Mercer has offices in Dubai, Abu Dhabi, Riyadh and Amman and employs over 30 staff within its Wealth business in the Middle East. Mercer is the largest investment advisor globally4 and operates the largest Outsourced Chief Investment Officer program globally5.

Sources:

1. Mercer Private Markets Survey; Pitchbook, February 2020.

2. Pitchbook, February 2020

3. EMPEA 2020 Market Study, www.empea.org.

4. Pension & Investments, AUA ranked by worldwide assets under advisement as of June 30, 2019, as reported by each firm to P&I.

5. ai CIO, Global OCIO Assets Under Full Discretion as of December 31, 2019, as reported by each firm to CIO magazine; Willis Towers Watson assets reported as of September 30, 2019.