Employee benefit risk management strategies and insights

Employee benefits risk management (EBRM) helps reduce people risks and rising healthcare costs

The cost and complexity associated with managing employee benefits in a compliant, prudent and fair way makes employee benefits risk management a key priority.

Even so, just two in five businesses (41%) believe they have effective EBRM for insurance and benefit design in place, putting them at risk of errors and poor decisions around design, financing, administration and vendor management. All of which can have substantial implications for the business, potentially leading to reputational and financial damage.

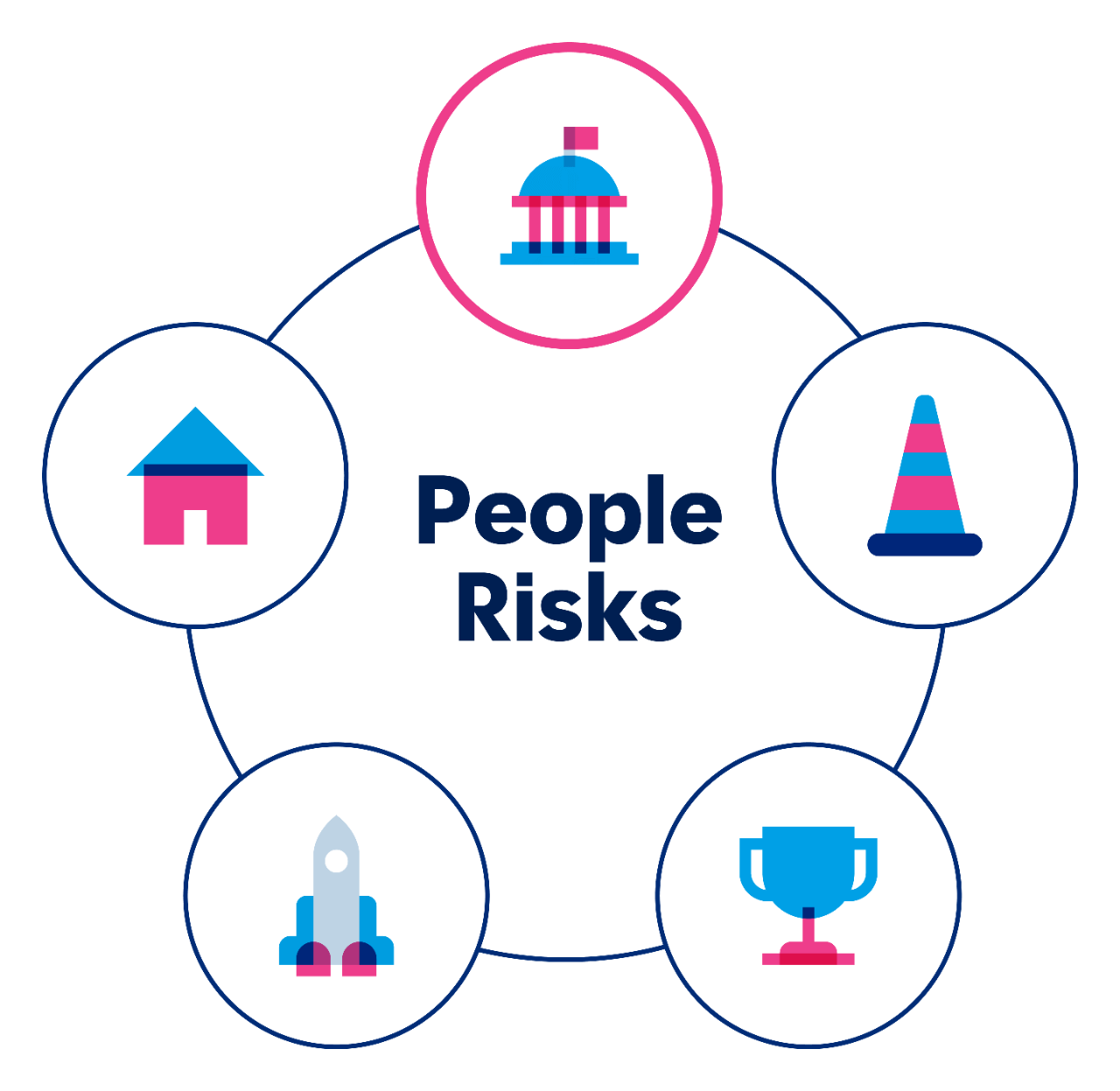

When asked about governance and financial risks they face, HR and Risk professionals highlighted five areas EBRM can help mitigate. This ranges from the administration and fiduciary of employee benefits plans to benefit decision-making and accountability.

Managing the risk associated with the increasing cost of health, risk protection and wellbeing benefits is also a top priority. Not least as our health trends report [LINK] reveals healthcare costs are rising at three times the rate of inflation. Pension benefits can also be challenging to administer and manage, especially where dynamic investment strategies or legacy arrangements exist.

Employee benefits risk management: governance and financial risks

Category Risks:

- Increasing health risk, risk protection and well being benefit cost

- Pension financial risks

- Administration and fiduciary

- Legal and compliance

- Benefit decision making and accountability

-

Increasing health, risk protection and well-being benefit costs.Increased spend due to factors like reduced insurer appetite for risk, medical inflation, increase in utilization, claims duration and severity impacting employee benefit premiums and other costs.

-

Pension financial risks.Investment, inflationary and longevity risks affecting the plan sponsor financial commitments to retirement plan (balance sheet, cash and expense) and individual retirement savings adequacy.

-

Administration and fiduciary.Inability to administer plans accurately, fairly, in accordance with promises made or prudently manage employee benefit programs/investment funds resulting in errors and unmet obligations.

-

Legal and compliance.Misalignment of benefit and other HR practices/programs to regulatory requirements, tax, labor, human rights and employment law causing fines, penalties and litigation.

-

Benefit decision making and accountability.Inappropriate benefit plan design, financing, vendor selection/management, communication and administration decisions due to lack of controls/expertise resulting in suboptimal costs, liabilities and commitments.

Employee benefit risk management services to boost agility and resilience

Robust EBRM requires getting the basics in place, including inventories of coverages and insurers and clear decision-making channels. This can also help you to move quickly in a crisis. For example, during the pandemic, employers with “command and control” over schemes could rapidly identify gaps in access to telemedicine. The same is true for those managing evolving insurer sanctions linked to geo-political events.

Centralized systems can also help with risk management, resilience and agility. 90% of organizations with centralized benefits systems were able to respond quickly to changes, according to our Benefits Tech Report. Compared to just 55% of those with decentralized systems. Unsurprisingly, 47% of organizations plan to fully centralize in the next year.

All of which means, active employee benefit risk management is essential. Those organizations that don’t manage risks may encounter surprise when accounting expenses and liabilities. Such poor compliance with regulatory requirements, tax, or other legislation, can be the cause of fines, penalties, and litigation.

Employee benefit risk management to contain costs

Employee benefit risk management services often prioritize managing risk associated with the rising cost of employee benefits. This is because without proper EBRM, rising health insurance costs, inflation and pressure to offer more benefits, create unsustainable costs.

With the cost of providing employee benefits being pushed up the corporate agenda, cost and empathy need to be balanced. The answer lies in being more strategic about how best to support employees and mitigate people risks, to bring costs down.

For example, preventative healthcare benefits can be offered to reduce the risk of sickness absence in a way that reduces healthcare insurance premiums. This can also make employees feel more cared for by creating a culture that promotes health.

Better design and fiduciary of employee benefits, through coverage provisions and smart financing, can also reduce employee benefits costs, making benefits more affordable so you can create diverse and inclusive benefits by increasing choice and eligibility.

EBRM: Three elements of an effective cost containment strategy

Employee benefit risk management services for multinationals

Managing risk associated with employee benefits requires lots of tactics across borders. Firstly, you have to be fair and consistent when managing funds and making decisions on behalf of employees, and secondly, you may be using dozens of insurers for global benefits.

Choosing and negotiating with vendors at a local level can lead to inefficiencies and may be preventing them from leveraging economies of scale across their global broking. And while you need to take local regulations into account, you also want an overarching EBRM strategy to incorporate local benefits plans.

Bundling employee benefits under regional and global benefits management arrangements reduces workload, maximizes financial impact, and ensures consistency in governance.

People Risk Report 2022

Questions to ask when looking to balance risk and cost as part of your EBRM strategy

-

What steps are you taking (at the local and global levels) to ensure benefits are being managed appropriately in each country?

-

Do you have specific strategies to manage health risk and steer people to high quality, efficient care to manage costs?

-

How do your local HR teams report upward into headquarters and seek approval or guidance regarding benefits design and placement?

-

Have you taken an enterprise risk management approach to your benefits programs to address the risks inherent in your benefits plan?

-

What assurance has been undertaken on your risk governance arrangements, and how does your approach compare to similarly sized industry peers?